- 762.54 KB

- 2022-04-29 14:05:25 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

'29January2018AsiaTechnologyEQUITIESSEMICONDUCTORMakingsenseoutof3Dsensingforepi-wafermakersTaiwanAdoptionof3Dsensingtoriserapidlyinmanyapplications,SamsonHung*ResearchAnalyst,Technologysuchassmartphones,self-drivingcarsandindustryautomationHSBCSecurities(Taiwan)CorporationLimitedsamson.hm.hung@hsbc.com.twSmartphoneisthekeydriverin2018-19andepi-wafervendors+886266312863WillCho*shouldbenefitfromoutsourcingpartnershipswithIDMsAnalyst,HardwareandMaterialsTheHongkongandShanghaiBankingCorporationLimited,Epi-waferplayersinTaiwanareVPEC,HLJandLandMark(Buy)SeoulSecuritiesBranchrickyjuilseo@kr.hsbc.com+822370687773DsensingdemandtogrowthrapidlydriveninitiallybysmartphoneadoptionandBruceLu*laterbynewareas,suchasVR/AR,autonomousdriving(e.g.LiDAR)andindustryAnalyst,TechnologyHSBCSecurities(Taiwan)CorporationLimitedautomation.Taiwanepi-wafermakersstandtobenefitfrom(1)outsourcingdemandbruce.kl.lu@hsbc.com.twfromaleadingIDMand(2)structuralgrowthfromnon-smartphoneapplication.We+886266312861forecastepi-waferdemandtogrowataCAGRof105%from2017to2019e.Keyepi-StevenPelayo,CFAGlobalHeadofTechnologyEquityResearchwafervendorsinTaiwanincludeVPEC(2455TT,notrated),LandMark(3081TT,TheHongkongandShanghaiBankingCorporationLimitedBuy),HLJ(3688TT,notrated),andEpistar(2448TT,Reduce).stevenpelayo@hsbc.com.hk+85228224391FocusingonApplesupplychainin2018.Before2020,wethinksmartphonecouldAnthonyLiao*stillbethemaindriverfor3DsensingdemandandiPhonewillstilldominatein3DResearchAssociate,TechnologyHSBCSecurities(Taiwan)CorporationLimitedsensingsolutionsintermsofbothhardware(VCSELLDandmoduledesign)andanthony.wc.liao@hsbc.com.tw+886266312865algorithm.WeseescopeforallthreenewiPhonemodelsin2018toadoptFaceIDandlikelyanextra3Dsensingsolutionintherear(althoughspecforVCSELandwhich*Employedbyanon-USaffiliateofHSBCSecurities(USA)Inc.andnotmodelswilladoptitareuncertain).ForAndroid,wethinkthe2018adoptionratewillberegistered/qualifiedpursuanttoFINRAregulationslowgiven(1)latedesignandlimitedsupply,(2)lackofalgorithm,and(3)costconcerns.VendorslandscapeforApplebeyond2017.WithiniPhonesuppliers,wethinkLumentummayremaintheleadingsupplierofdotprojectors,asFinisarmaytaketimetorampup.II-VIandLumentumcouldbetwomajorsuppliersforfloodilluminators.Withintheepi-wafersupplychain,LumentummayseeknewsuppliersinTaiwanasitgivesLumentumaccessto(1)lowercosts,(2)flexiblesupply,and(3)betterlogisticmanagement.Taiwanepi-wafermakerswithVCSELLDcapabilityareLandMark(3081TT,Buy)andVPEC(2455TT,NR).WethinkLED-basedMiFIDII–Researchepi-wafervendorssuchasEpistar(2488TT,Reduce)arelaggingbehindtheIsyouraccessagreed?requiredtechnologyhurdlewhiletheepi+chipbusinessmodelscouldbeviewedasCONTACTustodaypotentialcompetitorsbyexistingIDMplayers.Keyratingsandestimatesforepi-wafermanufacturerssupplyingtothespecialtysemiconductorsectorTargetImplied_______PE_____________PB_________ROE(%)____Dividendyield(%)pricePrice(LC)Upside/MktcapCompanyTickerRating*(LC)25-Jan-2018downside(USDbn)2018e2019e2018e2019e2018e2019e2018e2019eLandMark3081TTBuy460.0372.024%1.224.218.67.46.433.436.83.34.3Epistar2448TTReduce24.052.3-54%2.050.590.81.11.12.21.20.80.7VPEC2455TTNotratedNA105.0NA0.734.329.96.87.018.121.32.22.8FinisarFNSRUSNotratedNA18.96NA2.216.313.11.31.25.411.0NANAIQEIQELNNotratedNA110.3NA1.219.013.51.91.710.010.9NANAII-VIIIVIUSNotratedNA44.75NA2.822.716.42.82.414.417.3NANAHLJ3688TTNotratedNA163.99NA0.4NANANANANANANANASource:Bloombergconsensusforecastsfornon-coveredcompanies,HSBCestimatesforcoveredcompaniesDisclosures&DisclaimerIssuerofreport:HSBCSecurities(Taiwan)CorporationLimitedThisreportmustbereadwiththedisclosuresandtheanalystcertificationsintheDisclosureappendix,andwiththeDisclaimer,whichformspartofit.ViewHSBCGlobalResearchat:https://www.research.hsbc.com

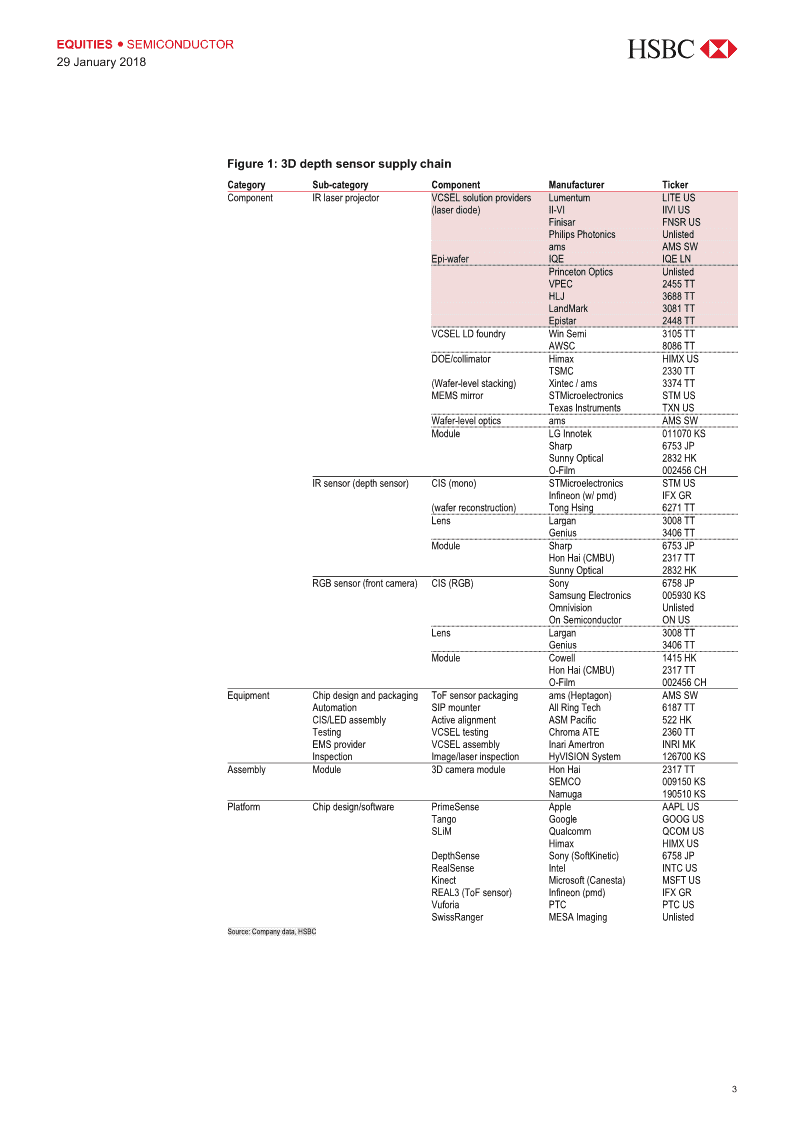

EQUITIES●SEMICONDUCTOR29January2018Buildingblockfor3DsensingThisreportfocusesonpotentialbeneficiariesamongtheepitaxywafermakersfromtherapid3DsensingdemandgrowthEpi-wafermakersarelikelytobenefitasoutsourcingpartnerstoleadingIDMsforsmartphonedemandin2018-19eMajorplayersinTaiwanareVPEC(2455TT,NR),LandMark(3081TT,Buy),HLJ(3688TT,NR),andEpistar(2448TT,Reduce)3Dsensing–theeyesoffuturemachinesWhetheritisAR/VR,autonomousdriving,orindustryautomation,oneofthecommonfeaturestomakethesetechnologieshappenisforthemachineto“see”thingsinathree-dimensionway.Thisisso-calledmachinevision.Inthepast,whatmachinescouldseewasmostlya2Dpicture,i.e.withoutdepthinformation.Withmoreandmoreprecisionrequired,itiscrucialformachinestodevelopthecapabilitytoperceivethingswithdepthinformation.Thisistermed“3Dsensing”.LastyearHSBCanalyst,WillCho,publishedareportAsiaTechHardware–Futurevision:theriseof3Ddepthsensing(11April2017)talkingaboutthe3Dsensingmarketandtheapplications.Thereareseveralkeypartsofa3DsensingmoduleandwecompileacomprehensivekeysupplychaincompaniesinFigure1.WithinApple3Dsensingsupplychain,HSBCTechnologyResearchteamcovers:LGInnotek:(Buy:Welldiscounted,publishedon23January2018)Largan:(UpgradetoBuy:Worstshouldbeover,publishedon11January2018)ChromaATE:(Hold:Multiplegrowthdriversbutloftyvaluation,publishedon30October2017)WinSemiconductors(Hold:3Q17strongbeat,momentumtocontinuein4Q,publishedon30October2017)ThisnotefocusesonVCSELsolutionforsmartphone3DsensingVCSEL(verticalcavitysurfaceemittinglaser)isthepreferredstructureforlaserdiodesusedinthe3Dsensingmodule.AccordingtoresearchbyMarketsandMarkets,theglobalVCSELmarketwillgrowataCAGRof17.3%fromUSD0.95bnin2015toUSD3.1bnin2022.Thisestimateincludesalltheapplicationssuchascommunication,sensing,andindustrialdemand.Inthisnote,welookatVCSELsolutionprovidersandepi-wafermanufacturersinboththeAppleandAndroidsupplychainforepi-wafermakers.Ourestimaterevenuefromsmartphone3Dsensingopportunitymayaccountforonly5%oftotaldemandin2019e.For3DsensingVCSELsolutionproviders,wethinkthekeyplayerswillbeLumentum,Finisar,II-VI,andams.Keyepi-waferplayersareIQE,VPEC,HLJ,andLandMark.2

