- 197.85 KB

- 2022-04-29 14:00:44 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

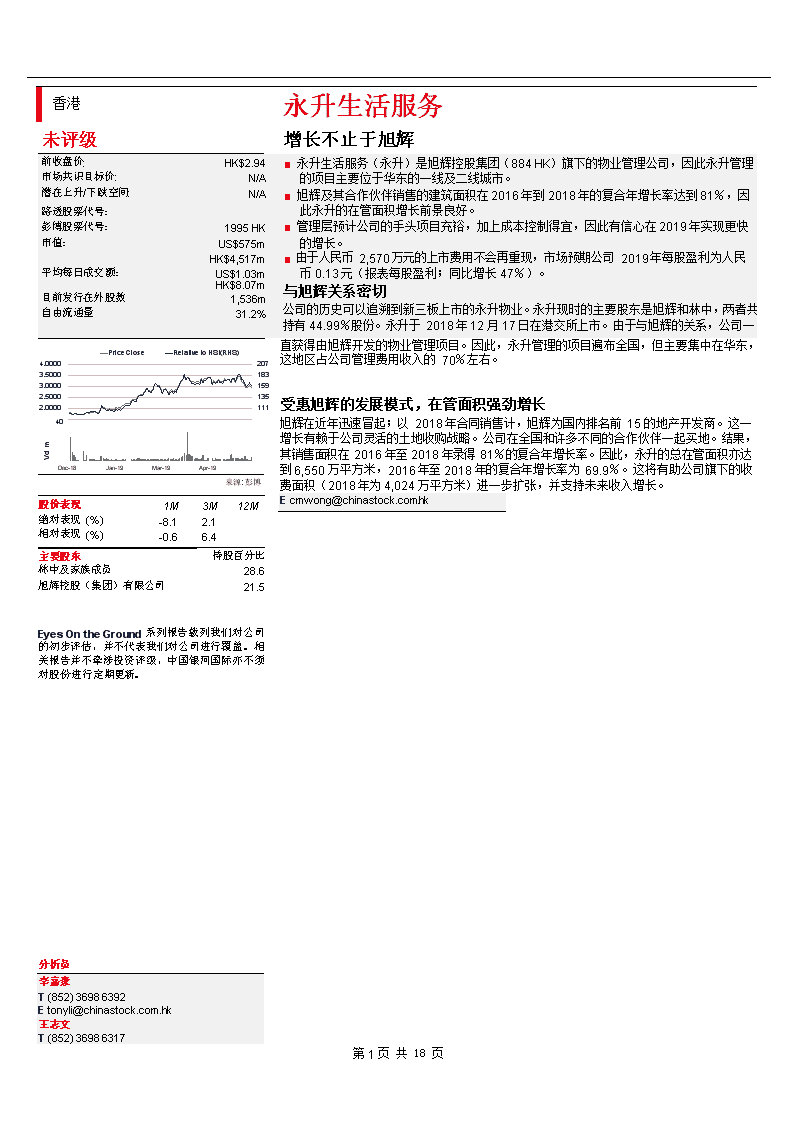

'香港永升生活服务未评级增长不止于旭辉前收盘价:HK$2.94■永升生活服务(永升)是旭辉控股集团(884HK)旗下的物业管理公司,因此永升管理市场共识目标价:N/A的项目主要位于华东的一线及二线城市。潜在上升/下跌空间:N/A■旭辉及其合作伙伴销售的建筑面积在2016年到2018年的复合年增长率达到81%,因路透股票代号:此永升的在管面积增长前景良好。彭博股票代号:1995HK■管理层预计公司的手头项目充裕,加上成本控制得宜,因此有信心在2019年实现更快市值:US$575m的增长。HK$4,517m■由于人民币2,570万元的上市费用不会再重现,市场预期公司2019年每股盈利为人民平均每日成交额:US$1.03m币0.13元(报表每股盈利;同比增长47%)。HK$8.07m与旭辉关系密切目前发行在外股数1,536m自由流通量31.2%公司的历史可以追溯到新三板上市的永升物业。永升现时的主要股东是旭辉和林中,两者共持有44.99%股份。永升于2018年12月17日在港交所上市。由于与旭辉的关系,公司一第18页共18页4.00003.50003.00002.50002.000040PriceCloseRelativetoHSI(RHS)207183159135111直获得由旭辉开发的物业管理项目。因此,永升管理的项目遍布全国,但主要集中在华东,这地区占公司管理费用收入的70%左右。受惠旭辉的发展模式,在管面积强劲增长旭辉在近年迅速冒起;以2018年合同销售计,旭辉为国内排名前15的地产开发商。这一增长有赖于公司灵活的土地收购战略。公司在全国和许多不同的合作伙伴一起买地。结果,其销售面积在2016年至2018年录得81%的复合年增长率。因此,永升的总在管面积亦达第18页共18页VolmDec-18Jan-19Mar-19Apr-19来源:彭博到6,550万平方米,2016年至2018年的复合年增长率为69.9%。这将有助公司旗下的收费面积(2018年为4,024万平方米)进一步扩张,并支持未来收入增长。第18页共18页股价表现1M3M12M绝对表现(%)-8.12.1相对表现(%)-0.66.4主要股东持股百分比林中及家族成员28.6旭辉控股(集团)有限公司21.5EyesOntheGround系列报告载列我们对公司的初步评估,并不代表我们对公司进行覆盖。相关报告并不牵涉投资评级,中国银河国际亦不须对股份进行定期更新。分析员李嘉豪T(852)36986392Etonyli@chinastock.com.hk王志文T(852)36986317Ecmwong@chinastock.com.hk第18页共18页

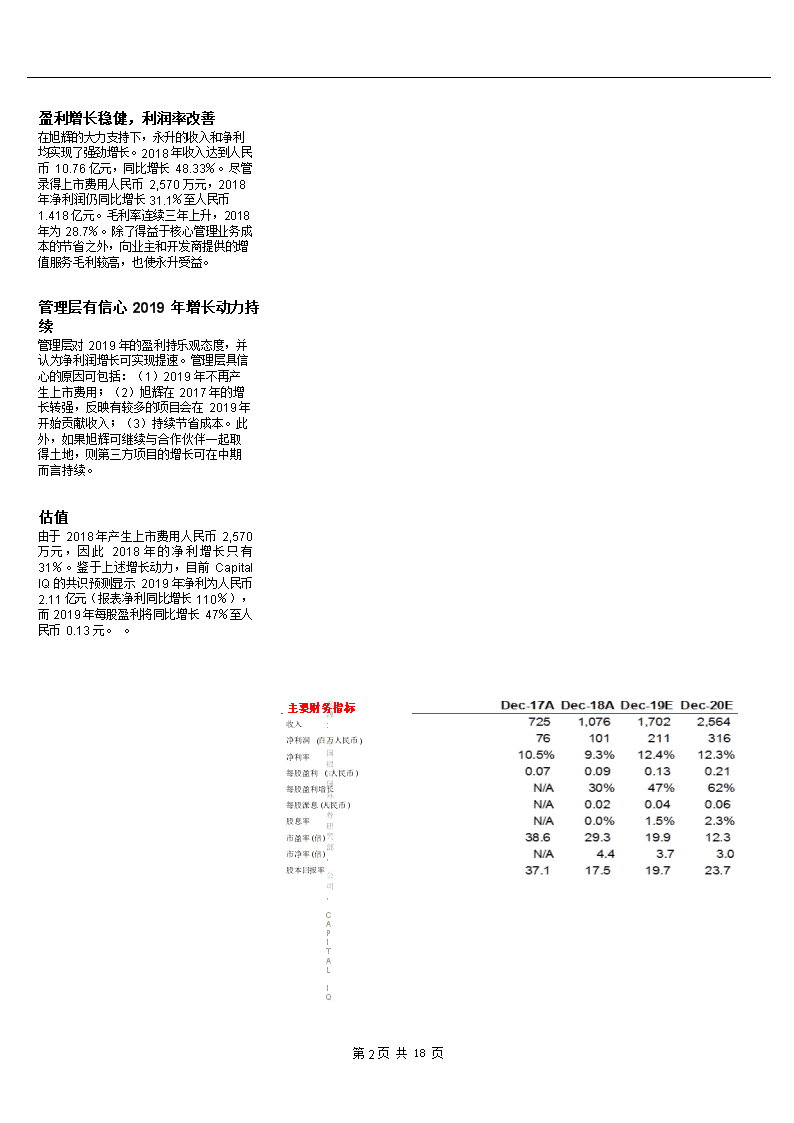

盈利增长稳健,利润率改善在旭辉的大力支持下,永升的收入和净利均实现了强劲增长。2018年收入达到人民币10.76亿元,同比增长48.33%。尽管录得上市费用人民币2,570万元,2018年净利润仍同比增长31.1%至人民币1.418亿元。毛利率连续三年上升,2018年为28.7%。除了得益于核心管理业务成本的节省之外,向业主和开发商提供的增值服务毛利较高,也使永升受益。管理层有信心2019年增长动力持续管理层对2019年的盈利持乐观态度,并认为净利润增长可实现提速。管理层具信心的原因可包括:(1)2019年不再产生上市费用;(2)旭辉在2017年的增长转强,反映有较多的项目会在2019年开始贡献收入;(3)持续节省成本。此外,如果旭辉可继续与合作伙伴一起取得土地,则第三方项目的增长可在中期而言持续。估值由于2018年产生上市费用人民币2,570万元,因此2018年的净利增长只有31%。鉴于上述增长动力,目前CapitalIQ的共识预测显示2019年净利为人民币2.11亿元(报表净利同比增长110%),而2019年每股盈利将同比增长47%至人民币0.13元。。主要财务指标收入净利润(百万人民币)净利率每股盈利(人民币)每股盈利增长每股派息(人民币)股息率市盈率(倍)市净率(倍)股本回报率来源:中国银河国际证券研究部,公司,CAPITALIQ第18页共18页