EQUITIES●SEMICONDUCTOR29January2018Figure1:3DdepthsensorsupplychainCategorySub-categoryComponentManufacturerTickerComponentIRlaserprojectorVCSELsolutionprovidersLumentumLITEUS(laserdiode)II-VIIIVIUSFinisarFNSRUSPhilipsPhotonicsUnlistedamsAMSSWEpi-waferIQEIQELNPrincetonOpticsUnlistedVPEC2455TTHLJ3688TTLandMark3081TTEpistar2448TTVCSELLDfoundryWinSemi3105TTAWSC8086TTDOE/collimatorHimaxHIMXUSTSMC2330TT(Wafer-levelstacking)Xintec/ams3374TTMEMSmirrorSTMicroelectronicsSTMUSTexasInstrumentsTXNUSWafer-levelopticsamsAMSSWModuleLGInnotek011070KSSharp6753JPSunnyOptical2832HKO-Film002456CHIRsensor(depthsensor)CIS(mono)STMicroelectronicsSTMUSInfineon(w/pmd)IFXGR(waferreconstruction)TongHsing6271TTLensLargan3008TTGenius3406TTModuleSharp6753JPHonHai(CMBU)2317TTSunnyOptical2832HKRGBsensor(frontcamera)CIS(RGB)Sony6758JPSamsungElectronics005930KSOmnivisionUnlistedOnSemiconductorONUSLensLargan3008TTGenius3406TTModuleCowell1415HKHonHai(CMBU)2317TTO-Film002456CHEquipmentChipdesignandpackagingToFsensorpackagingams(Heptagon)AMSSWAutomationSIPmounterAllRingTech6187TTCIS/LEDassemblyActivealignmentASMPacific522HKTestingVCSELtestingChromaATE2360TTEMSproviderVCSELassemblyInariAmertronINRIMKInspectionImage/laserinspectionHyVISIONSystem126700KSAssemblyModule3DcameramoduleHonHai2317TTSEMCO009150KSNamuga190510KSPlatformChipdesign/softwarePrimeSenseAppleAAPLUSTangoGoogleGOOGUSSLiMQualcommQCOMUSHimaxHIMXUSDepthSenseSony(SoftKinetic)6758JPRealSenseIntelINTCUSKinectMicrosoft(Canesta)MSFTUSREAL3(ToFsensor)Infineon(pmd)IFXGRVuforiaPTCPTCUSSwissRangerMESAImagingUnlistedSource:Companydata,HSBC3

EQUITIES●SEMICONDUCTOR29January2018Figure2:Valuationcomparisonsformajorcompaniesinthe3DsensingVCSEL/epi-wafersupplychainStockHSBCTPPriceMktcapEV/EBITDA__PE(x)___PB(x)__Salesgrowth(%)_OPM(%)_EPSy-o-y(%)ROE(%)_coderating(LC)(LC)(USDbn)18e19e18e19e18e19e18e19e18e19e18e19e18e19eLumentumLITEUSNotratedNA44.502.89.27.113.211.23.32.625.014.515.715.4781720.924.0FinisarFNSRUSNotratedNA18.962.26.65.516.313.11.31.2-6.611.410.114.1-43255.411.0II-VIIIVIUSNotratedNA44.752.811.610.422.716.42.82.420.014.213.216.3314114.417.3IQEIQELNENotratedNA1101.219.616.519.013.51.91.716.828.719.919.3294110.010.9VPEC2455TTNotratedNA1050.723.819.034.329.96.87.017.87.126.727.0411518.121.3LandMark3081TTBuy4603721.215.712.224.218.67.46.456.327.151.452.91013033.436.8Epistar2448TTReduce2452.32.07.17.550.590.81.11.1-0.41.05.93.4-28-442.21.2WinSemi3105TTHold2262403.511.09.719.116.74.54.023.79.529.931.3411425.325.4AWSC8086TTNotratedNA69.70.322.9n.a.28.7n.a.3.2n.a.15.9n.a.n.a.n.a.44n.a.12.4n.a.Average14.211.025.426.33.63.318.712.621.622.515.818.5Note:Pricedasofcloseon25January2018.Source:Bloombergconsensusforecastsfornon-coveredcompanies,HSBCestimatesforcoveredcompaniesEpi-waferdemandfor3DsensingtogrowrapidlyAftertheiPhoneXlaunch,a3Dsensingfeaturehasbecomeakeytopicformajorhandsetbrands,andwebelievemostofthemareworkingwithsupplychaincompaniestodevelopsuitablesolutionsfor3Dsensing.Inthelongerterm,3DsensingwillbeusedforotherrapidlygrowingapplicationssuchasLiDARinautonomousdrivingandinindustryautomationdeployment.Webelievethekeygrowthdriverfor3Dsensingepi-waferdemandinthenexttwotothreeyearswillbemainlyfromsmartphoneadoption.Perourestimates,theglobalepi-waferunitdemandglobalepi-wafersinsmartphonescouldseea2017-19eCAGRof105%.Ourkeyassumptions:AllnewiPhonemodelsadopttheFaceIDfeatureonthefront5%Androidadoptionin2018eand15%in2019eAssumingAndroidVCSELdemandpersetis60%ofApple’sdesign–forexample,somemaynotusefloodilluminatororcouldswitchtoIRLEDinsteadofIRlaserVCSEL.Ourassumptionsdonotincludepotential3Dsensingmoduleadoptionontherear,asitistooearlytodeterminethediesizeandthestructureofthelaserdiode(LD)used.However,weseescopeforAppletoincludethefeatureinthereartoexpanditscapabilityandapplicationsintootherareas.OurLGInnotekanalyst,WillCho,believesthattheaggressivecapexplanfromLGIindicatedpotentialnewdemand.InhisKoreahardwarenoteof20January2018,4Q17Preview:Takingshelterfromnear-termheadwind,hewrote:“LGIrecentlyannouncednewcapexplantoinvestKRW874bnfor2018-19incameramodulecapacityexpansionandnewcamera-relatedtechnology.Weassumethat80%oftotalcapexwillbededicatedto3Dsensorsand20%todualcameras,andmorethan70%Figure3:Selectedglobal3DsensingVCSELsupplychaincompaniesCampsApplesupplychainamsOtherstandaloneplayersSolutionproviderLumentumFinisar(IDM)II-VI(IDM)amsIntel(RealSense)IQE/VPEC(2455TT;potentiallystartingVPEC,LandMark,HLJ,Epi-WaferFinisarII-VIHLJ,Princeton,in-house2018)Accelink,CETC,SinoSemicLDchipfoundryprocessWinSemiFinisarII-VIAWSC,in-houseAWSC,HLJDOETSMC,Xintec,HimaxHimaxCameramodule,lasermodule,FinalmoduleassemblyLGInnotek,SharpSunnyOpticalLEDpackagerQualcomm,smartphonein-Mainchips/AlgorithmAppleQualcommhouseSource:HSBC4

EQUITIES●SEMICONDUCTOR29January2018willbeimplementedin2018inordertomakenewlinescomeonlinefrom2H18e.Giventhattheinitialcapexfordualcameraand3DsensoramountedatKRW250-300bn,respectively,in2017,thisnewinvestmentwith3xlargerscaleimplies(1)higheradoptionof3Dsensor,(2)introductionofnext-generation3Dsensingtechnology,and(3)persistingLGIdominancefor3Dsensors.Accordingly,weraise3DsensorpenetrationwithinApple(AAPLUS,USD179.27,Buy,coveredbyStevenPelayo)to89%by2019efrom79%andliftLGI’sordershareto60%from54%in2019e.”Figure4:Epi-waferdemandfor3Dsensinginsmartphone(unit)60,00040,00020,00002017e2018e2019eAppleNonAppleSource:HSBCestimatesWithinTaiwanepi-waferplayers,wethinkVPEC(2455TT,notrated)couldbecomeasecondsourceofVCSELepi-wafers,whicharenowsuppliedonlybyIQE.WethinkHLJ(3688TT,notrated)isalsoworkingwithams(AMSSW,notrated)todevelopsolutionsforAndroidsmartphones.WebelieveLandMark(3081TT,Buy)shouldbeanotherbeneficiaryoflonger-termopportunitiesinautonomousdrivingtechnologiessuchasdemandforLiDAR(lightdetectionandranging)orthemachinevisionsolutionsrelatedtoindustryautomation.WeseescopeforEpistar(2448TT,Reduce)tobeconsideredaviablepartnerinVCSELLDproductionasithasamplecapacityandknowledgeincompoundsemiconductorfabricationandthenecessaryknow-howforimplementingmetal-organicchemicalvapourdeposition(MOCVD).AreportintheEconomicNewson1December2017indicatedthattherearesolutionprovidersthathavesoughtcooperationopportunitieswithEpistaroverthepast2-3years,includingLumentum,II-VIandevenIQE.ThereportalsoindicatedthatsomeIDMshavealsoaskedEpistarforsamplingbyeitherEpistar’srecipeorportingtheirownsolutions.However,wethinkitiscapableofgreaterproductrangethanitscurrentoutput.However,inourview,keyglobalsolutionproviders,suchasLumentumandFinisar,couldviewLEDcompaniesasapotentialcompetitorsintermsoftheirbusinessmodelsasLEDcompanieshavecapabilitiesinbothepi-wafergrowthandchipprocess.TheseglobalsolutionproviderscouldbeconcernedthatifLEDcompanieslearnhowtoproduceepi-wafersandchips,theycouldcompetedirectlyinthefuture.Currently,weknowLumentumwillworkcloselywithIQEandVPEConepi-waferproduction.Finisarislikelytoproduceepi-wafersinternally,andII-VIislikelytoexpandinternalcapacityforfuturedemand.ForAndroid,wethinkamsmayusethecapacityofitsPrincetonacquisitionorHLJbeforeitrampsupitsownfacilityinSingapore.Asaresult,westruggletofindanysignificantplayersthatarelikelytoworkcloselywithEpistarinthelongterm.5