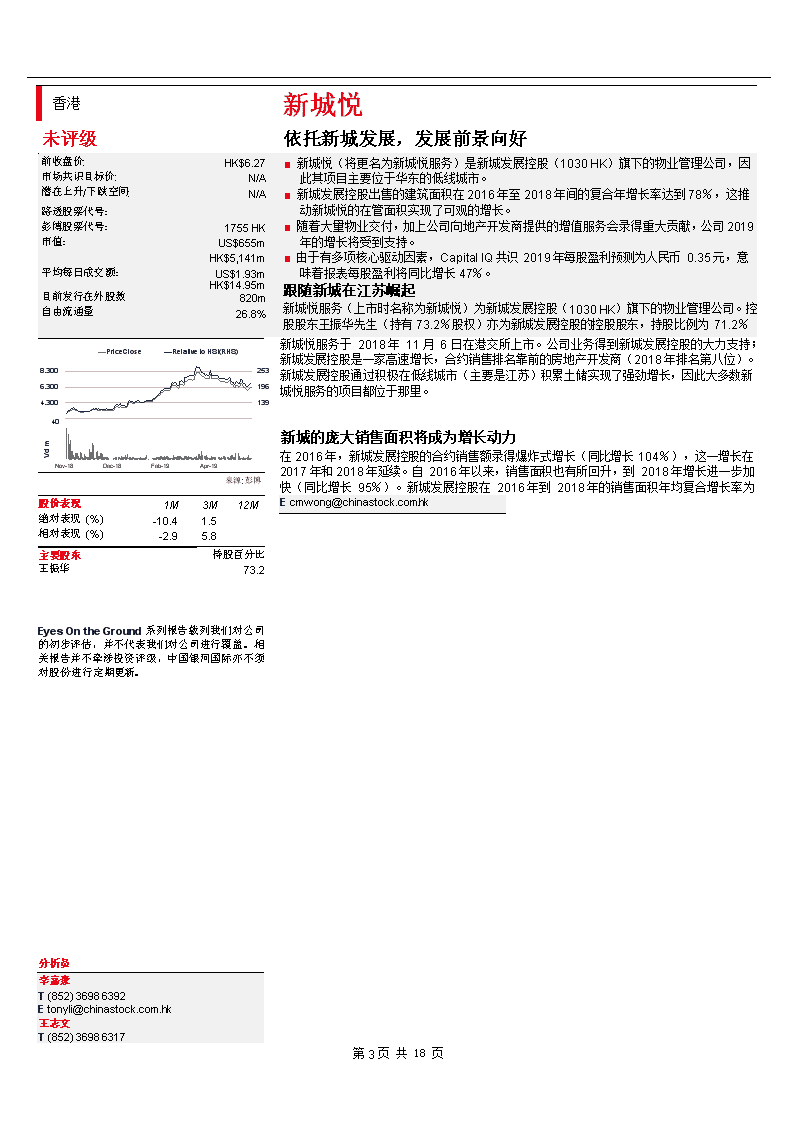

香港新城悦未评级依托新城发展,发展前景向好前收盘价:HK$6.27■新城悦(将更名为新城悦服务)是新城发展控股(1030HK)旗下的物业管理公司,因市场共识目标价:N/A此其项目主要位于华东的低线城市。潜在上升/下跌空间:N/A■新城发展控股出售的建筑面积在2016年至2018年间的复合年增长率达到78%,这推路透股票代号:动新城悦的在管面积实现了可观的增长。彭博股票代号:1755HK■随着大量物业交付,加上公司向地产开发商提供的增值服务会录得重大贡献,公司2019市值:US$655m年的增长将受到支持。HK$5,141m■由于有多项核心驱动因素,CapitalIQ共识2019年每股盈利预测为人民币0.35元,意平均每日成交额:US$1.93m味着报表每股盈利将同比增长47%。HK$14.95m跟随新城在江苏崛起目前发行在外股数820m自由流通量26.8%新城悦服务(上市时名称为新城悦)为新城发展控股(1030HK)旗下的物业管理公司。控股股东王振华先生(持有73.2%股权)亦为新城发展控股的控股股东,持股比例为71.2%第18页共18页8.3006.3004.300PriceCloseRelativetoHSI(RHS)253196139新城悦服务于2018年11月6日在港交所上市。公司业务得到新城发展控股的大力支持;新城发展控股是一家高速增长,合约销售排名靠前的房地产开发商(2018年排名第八位)。新城发展控股通过积极在低线城市(主要是江苏)积累土储实现了强劲增长,因此大多数新城悦服务的项目都位于那里。第18页共18页Volm40Nov-18Dec-18Feb-19Apr-19来源:彭博新城的庞大销售面积将成为增长动力在2016年,新城发展控股的合约销售额录得爆炸式增长(同比增长104%),这一增长在2017年和2018年延续。自2016年以来,销售面积也有所回升,到2018年增长进一步加快(同比增长95%)。新城发展控股在2016年到2018年的销售面积年均复合增长率为第18页共18页股价表现1M3M12M绝对表现(%)-10.41.5相对表现(%)-2.95.8主要股东持股百分比王振华73.2EyesOntheGround系列报告载列我们对公司的初步评估,并不代表我们对公司进行覆盖。相关报告并不牵涉投资评级,中国银河国际亦不须对股份进行定期更新。分析员李嘉豪T(852)36986392Etonyli@chinastock.com.hk王志文T(852)36986317Ecmwong@chinastock.com.hk77.5第18页共18页

%,远高于其他高排名的开发商。因此,新城悦的在管面积也于2018年开始加速增长,同比增长66%至1.122亿平方米,2016年至2018年的复合年增长率为53%。因此当新城发展控股开发的项目在未来交付,新城悦旗下收费的在管面积(2018年为4,290万平方米)将将会增长。整体利润率也在提高在新城发展控股的大力支持下,新城悦2018年的收入和净利均实现了强劲增长。2018年公司收入达到人民币11.5亿元,同比增长32.7%。凭借经营杠杆,2018年净利同比大幅增长105%至人民币1.5亿元(尽管录得上市费用人民币2,940万元)。这可归因于利润率的扩张。毛利率略微上升1.5个百分点至29.5%,净利率扩大4.6个百分点至13.1%。管理层对2019年增长前景感到乐观管理层对公司2019年的增长潜力保持正面看法。除了庞大的销售面积将成为创造收入的在管面积,公司也目标提升整体利润率:(1)由于公司调整价格以改善利润率,向开发商提供的增值服的利润会增加;(2)核心管理业务的利润率改善。估值2018年,公司产生上市费用人民币2,940万元,但2018年的净利增长仍然强劲。根据CapitalIQ的共识预测,市场现预计公司2019年增长势头将持续,共识净利润/每股盈利预测达到人民币2.15亿元/0.35元,同比增长43%/47%(基于报表数据)。主要财务指标收入净利润(百万人民币)净利率每股盈利(人民币)每股盈利增长市盈率(倍)市净率(倍)股本回报率来源:公司,CAPITALIQ第18页共18页