EQUITIES●SEMICONDUCTOR29January2018VCSEListhepreferredstructurefor3DsensingWebelievetheepi-waferisacriticalpartofthe3Dsensingtechnologyasitdeterminestheperformanceandalsotheproductionyieldsrateforthesubsequentmanufacturingprocess.Giventhenatureofthelaserrequired,(wavelength940umwhichisthemostresistanttothebackgroundnoises),GaAsisthepreferredmaterial.Intermsofthestructure,theVCSEL(verticalcavitysurfaceemittinglaser)ispreferredtotheedgeemittinglaser(EEL)astheVCSELcancoverawiderangleandhencethedesignforotherpartsdoesnotneedtobeassophisticatedasforEEL.ThecurrentLDdesignfor3DsensingusestheVCSELstructure.VCSELhasthefollowingadvantagesoverEEL:TheVCSELstructurecanwithstandhigherpowervoltagewithoutdamagetotheepitaxystructurethantheEELstructure.Itgeneratesanarrowerbandwidth,hencenarrowerlaserspectrum,whichreducestheinterferenceoftheexternallightsource,i.e.sunlight.Theshapeoflightemittedisacircleandhenceiseasierforexternaldevices,suchaslens,tobemountedontopofthelaserdiodes.ItislesssensitivetochangesintemperatureTheoperatingpowerdensityofhigh-powerVCSELislowerthanthatforEELgiventhattheemissionareaislarger.Thiswillalsoresultinlowertemperature/densityratioVCSELiseasiertotest.TheVCSELLDcanbetestedviaawaferprobemachinebyputtingtheprobesontothedieandapplyinganappropriatecurrent.However,forEEL,thediehastobeslicedintoindividualdiesandmountedontoacarrierfortesting.Figure5:ComparisonofVCSELversusEELVCSELEELAreaofilluminationsurfaceedgeShapeoflightCircularOvalLayersofepitaxyseveralhundredsdoubledigitChipprocessmediumdifficultWavelength(nm)upto850630-1550PowerHighLowSpectralwidth1-2nm1-2nmTestEasyDifficultSource:HSBC,companydataHowever,EELstillhasitsownadvantageWebelievetheVCSELshouldbeapreferredstructureforthe3Dsensingapplication.However,ApplealreadyhasveryextensivepatentsfiledfortheVCSEL-based3Dandfacialrecognitionsolutionsusedinitsphones.Itcouldbethereforebechallengingforotherplayerstobypassthepatents.Asaresult,wethinktherewillbetwomajorapproachesfornon-Applesmartphonevendors:BrandsthatconcernedaboutthepatentissuecouldeitherdeveloptheirownsolutionsoralgorithmtoavoidinfringingApple’spatent,oruseEELtoavoiddirectconfrontationwithApple.BrandsthatdonotcareaboutpatentinfringementincertainareasmightjustusetheVCSELsolutionforafastandlower-costsolution.6

EQUITIES●SEMICONDUCTOR29January2018Applesupplychainremainsthekeyfocusin2018WebelieveApplewillcontinuetodominate3Dsensingdemandin2018.WeexpectthreenewmodelsofiPhonetoadoptFaceIDmodule,andthereisscopeforadoptioniniPad.TherearethreeVCSELLDsembeddedinthefront3Dsensingmodules,includingthedotprojector(structuredlight),thefloodilluminator(non-structuredIRlight),andtheproximitysensor(ToF,ortimeofflight).Dotprojector–thelightsourceforemittingstructuredlightforthemajor3Dfacialrecognition.TheVCSELwillemitabeamoflightsource,thelightwillthengothroughlensandDOE(diffractiveopticalelement)andwillthengenerates30kdotstobeprojectedontheuser’sface.Theinfraredcamerawillthenreceivetheimageofthosedotsandusealgorithmtoformdepthinformation.ThekeysupplierofVCSELLDfordotprojectorisLumentumforiPhoneXandweexpectFinisartobecomeasasecondsourcefornewiPhonemodelsin2018.Floodilluminator–thefloodilluminatorisasimplelightsourcethatemitsinfraredlightforsensortodetermineifthereisafaceinfrontofthesensor.Ifso,thedotprojectorisactivatedtoemitpatternedlightforfacerecognition.WebelievethekeysuppliersoftheVCSELLDforfloodilluminatorareLumentumandII-VI.Proximitysensor–theproximitysensorisnotanewsensorintheiPhone.However,fromiPhone7ApplestartedtouseVCSELlaserdiodeasalightsource,replacingLEDasthelightsource.ThebenefitsofswitchingthelightsourcefromLEDtolaseraremainly(1)asmallerformfactorand(2)lowerpowerconsumption.STMicrohasreplacedamsasthesoleproximitysensorsupplier.ThestructureofSTMicro’ssensorissimilartoitsVLX530,withtheVCSELarrayandCMOSimagesensorbuiltintothesamemodule.HowdoesApple’sFaceIDwork?Step1:Floodilluminatoractivatesandemitstheunstructuredlight.Theinfraredcamerathencapturestheimagereflectedofftheobjectinfrontofthephone.TheAPwillfirstdetermineifthereisaface,ifafaceisdetectedstep2isinitiated.Step2:Thedotprojectorisactivatedtoemitastructuredlaserbeam(i.e.30,000dotsafterthelightgoesthroughDOE).TheIRcamerawillthencapturethedotsandcomparethedistributionofthedotsreflectedwiththeoriginalpatterntocalculatethedepthandshapetocreatea3Dimage.Ifthe3Dimagematchestheuser’sidentity,theiPhonewillbeunlocked.Figure6:iPhoneXFaceIDmoduleSolutionProviderEpi-waferSolutionProviderEpi-waferLumentumIQE/VPECLumentumIQE/VPECII-VIII-VIFinisarFinisarSource:Companydata,HSBCestimates7

EQUITIES●SEMICONDUCTOR29January2018KeyVCSELsuppliersforApple’sFaceID–Lumentum,Finisar,andII-VIInApple’ssupplychain,weseetwodistinctstrategiesbydifferentvendors,althoughthereisnocleardifferenceinthebenefitofpursuingtheoutsourcingorin-houseproductionstrategies.Forexample,Lumentum,nowthekeysupplier,wasconcernedthatitwouldnotbeabletohandlethebigvolumeproductionanddynamicnatureoftheconsumerproducts.Itthereforeactsasasystemintegratorandoutsourcesmostoftheproductiontopartners.FinisarandII-VIaremoreconcernedabouttechnologyleakageandsofollowanin-houseproductionstrategy.Figure7:iPhone3DsensingLDsuppliersPartsYearIDMEpi-waferDotprojector2017LumentumIQE2018(potential)LumentumIQE,VPECFinisarFinisarin-houseFloodilluminator2017LumentumIQEII-VIII-VIin-house2018(potential)LumentumIQE,VPECII-VIII-VIin-houseSource:Companydata,HSBCestimatesAndroidsegmentlikelytocatchupin2019WethinkitcouldbedifficultforAndroidsmartphonemanufacturerstolaunchmanynewmodelsequippedwitha3Dsensingfeaturedueto(1)supplyconstraintsforthe3Dsensingmoduleand(2)lackofmainchipswithgoodalgorithmsupport.AndroidsmartphonecompaniesarelaggingbehindApple,asthereisnocompletesolutioninthemarketrightnow.Acomplete3Dsensingmodule,basedonApple’ssolution,involvesseveralkeycomponents,suchasLD(laserdiode),lens,DOE(diffractiveopticalengine),andmoduleassemblersforthefinal3Dsensingmodule.GiveniPhone’slargevolumeanditsrequirementforsophisticatedsolutions,Appleisabletooutsourceallthekeypartstodifferentsupplychains.However,forAndroidsmartphonecompanies,onlythebigplayerssuchasSamsungorHuaweicouldestablishtheirownsupplychains.Webelievesmallerplayersneedsolutionproviderstointegrateandprovideacompletesolution.WebelievethereareseveralplayersthatareworkingaggressivelyfortheopportunitiesintheAndroidsupplychain.Lumentum:AlthoughLumentumwillserveasthekeysupplierforiPhonedemand,wewouldexpectLumentumtoalsoaimtopenetratetheAndroidmarketasanewgrowthdriverbeyondiPhonedemand.LumentummayworkwithQualcommandHimaxtoprovidetotalsolutions.Thefinalmoduleassemblerscouldbeexistingcameramodulesuppliersandopticalcommunicationmoduleassemblers(suchaseLaser),andevensomeLEDmodulecompanies,suchasEverlight,couldstarttoreceivesomeenquiriesaboutpotentialpackagingopportunities.ams:TheAustriancompanyisworkingaggressivelytopenetratethe3DsensingsupplychainespeciallyafteritlosttheproximitysensorbusinessiniPhonefromiPhone7onwards.Asamslackslaserdiodescapability,itmadeafewacquisitionandinvestmentstostrengthenitscapability.In2016,amsacquiredPrincetonOpto,alaserdiodedesigner,toobtainitsstrongcapabilityinLDdesignandknow-how.ItalsoinvestedinHLJ(3688TT),alistedTaiwancompanynowtradingontheemergingboard,andholds15%oftheshares.8

EQUITIES●SEMICONDUCTOR29January2018HLJhasatrackrecordofsupplyingtheVCSELLDforAirPod.amshasalsomadeanannouncementaboutplannedcapexandwilllikelyexpanditslaserdiodecapacityandislikelytoentermassproductionin2019.Weseescopeforamstoformanalliancewithitskeypartners,suchasPrincetonandHLJ,toestablishitslaserdiodecapability.Othersupplychainplayersthatmaybenefit:Forotherepi-wafermakers,wethinkHLJ(3688TT,notrated)maybewell-poisedtogetsomeordersfromamsbeforeamsrampsupinternalcapacityasamsisthebiggestshareholderofHLJ.Meanwhile,wealsoseescopeforHLJandamstoformadeeperstrategicpartnershipasHLJcouldhelpamstomovealongthelearningcurvefasterbyworkingcloselywithams.Figure8:Androidcamp3DsensingpotentialLDepi-wafersupplychainIDMEpi-waferLumentumIQE,VPECamsPrinceton,HLJ,in-houseIndividualplayersEpistar,LandMark,HLJSource:Companydata,HSBCestimatesSizingupepi-wafermarketinsmartphone3DsensingWedonotthinkitisdifficulttoestimatetheaddressablemarketfortheiPhone3Dsensingmoduledemand.However,itisdifficulttocomeoutwithafirmestimateofthetotaladdressablemarketfortherestofthe3Dsensingmarket.ThekeyreasonisthatdifferentcustomerscanhavedifferentLDdesigns,andhencethediesizeandthroughputtimecouldhavehugevariation.iPhonetodominate3Dsensingdemandin2018withinsmartphoneHowever,giventhatAppleislikelytoremainthedominantplayerinthesupplychain,wethinkhigh-endsmartphonemodelsmaytrytoadoptdesignssimilartothoseofApple,soweuseApple’ssolutionasareferencetoproduceanestimatewhichwethinkisthehigh-endofpotentialaddressablemarketinthesmartphonesupplychain.9