Figure1:Netprofitofpropertymanagersin2018:adichotomyforsmallplayers1000200%923900801800150%700600100%50048548340035350%3002001500%1011007870540-50%CGServicesA-LivingColourLifeGreentownServiceCOPLXingchengyueEverSunshineAoyuanHealthlyLifeBinjiangServiceKaisaPropertyNP(2018,RMBm)YoY(%;RHS)SOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERGChinaPropertyManagementLowbase,highgrowth:emergingpropertymanagers■Managerswithstrongparentscouldexperiencerobustgrowthin2019E–2020E.■WeexpectcertainnewlylistedpropertymanagerstoexperiencehighgrowthforatSummaryvaluationmetricsleast2–3yearsthankstoarelativelylowbase.P/E(x)Dec-18ADec-19FDec-20F■Value-addedservicestodeveloperscouldbeacriticalcomponentformeetinggrowthA-LivingServices15.5912.9211.38expectations,sotheywarrantattention.ColourLifeServicesGroup10.348.497.04■Small-capssuchasEverSunshine[1995.HK;NR]andXinchengyue[1775.HK,NR]CountryGardenServices36.3130.9723.05shouldbeputontheradarastheirearningsgrowthcouldbehighin2019E–2020E.P/BV(x)Dec-18ADec-19FDec-20FA-LivingServices2.292.131.90ColourLifeServicesGroup1.601.431.23CountryGardenServices15.047.025.65DividendYieldDec-18ADec-19FDec-20FA-LivingServices3.13%3.09%3.52%ColourLifeServicesGroup3.93%4.65%5.68%CountryGardenServices0.62%0.81%1.08%Smallerplayerslikelytoenjoystrongresultsin2018–2020EIntheChinapropertymanagementsector,mostpropertymanagersrecordedgoodearningsgrowthin2018,andsomeachieved>30%YoYgrowthinEPS.TheFY2018earningsofcertainsmallerplayersnotunderourexistingcoveragewereevenstronger,thanksto(1)arelativelysmallbase;(2)goodorganicgrowthwiththesupportofawell-knownparent;and(3)goodexecution.Weexpectthismomentumtobesustainedin2019Eand2020E.Twogrowthenginesinthenearfuture,especiallyin2019E(1)GFAgrowth:Ittypicallytakes2–3yearsforcontractedsalesfordeveloperstotranslateintorevenue-generatingGFAforpropertymanagers.Therefore,weexpectpropertymanagerstobenefitfromtheirassociateddevelopershavingstronggrowthincontractedsalesin2016–2017.(2)Value-addedservices:Ifthedeveloperscontinuetorecordstrongpropertysalesin2019E,thiswillprovidesupportforthevalue-addedservicessegmentofpropertymanagersin2019E.ManagementconfidentinachievingstronggrowthBasedonourrecentdiscussionswiththeseniormanagementofdifferentpropertymanagers,mostofthemconfirmedourview.Theyarealsoconfidentinachievingstronggrowthin2019E.Thosebackedbyasolidpropertydeveloperareconfidentthatleveragingthebrandnameoftheirassociateddeveloperscanhelpthemwinmorecontractsfromthird-partydevelopers,andevencloseM&Adeals.Smallerplayershaveissues,butnotabigconcernintheneartermHowever,wenotethatcertaininvestorsarestillingholdinga“waitandsee”attitudetowardssmaller,newlylistedmanagers.Inadditiontotheirshortlistinghistory,investorsmayhaveconcernsabouttherevenuegrowthofvalue-addedservicestodevelopers.Thisdependsonthelandbankofthedevelopers,sosustainabilitymaybeaquestionforsmallerplayers.Also,itwillalsobemoredifficultforthemtoexecuteacquisitionsthanforbiggerplayers,sincethefundsraisedduringtheIPOprocesswerealsosmaller.FindingthenextemergingpropertymanagersWereiterateourinvestmentthesisthatastrongparentispreferredinthissector.ThisisoneofthekeyreasonswepreferA-Living[3319.HK;BUY]andCountryGardenServices[6098.HK;BUY].Forinvestorswhoprefersmall-capexposure,certainstockscouldbeputontheirradar,suchas(1)EverSunshine[1995.HK;NR],whichisbackedbyCIFI[884.HK],and(2)Xinchengyue[1775.HK,NR,toberenamedS-EnjoyService],whichisbackedbyFutureLand[1030.HK].Theystillenjoyavaluationadvantagecomparedwithplayerswithalongerlistingtrackrecord(Figure6).AnalystsTonyLiT(852)36986392Etonyli@chinastock.com.hkWongChiManT(852)36986317第18页共18页