EQUITIES●SEMICONDUCTOR29January2018Weusethefollowingspecificationstoformourestimate.Epi-waferandchipspecs:Grossdieperwafer:Dotprojector:13,000-14,000per6-inchepi-wafer/assuming13,000diesperwaferFloodilluminator:30,000-35,000per6-inchepi-wafer/assuming32,500diesperwaferProductionyieldrates(postepi-wafer+chipprocess)Dotprojector:50%+backinOct2017andnowimprovedto70-80%/assuming75%for2018and80%2019Floodilluminator:steadilyataround80%/assuming80%for2018and85%for2019Productionyieldrateatfinalmoduleassemblyat85%for2018eand90%for2019eHSBCcurrentlyforecast2019eglobaliPhoneshipmenttobe255.5munits.WeassumemostoftheiPhonesshippedin2019willbeequippedwithFaceID.Usingthescenarioandassumptionshighlightedearlier,weestimatethattheepi-waferdemandin2019couldbe37.6kwafers.Potentialadoptioninrearforlonger-range3DsensingapplicationThereisanother3DsensingmodulethatmaybeadoptedintherearoffutureiPhones,likelyintendedforlonger-rangesensingapplicationssuchasmeasuringthedimensionofaroomorotherAR/VRapplications.WebelievethepowercouldbehigherthantheexistingdotprojectorLD,asitneedstocoveralongerrange.Wearenotsurewhatthepatternofthestructuredlightwouldbe.Itisalsonotcertainwhentherear3Dsensingmodulewouldbeintroducedorwhichmodelswouldincludeit.Ifwejustdoaquicksimulationusingsomeguesstimates–diesize2xofcurrentdotprojectorandallthreemodelsadoptingtherearsensingmodule–itlookslikeitwillrequireanadditional20MOCVDreactorstoproducethesewafers.Figure9:2019iPhoneDotprojectorepi-waferdemandestimateLDdemand(munits)255.5Dieperwafer(6-inch)13,000Yieldrate80%Gooddieperwafer10,400Moduleyieldrate90%Availablegooddieperwaferpostmoduleassembly9,360Waferdemand(unit)27,297Source:HSBCestimatesFigure10:2019iPhonefloodilluminatorepi-waferdemandestimateLDDemand(munits)255.5Dieperwafer(6-inch)32,500Yieldrate85%Gooddieperwafer27,625Moduleyieldrate90%Availablegooddieperwaferpostmoduleassembly24,863Waferdemand(unit)10,277Source:HSBCestimates10

EQUITIES●SEMICONDUCTOR29January2018ForMOCVDassumption:UsingAixtronG4MOCVDreactor7wafers/perchamber/perrun1runperday(1runperdaycouldbeconservative;wethinkitmaybeabletoreach2runsperday)BasedonourassumptiononMOCVD,weestimatethataMOCVDreactorcouldproduce1,750wafersayear.Accordingtoourestimateof35.6kwafersrequiredfor2019iPhoneproduction,weestimatethattotal22MOCVDwouldberequiredtomeetthatdemand.However,abetterwaytocalculatewaferdemandmaybebasedonpeakproductionrequirementInthiscalculationweassumethatApplewouldneedLDvendorstoproduceenoughepi-wafersforthenewiPhonemodelsinathree-monthperiodintherun-uptothenewproductlaunchperiod(usuallyin3Qto4Q).Itmeansthatepi-wafermakerswillhavetopreparemoreMOCVDtofulfiltheintenseproductionschedule.IfweassumeAppleships170mnewmodeliPhonesin2019eandtheyareallmadeinonequarter,thismeansthatepi-wafermakerswillneedtoproduce1.89mLDperday(assuming90daysperquarter).Thiswilltranslateinto40MOCVDintotal(29fordotprojectorsand11forfloodilluminators).Byconvertingthisdemandintonumberofepi-wafers,weestimatetheneedforaround8,333waferspermonthtoproducebothdotprojectorsandfloodilluminators;incomparisonIQEcurrentlyshipsaround3,500-4,000epi-waferpermonth.Figure11:2019iPhoneLDwaferdemandanalysis–assuming170miPhonetobemadein3monthsDotprojectors-LDdemandperday1,888,889-Gooddieperwafer9,360-waferdemandperday202FloodIlluminator-LDdemandperday1,888,889-Gooddieperwafer24,863-waferdemandperday76Totaldemand-waferperday278-waferpermonth8,333Source:HSBCestimatesFigure12:Epi-wafermonthlydemandforiPhoneatpeakproduction(unit)9,0008,0007,0006,0005,0004,0003,0002,0001,00002017e2018e2019eSource:HSBCestimates11

EQUITIES●SEMICONDUCTOR29January2018AndroidmarketestimatesItismoredifficulttoestimatethedemandfromtheAndroidsegmentasthedesignandpenetrateratecouldvaryalotbetweenmanufacturers.WethususethespecfortheiPhoneasareference,whichwethinkshouldbethehigheststandardintheindustry,hencethemostcapacityconsumingdesign.Basedonthissetofassumptions,forevery10msmartphonesusing3Dsensing,similartoApple’sdesign,1MOCVDisrequiredonanannualbasis.Differentbrandsmayadoptdifferentapproachesindeveloping3DsensingmoduleWebelievedifferentsmartphonecompaniesmayadoptdifferentapproachesindevelopinga3Dsensingmodule.Companieswithbiggervolumeandin-houseAP(applicationprocessor)capabilitymayuseamodelsimilartoApple’stobreakdownthe3Dsensingmoduleintovariouskeycomponentsandtocomeupwiththeirownsolutions.Underthisapproach,thesecompaniescanusetheadvantagesoftheirownAPandalgorithmsforabetterperformance.However,forcompanieswithoutinternalAPandwithsmallervolumes,wethinkitislikelythattheywilladoptfinishedmodulesolutionsprovidedbysolutionproviders.Forexample,Qualcomm,providingthealgorithminitschip,willlikelytoworkwithsupplychaincompaniessuchasHimaxtoprovidetheDOEandWLOforthemodule,andthenprocurethelasersourcefromcompaniessuchasLumentum.Forthemostbullishcasewith97.5%adoption,ouranalysisindicatedthattherecouldbe104MOCVDrequiredfor2019,assumingallandroidsmartphonesadoptFaceIDandthedesignissimilartoApple’ssolution.Ifweusethefingerprintsensorasareference,twoyearsafteriPhoneadoptedthistechnology,thefingerprintpenetrationratefornon-Applesmartphoneswasaround10-15%andthen40-45%threeyearsafteriPhoneadoption.Ifweusethe15%adoptionratein2019eandassumingthecomplexityis60%ofApple’sdesign(forexamplehavingalowerstructuredlightLDspec,andusingtheexistingfrontLEDinsteadofaddingafloodilluminator),wethinkitislikelyanadditional16MOCVDwillberequiredfornon-Applesmartphonedemandin2019e.Figure13:MOCVDdemandfromsmartphone3DVCSELepi-wafer60501240430204032101602017e2018e2019eApple*NonAppleSource:HSBCestimates,*Appledemandbasedonpeaklevelproductionrequirement12

EQUITIES●SEMICONDUCTOR29January2018Figure14:Scenarioanalysisonnon-iPhoneMOCVDdemand(annual)___________________CapacityconsumptionversusAppleFaceIDdesign____________________Adoptionrate60%70%80%90%100%10%6.27.28.39.310.320%12.414.516.518.620.730%18.621.724.827.931.040%24.828.933.137.241.350%31.036.241.346.551.760%37.243.449.655.862.070%43.450.657.965.172.380%49.657.966.174.482.790%55.865.174.483.793.0100%62.072.382.793.0103.3Source:HSBCestimatesRevenuepotentialfromsmartphone3Dsensingepi-wafermarketTocalculaterevenuesize,weuseapriceofUSD2,000perwaferin2017,whichfallsby20%in2018andby15%in2019.Basedonthisassumption,weestimateoverallrevenueforepi-waferin2019couldreachUSD86m,withUSD55mfromiPhoneandUSD31mfromAndroidsmartphonedemand.Notethatifweincludetherear3DsensingfromApple,assumingfromnewmodelslaunchedin2019,wecouldexpectadditional42kwaferdemandandanadditionalUSD96mrevenue.ThissetofnumbersassumesLDwithadiesizetwicethatofthoseusedincurrentdotprojectors.Figure15:Epi-waferrevenuepotentialfromsmartphone(USDm)100.090.080.070.060.050.040.030.020.010.00.02017e2018e2019eAppleNonAppleSource:HSBCestimatesKeyepi-wafersuppliersinTaiwanVPEC(2455TT,notrated):WeseescopeforVPECtopenetratetheiPhoneFaceIDsupplychainin2H18ifitcansuccessfullyrampupitsproductionqualityandyieldrates.VPECisreportedly(Digitimes,1December2017)nowworkingcloselywiththeleading3DsensingLDvendor,Lumentum,andLumentumisincreasingitslevelofsupporttoVPECbyassistingandcooperatewiththecompanyonthefabricationofepi-wafers.WebelievethekeybenefitsthatVPECcouldbringtoLumentumare(1)diversifyingLumentum’sepi-wafersupply(asIQEiscurrentlytheonlysupplier,creatingrisk)and(2)reducingthelogisticscomplexityandshorteningtheproductionleadtimeasLumentumcurrentlyworkswithWinSemiwhosecapacityisinTaiwansoitisbettertohaveanepi-wafermakerthatisalsobasedinAsia.VPECnowhas41MOCVDandismainlyfocusingonpoweramplifiersandopticalcommunicationepi-wafer.VPECisusingtwo6-inchMOCVDfortheR&Dandpilotproductionof3DsensingVCSELLDandplanstoaddanotherfourMOCVDin1H18.13

EQUITIES●SEMICONDUCTOR29January2018HLJ(3688TT,notrated):HLJhasbeeninthelaserindustryforalongtime.ItisadedicatedcompoundsemiconductorIDMcompanywithfocusonsolidstatelaserdiodes.Thecompanyoriginallyfocussedonopticalcommunicationbutafterdemandcollapseditturnedtosolarbusinessinearly2000.Nowthatsolarmarketpricingisnolongerattractive,HLJhasstartedtofocusonVCSELlaserdiodesforrangesensingandotherapplications.HLJcancarryoutbothepi-wafermanufacturingandchipprocess.HLJhaspenetratedApple’ssupplychainwithaToFLDforAirPod’sproximitysensor.HLJmainlyruns2-inchand3-inchwaferproduction,butisplanningtoexpandinto4-inchepi-wafercapacity.Anotherkeydevelopmentisamsbecomingastrategicshareholder;weexpectmorecooperationinfuturebetweenHLJandamsinproductionortheramp-upofams’snewlaserdiodeproductionlineinSingapore.LandMark(3081TT,Buy):LandMarkcanalsofabricateepi-wafersforVCSEL3Dsensinglasers.Infact,webelieveLandMarkwasoneoftheearlycandidatesforsupplyingthe3Dsensingepi-waferforApple’ssupplychain.However,LandMarkdecidednottopursuethe3Dsensingopportunitiesatthattimebecausethegrossmarginofthebusiness,at30-40%,iswellbelowthecorporateaverageofabove50%.However,accordingtocompanyduringitslastanalystmeeting,ithasreviseditsstrategyandindicatedthatitwouldenterthisbusinessiftheopportunityarose.LandMarkhassaidpubliclythatitisnotinterestedinaggressivelycompetinginthismarket,butwouldliketoproveitsabilitytoproduceVCSELLDfor3DsensingapplicationstofutureLiDARcustomers.LEDbasedepi-wafercompaniessuchasEpistar(2448TT,Reduce):LEDchipmakersareanothergroupofpotentialepi-waferprovidersastheyarealsoinvolvedinthecompoundsemiconductorindustryandrunMOCVDastheirkeytool.LEDcompaniesarealsoontheradarofmanyglobalIDMslookingforcooperationopportunitiesgiventheirscaleandpriorexperiencewithMOCVDprocess.WealsothinktheLEDcompaniesenjoythemostattractivecoststructureastheyhavebeenthroughaverytoughindustrycycleandcouldhaveaveryleancoststructureandareveryeffectiveinkeepingcostsdown.However,webelievethekeychallengesfacingtheseLEDcompaniesarethetechnologybarriersinfabricatingVCSELlaserdiodecomparedtoLEDchips.Firstofall,blue-rayLEDchiparemadefromGaNinsteadofGaAs.Asaresult,LEDchipmakersdonothavethelatestknow-howinGaAs.AlthoughEpistarhastheknowledgeinGaAs,sinceitproducesthefour-elementLED,theknow-howintheinteractionofothermaterialsisalsoverydifferent.Secondly,thelayercountformanufacturingtheLEDismuchsmallerthanforthe3Dsensinglaserdiode(fewerthan10layersversusmorethan200layers).OurconversationswithindustryexpertshaveindicatedthatthechallengesforLEDcompaniestomeettherequirementofa3DsensingLDarestillhigh.Lastly,thereisaconcernforcurrent3DsensingLDprovidersaboutapotentialbusinessconflictinthefuture.MostoftheLEDchipmakershaveabusinessmodelinwhichtheycarryoutbothepi-waferfabricationandchipprocesses.ThisiscreatesdirectcompetitionbetweenthemandexistingsupplierssuchasLumentumorFinisar.FinisarandII-VIbothdoalltheirmanufacturingin-houseduetoconcernsabouttechnologyleakage.Lumentum,however,hasanoutsourcingbusinessmodel,andseparatestheepi-waferfabrication,chipprocess,andwaferacceptancetest(WAT)betweenvariousvendorstoavoidgivingonecompanyinsightintothewholetechnology.Webelievethisisacleverstrategytoavoidfosteringfuturecompetitors.Meanwhile,giventhecomplexstructureoftheepi-waferdesign(morethan200layersofcompoundsemiconductormaterialdeposited),thefabricationprocessisverydifficult.Asaresult,thecurrentepi-wafersuppliersforAppleFaceIDmoduleareallfromthelaserindustry,suchasLumentum/IQE,Finisar,andII-VI.Ourindustrysurveyindicatedthatitisstillverydifficultforothercompoundsemiconductorepi-wafervendors,suchasLED,tosuccessfullymatchthequalityoftheVCSELLDrequirementiftheyhavenopartnerstohelp.Nonetheless,hasEpistarindicatedthatithasalreadyconvertedtwoMOCVDinto6-inchcapacityfortheR&Dproductionandwilllikelytoconvertanotherseven6-inchMOCVDin2H18.Itcurrentlyhasacleanroomthatcouldfit13-14MOCVDifrequired.14

EQUITIES●SEMICONDUCTOR29January2018Sensitivityanalysison3DsensingcontributionWeconductasensitivityanalysisonthesignificantofthe3Dsensingepi-waferrevenueopportunityformajorepi-wafermakersinTaiwanbasedontheir2018erevenue.(Note:forEpistarandLandMark,weuseHSBCestimated2018revenue.ForVPEC,weuseBloombergconsensus2018erevenueestimateasabase.ForHLJ,weuse2017reportedrevenue,asthereisnoconsensusavailable.)Accordingtoouranalysis,10%of3Dsensingepi-waferrevenuein2019wouldtranslatetoonly1%ofEpistar’srevenuewhilethatwillaccountforaround8%ofrevenuetoLandMark.WehencebelievethecontributiontoEpistarwillbelimited.MoreMOCVDcapacityexpansionunderwayWhileitisstillunclearhowmanyMOCVDwillbeaddedfortheindustryin2018,weexpecttoseeexpansionatseveralkeyplayersoverthenext6-12monthsandthinkthereshouldbeenoughsupplyfortheindustry.Wethinktherearecurrentlyaround20-25MOCVDemployedbyIQE,andII-VI,andverysmallnumbersfromFinisarsupplyingiPhoneX3DsensingVCSELLDdemand.Basedonourearlierassumption,wethinkiPhonewillrequire32MOCVDin2018and40MOCVDin2019e,drivenbybothincreasingpenetrationbutoffsetbyimprovingproductionyieldrates.Wethinktheadditional18MOCVDofcouldbesupportedbythecapacityexpansionfromIQE,Finisar,II-VI,andalsonewcapacityexpansionfromnewentrantssuchasVPEC(additional6MOCVDin2018).Forthenon-Applesmartphonemarketof20-25MOCVDdemand,wethinktheexpansionfromamsandspillovereffectfromtheApplesupplychaincouldbeenoughtosupportthedemand.Potentialexpansionorfund-raisingplansfrommajorplayersFinisar:AppleannouncedinDecember2017thatithadreachedapurchaseagreementwithFinisarunderwhichitwillpurchaseatotalvalueofUSD390mproductsinacertainperiodoftime.Webelievethispurchaseagreementismainlyfocussedonthe3DsensingLD.Finisarindicatedthatitwillusepartofthefundtorestorea700,000square-footmanufacturingplantinTexastoproduceVCSELLDforthe3Dsensingmodules.AssumingFinisarusesUSD100mforMOCVDinvestment,wethinkFinisarcouldincreasetoaround20-25MOCVDoverthenexttwoyears.IQE:InNovember2017,IQEreportedthatitintendedtoraisearoundGBP9.5minnewcapitaltocapturemultiplehigh-growthmassmarketopportunities.ThefundwillallowIQEtoexpanditscapitalexpenditureprograminitsnewfoundry,withthepurchaseofupto40-60newMOCVDmachinesoverthenextthreetofiveyears.Itwillalsoenablethecompanytoacceleratethedevelopmentofnewproductsandtechnology.ams:AfteracquiringPrincetoninearly2017tocreateafullyautomatedcleanroomformicro-opticsensors,alongsidenewR&DandmanufacturinglinesforVCSELproduction,amssaidthatitintendedtoinvestatotalofEUR100matitsSingaporesitetoprepareforexpectedvolumeopportunitiesfrom2019onwards(companystatement,24July2017).ThecompanyisalsoexpandingitswafermanufacturingcapacityinUtica,NewYork,wherethefirstproductsareexpectedtorolloffthenewproductionlinein1H18(Observer-Dispatch,“Itisexpectedtobeoperationalbytheendof2017,withatargetforthefirstbatchesofwafersmadeattheplantinthefirsthalfof2018”,20April2016.)Also,afteracquiringHeptagonbackinOctober2016,amsbecamethelargestshareholderofHLJ.WeseescopeforamstoexpanditsSingaporefabwitha2,0006-inchwaferpermonthbyendof2018andamsmayexpandto6,0006-inchwaferpermonthbasedonitscurrentfabcleanroomspace.II-VI:II-VIacquireda6-inchepi-wafermakerKaiamLaser,atapriceofaroundUSD80minAugust2017andwillconverttheequipmenttoproduceVCSELLDepi-wafer.15

EQUITIES●SEMICONDUCTOR29January2018ValuationandrisksValuationmethodologyRiskstoourviewCurrentprice:OurtargetpriceofTWD460implies30x2018ePEand23x2019eKeydownsiderisks:(1)slower-than-expected100GswitchLandMarkTWD372.00PE.Althoughthemultipleseemsstretchedin2018e,the2019edemandin2018asglobaldatatrafficmaynotcontinueto3081TTtargetPEiswithinitshistoricalaveragerange,whichwethinkisfairgrowstrongly;and(2)risingcompetitionfromChineseTargetprice:TWD460.00giventhatwearepositiveonLandMark’slong-termgrowthoutlook.playersasanalternativesuppliertoreplaceLandMark.WeuseDCFasourvaluationmethodology,aswebelievethisbestBuyUp/downside:reflectsthecompany’slong-termgrowthpotential.InourDCF24%model,weassume20%medium-termgrowth,2%terminalgrowth,anda7.4%WACC(CoEat7.4%,costofdebtat2.5%,RFRat2.5%,ERPat4.6%,betaof1.1).Ourtargetpriceimpliesupsideof24%andwethereforeratethestockBuy.SamsonHung*|samson.hm.hung@hsbc.com.tw|+886266312863Currentprice:WebaseourtargetpriceofTWD24ona0.5x2018ePB,whichisKeyupsiderisks:faster-than-expectedcommercialisationEpistarTWD52.30theaverageoftwomultiples:(1)onestandarddeviationbelowtheofnewproductsandLEDsupplyremainingtightin2018.2448TThistoricalaverage(0.65x)and(2)thehistoricaltrough(0.36x),toTargetprice:TWD24.00reflectthefallingROEtrendbuttheslightlybetteroperatingstructureafterEpistarrationalizeditsoperations.OurTWD24targetpriceReduceUp/downside:implies54%downsideandwemaintainourReducerating.-54%SamsonHung*|samson.hm.hung@hsbc.com.tw|+886266312863Currentprice:Weuseasum-of-the-partsmethodologytovalueLGInnotek:Keydownsiderisks:(1)lower-than-expecteddualcameraLGInnotekKRW126,500(1)Fortheelectroniccomponentsunit,weapplyanunchanged5.5xadoptionrateiniPhone;(2)anaggressiveshiftinorder011070KS2018eEV/EBITDA(averageEV/EBITDAofthecompanyduringallocationtosecondorthirdsourcebyamajorcameraTargetprice:2012-13,whenthecomponentsmarginimproved,offsettinglossesmoduleclient;(3)adelayinaturnaroundinLEDearningsKRW190,000onLED).(2)Fortheautomotivecomponentssegment,weuseaduetolingeringoversupply;(4)aslower-than-expectedBuyUp/downside:DCFmodel,giventhatthisbusinessgeneratesstablecashflow,increaseinordersforautomotivecomponents.50%basedonlong-termordercontracts.Weassumea2.5%risk-freerateanda5.5%equityriskpremium.Weemployamarket-based1.0beta,resultinginan8.0%WACC.OurtargetpriceKRW190,000implies50%upside,werateLGIBuy.WillCho*|will.cho@kr.hsbc.com|+82237068765Currentprice:WederiveourtargetpriceofTWD4,200byapplyingaPEtargetofKeydownsiderisks:(1)weakerenddemand;(2)poorLarganTWD3,790.0020x(post-crisisaverage)to2018eEPSofTWD209.90.Ourshareexecution;and(3)strongercompetition.3008TTpricerepresents11%upsidetothelastclosingprice.WebelieveTargetprice:TWD4,200.00theworstisoverandratethestocktoBuyonthebackofpositiveprofitabilityimprovements,continuousspecupgrades,reducedBuyUp/downside:concernsonhybridlens,anditsmarketdominanceatanattractive11%valuation(c15x2019PE).BruceLu*|bruce.kl.lu@hsbc.com.tw|+886266312861Currentprice:WederiveourtargetpriceofTWD226byapplyingaPEmultipleofKeyupsiderisks:(1)strongerdemand;(2)weakerWinSemiTWD240.0018x,whichwebelieveisdeservedgivenstrongearningsCAGRofcompetition;(3)betterexecution.Keydownsiderisks:3105TT23%in2016-19e,to2018eEPSofTWD12.55.Westayontheside-(1)weakerdemand;strongcompetition;pooryields.Targetprice:TWD226.00linesasthecompany’ssharepricehasdoubledYTDandalreadyseemstobepricinginthepositives,thoughwethinkthesharepriceHoldUp/downside:mayseesupportfromthepositiveoutlook;retainHoldrating.-6%BruceLu*|bruce.kl.lu@hsbc.com.tw|+886266312861Currentprice:WederiveourtargetpriceofTWD134byapplyingaPEmultipleofKeyupsiderisks:fastergrowthofSemiTestorTurnkeyChromaATETWD167.5019x,whichwebelieveisdeservedgivenChroma’sstrongerandbusiness,anylarger-than-expectedcontributionfromnon-2360TTbroadergrowthdrivers,to2018eEPSofTWD7.03.Weratetheopincome(suchasMAS),oranybetter-than-expectedTargetprice:stockHoldandourtargetpriceimplies20%downsidetothecurrentgrowthinthecompany’scoreTestinstruments&ATETWD134.00shareprice.segment.Keydownsiderisks:Lumpinessinorderpatterns,HoldUp/downside:significantslowdowninTest,TurnkeyorAutomation-20%industries,oradelayinthegrowthofEV,battery,IoT,solarandLEDmarket.StevenPelayo|stevenpelayo@hsbc.com.hk|+8522822439116

EQUITIES●SEMICONDUCTOR29January2018ValuationmethodologyRiskstoourviewCurrentprice:Weprimarilyuseatargetcalendar2018ePEmultipleof15xtoKeydownsiderisks:(1)Near-termrisksincludepotentialAppleUSD171.11deriveourUSD193targetprice.Thelong-termhistoricalforwardPEmanufacturinghiccupsandweakerproductmiximpactingAAPLUSrangehasbeenbetween9xand16x.WebelieveusingamultipleatASP/margins.(2)Long-termthreatsincludeshiftstowardTargetprice:thehigherendofthehistoricalrangeisjustifiedgiven(1)resumptionmoreemergingmarketdemandwhereApple’spremiumUSD193.00ofiPhoneunitgrowth;(2)blendedASPincreasewithiPhoneandpricingcouldbeaheadwind.Also,theemergingmarketBuyUp/downside:Watch;(3)fast-growingcontributionfromServicesisgrowingfastconsumersmaynotrichlyvalueApple’secosystem,ifthe13%andhasveryhighmargins;and(4)strongfreecashflowandaloftyprimaryend-useistosimplygainaccesstootherplatformsnetcashbalance.With14%upside,weratethestockasBuyaswesuchasWeChatinChina.(3)CompetitionremainingarepositiveonthepotentialforanupsidetoconsensusforecastforintenseandrapidtechnologicalchangesindicatingthatiPhoneshipment,revenueandmargins.Applemustmaintainasteadycadencebyintroducinginnovativeproducts/features.(4)ManagingadiversedistributionchannelfromAppleRetailandtelecomcarrierstodistributorsandotherresellers.(5)Difficultyinreceivingcontinuedsupportfromthird-partysoftwaredevelopersforapplicationsandtherequiredsoftware.(6)IPprotectionandlegalresolutionsregardingpatentinfringementcases(e.g.,withQualcomm).(7)Worse-than-expectedchangesintaxlegislationaroundtheglobe.(8)Unfavourableglobalandregionaleconomicconditions.StevenPelayo|stevenpelayo@hsbc.com.hk|+85228224391Note:Pricedatcloseof25January2018*Employedbyanon-USaffiliateofHSBCSecurities(USA)Inc.andnotregistered/qualifiedpursuanttoFINRAregulationsSource:HSBCestimates17

EQUITIES●SEMICONDUCTOR29January2018DisclosureappendixAnalystCertificationThefollowinganalyst(s),economist(s),orstrategist(s)whois(are)primarilyresponsibleforthisreport,includinganyanalyst(s)whosename(s)appear(s)asauthorofanindividualsectionorsectionsofthereportandanyanalyst(s)namedasthecoveringanalyst(s)ofasubsidiarycompanyinasum-of-the-partsvaluationcertifies(y)thattheopinion(s)onthesubjectsecurity(ies)orissuer(s),anyviewsorforecastsexpressedinthesection(s)ofwhichsuchindividual(s)is(are)namedasauthor(s),andanyotherviewsorforecastsexpressedherein,includinganyviewsexpressedonthebackpageoftheresearchreport,accuratelyreflecttheirpersonalview(s)andthatnopartoftheircompensationwas,isorwillbedirectlyorindirectlyrelatedtothespecificrecommendation(s)orviewscontainedinthisresearchreport:SamsonHung,WillCho,BruceLu,StevenPelayo,andAnthonyLiaoImportantdisclosuresEquities:StockratingsandbasisforfinancialanalysisHSBCanditsaffiliates,includingtheissuerofthisreport(“HSBC”)believesaninvestor"sdecisiontobuyorsellastockshoulddependonindividualcircumstancessuchastheinvestor"sexistingholdings,risktoleranceandotherconsiderationsandthatinvestorsutilisevariousdisciplinesandinvestmenthorizonswhenmakinginvestmentdecisions.Ratingsshouldnotbeusedorreliedoninisolationasinvestmentadvice.Differentsecuritiesfirmsuseavarietyofratingstermsaswellasdifferentratingsystemstodescribetheirrecommendationsandthereforeinvestorsshouldcarefullyreadthedefinitionsoftheratingsusedineachresearchreport.Further,investorsshouldcarefullyreadtheentireresearchreportandnotinferitscontentsfromtheratingbecauseresearchreportscontainmorecompleteinformationconcerningtheanalysts"viewsandthebasisfortherating.From23rdMarch2015HSBChasassignedratingsonthefollowingbasis:Thetargetpriceisbasedontheanalyst’sassessmentofthestock’sactualcurrentvalue,althoughweexpectittotakesixto12monthsforthemarketpricetoreflectthis.Whenthetargetpriceismorethan20%abovethecurrentshareprice,thestockwillbeclassifiedasaBuy;whenitisbetween5%and20%abovethecurrentshareprice,thestockmaybeclassifiedasaBuyoraHold;whenitisbetween5%belowand5%abovethecurrentshareprice,thestockwillbeclassifiedasaHold;whenitisbetween5%and20%belowthecurrentshareprice,thestockmaybeclassifiedasaHoldoraReduce;andwhenitismorethan20%belowthecurrentshareprice,thestockwillbeclassifiedasaReduce.Ourratingsarere-calibratedagainstthesebandsatthetimeofany"materialchange"(initiationorresumptionofcoverage,changeintargetpriceorestimates).Upside/Downsideisthepercentagedifferencebetweenthetargetpriceandtheshareprice.Priortothisdate,HSBC’sratingstructurewasappliedonthefollowingbasis:Foreachstockwesetarequiredrateofreturncalculatedfromthecostofequityforthatstock’sdomesticor,asappropriate,regionalmarketestablishedbyourstrategyteam.Thetargetpriceforastockrepresentedthevaluetheanalystexpectedthestocktoreachoverourperformancehorizon.Theperformancehorizonwas12months.ForastocktobeclassifiedasOverweight,thepotentialreturn,whichequalsthepercentagedifferencebetweenthecurrentsharepriceandthetargetprice,includingtheforecastdividendyieldwhenindicated,hadtoexceedtherequiredreturnbyatleast5percentagepointsoverthesucceeding12months(or10percentagepointsforastockclassifiedasVolatile*).ForastocktobeclassifiedasUnderweight,thestockwasexpectedtounderperformitsrequiredreturnbyatleast5percentagepointsoverthesucceeding12months(or10percentagepointsforastockclassifiedasVolatile*).StocksbetweenthesebandswereclassifiedasNeutral.*Astockwasclassifiedasvolatileifitshistoricalvolatilityhadexceeded40%,ifthestockhadbeenlistedforlessthan12months(unlessitwasinanindustryorsectorwherevolatilityislow)oriftheanalystexpectedsignificantvolatility.However,stockswhichwedidnotconsidervolatilemayinfactalsohavebehavedinsuchaway.Historicalvolatilitywasdefinedasthepastmonth"saverageofthedaily365-daymovingaveragevolatilities.Toavoidmisleadinglyfrequentchangesinrating,however,volatilityhadtomove2.5percentagepointspastthe40%benchmarkineitherdirectionforastock"sstatustochange.18

EQUITIES●SEMICONDUCTOR29January2018Ratingdistributionforlong-terminvestmentopportunitiesAsof26January2018,thedistributionofallindependentratingspublishedbyHSBCisasfollows:Buy45%(27%oftheseprovidedwithInvestmentBankingServices)Hold42%(27%oftheseprovidedwithInvestmentBankingServices)Sell13%(18%oftheseprovidedwithInvestmentBankingServices)Forthepurposesofthedistributionabovethefollowingmappingstructureisusedduringthetransitionfromtheprevioustocurrentratingmodels:underourpreviousmodel,Overweight=Buy,Neutral=HoldandUnderweight=Sell;underourcurrentmodelBuy=Buy,Hold=HoldandReduce=Sell.Forratingdefinitionsunderbothmodels,pleasesee“Stockratingsandbasisforfinancialanalysis”above.Forthedistributionofnon-independentratingspublishedbyHSBC,pleaseseethedisclosurepageavailableathttp://www.hsbcnet.com/gbm/financial-regulation/investment-recommendations-disclosures.InformationregardingcompanysharepriceperformanceandhistoryofHSBCratingsandtargetpricesinrespectoflong-terminvestmentopportunitiesforthecompaniesthatarethesubjectofthisreportisavailablefromwww.hsbcnet.com/research.ToviewalistofalltheindependentfundamentalratingsdisseminatedbyHSBCduringthepreceding12-monthperiod,pleaseusethefollowinglinkstoaccessthedisclosurepage:ClientsofGlobalResearchandGlobalBankingandMarkets:www.research.hsbc.com/A/DisclosuresClientsofHSBCPrivateBanking:www.research.privatebank.hsbc.com/DisclosuresHSBC&AnalystdisclosuresDisclosurechecklistCompanyTickerRecentpricePricedateDisclosureAPPLEAAPL.O171.1126January20181,5,6,7LARGANPRECISION3008.TW3880.0026January20184,6,7Source:HSBC1HSBChasmanagedorco-managedapublicofferingofsecuritiesforthiscompanywithinthepast12months.2HSBCexpectstoreceiveorintendstoseekcompensationforinvestmentbankingservicesfromthiscompanyinthenext3months.3Atthetimeofpublicationofthisreport,HSBCSecurities(USA)Inc.isaMarketMakerinsecuritiesissuedbythiscompany.4Asof31December2017HSBCbeneficiallyowned1%ormoreofaclassofcommonequitysecuritiesofthiscompany.5Asof30November2017,thiscompanywasaclientofHSBCorhadduringthepreceding12-monthperiodbeenaclientofand/orpaidcompensationtoHSBCinrespectofinvestmentbankingservices.6Asof30November2017,thiscompanywasaclientofHSBCorhadduringthepreceding12-monthperiodbeenaclientofand/orpaidcompensationtoHSBCinrespectofnon-investmentbankingsecurities-relatedservices.7Asof30November2017,thiscompanywasaclientofHSBCorhadduringthepreceding12-monthperiodbeenaclientofand/orpaidcompensationtoHSBCinrespectofnon-securitiesservices.8Acoveringanalyst/shasreceivedcompensationfromthiscompanyinthepast12months.9Acoveringanalyst/soramemberofhis/herhouseholdhasafinancialinterestinthesecuritiesofthiscompany,asdetailedbelow.10Acoveringanalyst/soramemberofhis/herhouseholdisanofficer,directororsupervisoryboardmemberofthiscompany,asdetailedbelow.11Atthetimeofpublicationofthisreport,HSBCisanon-USMarketMakerinsecuritiesissuedbythiscompanyand/orinsecuritiesinrespectofthiscompany12Asof23January2018,HSBCbeneficiallyheldanetlongpositionofmorethan0.5%ofthiscompany’stotalissuedsharecapital,calculatedaccordingtotheSSRmethodology.13Asof23January2018,HSBCbeneficiallyheldanetshortpositionofmorethan0.5%ofthiscompany’stotalissuedsharecapital,calculatedaccordingtotheSSRmethodology.19

EQUITIES●SEMICONDUCTOR29January2018HSBCanditsaffiliateswillfromtimetotimeselltoandbuyfromcustomersthesecurities/instruments,bothequityanddebt(includingderivatives)ofcompaniescoveredinHSBCResearchonaprincipaloragencybasis.Analysts,economists,andstrategistsarepaidinpartbyreferencetotheprofitabilityofHSBCwhichincludesinvestmentbanking,sales&trading,andprincipaltradingrevenue.Whether,orinwhattimeframe,anupdateofthisanalysiswillbepublishedisnotdeterminedinadvance.Non-U.S.analystsmaynotbeassociatedpersonsofHSBCSecurities(USA)Inc.andthereforemaynotbesubjecttoFINRARule2241orFINRARule2242restrictionsoncommunicationswiththesubjectcompany,publicappearancesandtradingsecuritiesheldbytheanalysts.EconomicsanctionsimposedbytheEUandOFACprohibittransactingordealinginnewdebtorequityofRussianSSIentities.ThisreportdoesnotconstituteadviceinrelationtoanysecuritiesissuedbyRussianSSIentitiesonorafter16July2014andassuch,thisreportshouldnotbeconstruedasaninducementtotransactinanysanctionedsecurities.Fordisclosuresinrespectofanycompanymentionedinthisreport,pleaseseethemostrecentlypublishedreportonthatcompanyavailableatwww.hsbcnet.com/research.HSBCPrivateBankingclientsshouldcontacttheirRelationshipManagerforqueriesregardingotherresearchreports.Tofindoutmoreabouttheproprietarymodelsusedtoproducethisreport,pleasecontacttheauthoringanalyst.Additionaldisclosures1.Thisreportisdatedasat29January2018.2.Allmarketdataincludedinthisreportaredatedasatclose25January2018,unlessadifferentdateoraspecifictimeofdayisindicatedinthereport.3.HSBChasproceduresinplacetoidentifyandmanageanypotentialconflictsofinterestthatariseinconnectionwithitsResearchbusiness.HSBC"sanalystsanditsotherstaffwhoareinvolvedinthepreparationanddisseminationofResearchoperateandhaveamanagementreportinglineindependentofHSBC"sInvestmentBankingbusiness.InformationBarrierproceduresareinplacebetweentheInvestmentBanking,PrincipalTrading,andResearchbusinessestoensurethatanyconfidentialorpricesensitiveinformationishandledinanappropriatemanner.4.Youarenotpermittedtouse,forreference,anydatainthisdocumentforthepurposeof(1)determiningtheinterestpayable,orothersumsdue,underloanagreementsorunderotherfinancialcontractsorinstruments,(2)determiningthepriceatwhichafinancialinstrumentmaybeboughtorsoldortradedorredeemed,orthevalueofafinancialinstrument,or(3)measuringtheperformanceofafinancialinstrument.Production&distributiondisclosures1.Thisreportwasproducedandsignedoffbytheauthoron26January2018at10:48GMT.2.Toseewhenthisreportwasfirstdisseminated,pleaserefertothedisclosurepageavailableathttps://www.research.hsbc.com/R/34/nrJCb9z20

EQUITIES●SEMICONDUCTOR29January2018DisclaimerLegalentitiesasat30November2017Issuerofreport‘UAE’HSBCBankMiddleEastLimited,Dubai;‘HK’TheHongkongandShanghaiBankingCorporationLimited,HongHSBCSecurities(Taiwan)CorporationLimitedKong;‘TW’HSBCSecurities(Taiwan)CorporationLimited;"CA"HSBCSecurities(Canada)Inc.;HSBCBank,ParisBranch;13thFloor,333KeelungRoad,Sec.1,HSBCFrance;‘DE’HSBCTrinkaus&BurkhardtAG,Düsseldorf;000HSBCBank(RR),Moscow;‘IN’HSBCSecuritiesandTaipei,TaiwanCapitalMarkets(India)PrivateLimited,Mumbai;‘JP’HSBCSecurities(Japan)Limited,Tokyo;‘EG’HSBCSecuritiesEgyptTelephone:+886227228458SAE,Cairo;‘CN’HSBCInvestmentBankAsiaLimited,BeijingRepresentativeOffice;TheHongkongandShanghaiFax:+886227222056BankingCorporationLimited,SingaporeBranch;TheHongkongandShanghaiBankingCorporationLimited,SeoulWebsite:www.research.hsbc.comSecuritiesBranch;TheHongkongandShanghaiBankingCorporationLimited,SeoulBranch;HSBCSecurities(SouthAfrica)(Pty)Ltd,Johannesburg;HSBCBankplc,London,Madrid,Milan,Stockholm,TelAviv;‘US’HSBCSecurities(USA)Inc.,NewYork;HSBCYatirimMenkulDegerlerAS,Istanbul;HSBCMéxico,SA,InstitucióndeBancaMúltiple,GrupoFinancieroHSBC;HSBCBankAustraliaLimited;HSBCBankArgentinaSA;HSBCSaudiArabiaLimited;TheHongkongandShanghaiBankingCorporationLimited,NewZealandBranchincorporatedinHongKongSAR;TheHongkongandShanghaiBankingCorporationLimited,BangkokBranch;PTBankHSBCIndonesia;HSBCQianhaiSecuritiesLimitedThisdocumenthasbeenissuedbyHSBCSecurities(Taiwan)CorporationLimitedintheconductofitsTaiwanregulatedbusinessfortheinformationofitsinstitutionalandprofessionalcustomers.ItisnotintendedforandshouldnotbedistributedtoretailcustomersinTaiwan.Thisrecommendationmaterialisforreferenceonly.Investorsshouldcarefullyconsidertheirowninvestmentrisk.Investmentresultsaretheresponsibilityoftheindividualinvestor.HSBCSecurities(Taiwan)CorporationLimitedisregulatedbytheSecuritiesandFuturesBureau.AllenquiresbyrecipientsinTaiwanmustbedirectedtoyourHSBCcontactinTaiwan.IfthisreportisreceivedbyacustomerofanaffiliateofHSBC,itsprovisiontotherecipientissubjecttothetermsofbusinessinplacebetweentherecipientandsuchaffiliate.Thisdocumentisnotandshouldnotbeconstruedasanoffertosellorthesolicitationofanoffertopurchaseorsubscribeforanyinvestment.HSBChasbasedthisdocumentoninformationobtainedfromsourcesitbelievestobereliablebutwhichithasnotindependentlyverified;HSBCmakesnoguarantee,representationorwarrantyandacceptsnoresponsibilityorliabilityastoitsaccuracyorcompleteness.ExpressionsofopinionarethoseoftheResearchDivisionofHSBConlyandaresubjecttochangewithoutnotice.Fromtimetotimeresearchanalystsconductsitevisitsofcoveredissuers.HSBCpoliciesprohibitresearchanalystsfromacceptingpaymentorreimbursementfortravelexpensesfromtheissuerforsuchvisits.HSBCanditsaffiliatesortheirofficers,directorsandemployeesmayhavepositionsinanysecuritiesmentionedinthisdocument(orinanyrelatedinvestment)andmayfromtimetotimeaddtoordisposeofanysuchsecurities(orinvestment).HSBCanditsaffiliatesmayactasmarketmakerorhaveassumedanunderwritingcommitmentinthesecuritiesofcompaniesdiscussedinthisdocument(orinrelatedinvestments),maysellthemtoorbuythemfromcustomersonaprincipalbasisandmayalsoperformorseektoperforminvestmentbankingorunderwritingservicesfororrelatingtothosecompanies.HSBCResearchmaynotbedistributedtothepublicmediaorquotedorusedbythepublicmediawithouttheexpresswrittenconsentofHSBCSecurities(Taiwan)CorporationLimited.ReportswrittenbyTaiwan-basedanalystsonnon-TaiwanlistedcompaniesarenotconsideredrecommendationstobuyorsellsecuritiesunderTaiwanStockExchangeOperationalRegulationsgoverningsecuritiesfirmsrecommendingtradesinsecuritiestocustomersandassuchHSBCSecurities(Taiwan)CorporationLimitedmaynotexecutetransactionsforclientsinthesesecurities/instruments.IntheUKthisreportmayonlybedistributedtopersonsofakinddescribedinArticle19(5)oftheFinancialServicesandMarketsAct2000(FinancialPromotion)Order2005.TheprotectionsaffordedbytheUKregulatoryregimeareavailableonlytothosedealingwitharepresentativeofHSBCBankplcintheUK.HSBCSecurities(USA)Inc.acceptsresponsibilityforthisresearchreportpreparedbyitsforeignaffiliate.AllU.S.personsreceivingthisreportandwishingtoeffecttransactionsinanysecuritydiscussedhereinshoulddosowithHSBCSecurities(USA)Inc.intheUnitedStatesandnotwiththeforeignaffiliate,theissuerofthisreport.Note,however,thatHSBCSecurities(USA)Inc.isnotdistributingthisreportandhasnotcontributedtoorparticipatedinitspreparation.InKorea,thispublicationisdistributedbyeitherTheHongkongandShanghaiBankingCorporationLimited,SeoulSecuritiesBranch("HBAPSLS")orTheHongkongandShanghaiBankingCorporationLimited,SeoulBranch("HBAPSEL")forthegeneralinformationofprofessionalinvestorsspecifiedinArticle9oftheFinancialInvestmentServicesandCapitalMarketsAct(“FSCMA”).ThispublicationisnotaprospectusasdefinedintheFSCMA.Itmaynotbefurtherdistributedinwholeorinpartforanypurpose.BothHBAPSLSandHBAPSELareregulatedbytheFinancialServicesCommissionandtheFinancialSupervisoryServiceofKorea.InSingapore,thispublicationisdistributedbyTheHongkongandShanghaiBankingCorporationLimited,SingaporeBranchforthegeneralinformationofinstitutionalinvestorsorotherpersonsspecifiedinSections274and304oftheSecuritiesandFuturesAct(Chapter289)(“SFA”)andaccreditedinvestorsandotherpersonsinaccordancewiththeconditionsspecifiedinSections275and305oftheSFA.ThispublicationisnotaprospectusasdefinedintheSFA.Itmaynotbefurtherdistributedinwholeorinpartforanypurpose.TheHongkongandShanghaiBankingCorporationLimitedSingaporeBranchisregulatedbytheMonetaryAuthorityofSingapore.RecipientsinSingaporeshouldcontacta"HongkongandShanghaiBankingCorporationLimited,SingaporeBranch"representativeinrespectofanymattersarisingfrom,orinconnectionwiththisreport.InAustralia,thispublicationhasbeendistributedbyTheHongkongandShanghaiBankingCorporationLimited(ABN65117925970,AFSL301737)forthegeneralinformationofits“wholesale”customers(asdefinedintheCorporationsAct2001).Wheredistributedtoretailcustomers,thisresearchisdistributedbyHSBCBankAustraliaLimited(ABN48006434162,AFSLNo.232595).TheserespectiveentitiesmakenorepresentationsthattheproductsorservicesmentionedinthisdocumentareavailabletopersonsinAustraliaorarenecessarilysuitableforanyparticularpersonorappropriateinaccordancewithlocallaw.Noconsiderationhasbeengiventotheparticularinvestmentobjectives,financialsituationorparticularneedsofanyrecipient.ThispublicationisdistributedinNewZealandbyTheHongkongandShanghaiBankingCorporationLimited,NewZealandBranchincorporatedinHongKongSAR.InJapan,thispublicationhasbeendistributedbyHSBCSecurities(Japan)Limited.Itmaynotbefurtherdistributedinwholeorinpartforanypurpose.InCanada,thisdocumenthasbeendistributedbyHSBCSecurities(Canada)Inc.(memberIIROC),oritsaffiliates.TheinformationcontainedhereinisundernocircumstancestobeconstruedasinvestmentadviceinanyprovinceorterritoryofCanadaandisnottailoredtotheneedsoftherecipient.NosecuritiescommissionorsimilarregulatoryauthorityinCanadahasreviewedorinanywaypassedjudgmentuponthesematerials,theinformationcontainedhereinorthemeritsofthesecuritiesdescribedherein,andanyrepresentationtothecontraryisanoffence.IfyouareanHSBCPrivateBanking(“PB”)customerwithapprovalforreceiptofrelevantresearchpublicationsbyanapplicableHSBClegalentity,youareeligibletoreceivethispublication.Tobeeligibletoreceivesuchpublications,youmusthaveagreedtotheapplicableHSBCentity’stermsandconditions(“KRCTerms”)foraccesstotheKRC,andthetermsandconditionsofanyotherinternetbankingserviceofferedbythatHSBCentitythroughwhichyouwillaccessresearchpublicationsusingtheKRC.DistributionofthispublicationisthesoleresponsibilityoftheHSBCentitywithwhomyouhaveagreedtheKRCTerms.Ifyoudonotmeettheaforementionedeligibilityrequirementspleasedisregardthispublicationand,ifyouareacustomerofPB,pleasenotifyyourRelationshipManager.ReceiptofresearchpublicationsisstrictlysubjecttotheKRCTerms,whichcanbefoundathttps://research.privatebank.hsbc.com/–wedrawyourattentionalsototheprovisionscontainedintheImportantNotessectiontherein.©Copyright2018,HSBCSecurities(Taiwan)CorporationLimited,ALLRIGHTSRESERVED.Nopartofthispublicationmaybereproduced,storedinaretrievalsystem,ortransmitted,onanyformorbyanymeans,electronic,mechanical,photocopying,recording,orotherwise,withoutthepriorwrittenpermissionofHSBCSecurities(Taiwan)CorporationLimited.MCI(P)116/01/2018,MCI(P)126/02/2017[1072885]21

GlobalTelecoms,Media&TechnologyResearchTeamGlobalAsiaSpecialistSalesAnalyst,GlobalSectorHead,TelecomsAnalystJamesBritton+442079915503StephenHoward+442079916820YogeshAggarwal+912222681246james1.britton@hsbc.comstephen.howard@hsbcib.comyogeshaggarwal@hsbc.co.inKubilayYalcin+492119104880Analyst,GlobalSectorHead,TechnologyAnalystkubilay.yalcin@hsbc.deStevenCPelayo+85228224391VivekGedda+912261640693stevenpelayo@hsbc.com.hkvivekgedda@hsbc.co.inMylesMcMahon+85228224676mylesmacmahon@hsbc.com.hkAnalyst,GlobalSectorHead,Internet&AnalystE-commerceVikasAhuja+912233960690ChiTsang+85228222590vikasahuja@hsbc.co.inchitsang@hsbc.com.hkAnalystNealeAnderson+85229966716Europeneale.anderson@hsbc.com.hkAnalystNicolasCote-Colisson+442079916826Analystnicolas.cote-colisson@hsbcib.comBruceLu+886266312861bruce.kl.lu@hsbc.com.twAnalystAntoninBaudry+33156524325Analystantonin.baudry@hsbc.comSamsonHung+886266312863samson.hm.hung@hsbc.com.twAnalystChristopherJohnen+492119102852Analystchristopher.johnen@hsbc.deRickySeo+82237068777rickyjuilseo@kr.hsbc.comAnalystLuigiMinerva+442079916928Analystluigi.minerva@hsbcib.comRajivSharma+912222681239rajivsharma@hsbc.co.inAnalystOlivierMoral+33156524322Analystolivier.moral@hsbc.comDarpanThakkar+912261640695darpan.thakkar@hsbc.co.inAnalystAdamFox-Rumley+442079916819Analystadam.fox-rumley@hsbcib.comPiyushChoudhary+6566580607piyush.choudhary@hsbc.com.sgAmericasAnalystAnalystJenaHan+82237068772ChristopherARecouso+12125252279jenahan@kr.hsbc.comchristopher.a.recouso@us.hsbc.comAnalystAnalystWillCho+82237068765RonnyBerger,CFA+442079912750will.cho@kr.hsbc.comronny.berger@hsbc.comAnalystAnalystDarrylCheng+886266312864SunilRajgopal+12125250267darryl.tj.cheng@hsbc.com.twsunilrajgopal@us.hsbc.comAssociateWayneWang+85229149935GlobalEmergingMarkets(GEMs)wayne.n.wang@hsbc.com.hkAnalystHervéDrouet+442079916827Associateherve.drouet@hsbcib.comHeatherLi+85229966574heather.q.li@hsbc.com.hkEmergingEurope,MiddleEast&Africa(EMEA)AssociateAnalystKennethShim+82237068779ZiyadJoosub+27116764223kennyshim@kr.hsbc.comziyad.joosub@za.hsbc.comAssociateAnalystAngusLin+85229966584EricChang+97144236554angus.s.h.lin@hsbc.com.hkerichy.chang@hsbc.comAssociateAnthonyLiao+886266312865anthony.wc.liao@hsbc.com.twAssociateThurstonLee+886266312866thurston.jc.lee@hsbc.com.tw'