Ecmwong@chinastock.com.hk第18页共18页

Findingtheemergingleaders2019:likelyahoneymoonformanypropertymanagers2018:impressivegrowthinbothtopandbottomlinesManypropertymanagersachievedgoodresultsinFY2018intermsofbothrevenueandnetprofit.Ingeneral,theresultswereinlinewithinvestors’expectations.Althoughthesectorencounteredamajorcorrectioninlate-2018duetoconcernsaboutpoliciesrelatedtosocialsecuritypayments,thelistedcompanieswereresilientindemonstratingtheircompliancewithlocalregulations.Governmentclarificationandthesubsequentrelaxationoftheregulationshelpedthesector’svaluationrecoverinearly2019.Goingforwardinmid-2019,webelievethesectorwillcontinuetobedrivenbyfundamentalsandthatstockpickingwillmatter.Mostpropertymanagersrecordedgoodearningsgrowthin2018,andsomeachieved>30%YoYgrowthinEPS.TheFY2018earningsforcertainsmallerplayersnotunderourexistingcoveragecouldbeevenstronger,thanksto:(1)theirrelativelysmallbase;(2)goodorganicgrowthwiththesupportofawell-knownparent;and(3)goodexecution.Figure2:Revenueofmajorlistedpropertymanagersin20187,0006,710120%6,0005,0004,675100%4,0003,6493,61480%60%3,0002,0001,1501,07689640%20%GreentownServiceCGServicesCOPLColourLifeA-LivingXingchengyueEverSunshineKaisaPropertyAoyuanHealthlyLifeBinjiangServiceSOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERG第18页共18页

Figure3:Netprofitofmajorlistedpropertymanagersin2018923900801700600500485483100%40035350%3002001500%101787054CGServicesA-LivingColourLifeGreentownCOPLXingchengyueEverSunshineServiceAoyuanHealthlyLifeBinjiangServiceKaisaPropertySOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERGFigure4:Revenueandnetprofitofmajorpropertymanagers(2016–2018)GreentownColourLifeCOPLA-LivingCGServicesXingchengyueEverSunshineKaisaPropertyAoyuanServiceHealthlyLife2869HK1778HK2669HK3319HK6098HK1755HK1995HK2168HK3662HKRevenue(RMBm)FY20163,7221,3422,9521,2452,358573480539265FY20175,1401,6292,7961,7613,122866725669436FY20186,7103,6143,6493,3774,6751,1501,076896619Revenue-YoYFY201627.5%62.2%38.5%33.2%41.0%43.3%43.7%12.8%47.9%FY201738.1%21.4%-5.3%41.5%32.4%51.1%51.1%24.1%64.2%FY201830.5%121.9%30.5%91.8%49.8%32.7%48.3%33.9%41.9%NetProfit(RMBm)FY201628618821316132443345841FY201738732125529040273767170FY20184834853538019231501015478NetProfit-YoYFY201644.3%11.5%116.9%147.3%47.1%95.1%115.9%0.7%52.3%FY201735.7%70.8%20.1%80.3%23.9%69.4%127.5%22.9%70.1%FY201824.7%51.3%38.2%176.5%129.8%104.9%31.5%-24.3%12.0%SOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERG第18页共18页

Managementconfidentinachievingstronggrowthin2019Whileweexpectmanypropertymanagerstocontinuetoenjoyfundamental-drivenhighgrowthin2019E,weexpectthegrowthratetostarttovaryforcertainmanagers.Somelargermanagerswillcontinuetoenjoyhighgrowththankstothesupportoftheirassociateddevelopers,butsomelargerplayersmayfaceaslowdownintheorganicgrowthratebecauseofahighbase.Ifinvestorsprefertoseekhigh-growthstocks,thentheymayconsidercertainsmallerplayers.Weexpect2019Etocontinuetobeanotheryearforachievinghighgrowthforcertainsmallerplayersforseveralreasons:(1)GFAgrowth:Asaruleofthumb,ittypicallytakes2–3yearsfordevelopers’contractedsalestotranslateintorevenue-generatingGFAforpropertymanagers.Therefore,weexpectpropertymanagerstobenefitfromtheirassociateddevelopershavingstronggrowthincontractedsalesin2016–2017.(2)Value-addedservices:Ifthedeveloperscontinuetorecordstrongpropertysalesin2019E,thiswillalsoprovidesupportforthevalue-addedservicessegmentofpropertymanagersin2019E.Findingthehighachieversin2019:lookingatGFAsoldTopickpropertymanagerslikelytoexperiencehighgrowthin2019E,webelievetheperformanceoftheirassociateddevelopersshouldbeexamined.WeconsidertheGFAsoldbythedeveloperstobeabetterindicatoroftheirassociatedpropertymanagers’futureGFAgrowththantheactualamountofcontractedsales.SomeinvestorsmayhavetheperceptionthatstrongcontractedsalesmayindicatestrongGFAgrowth.Whilethisisgenerallytruemostofthetime,itdoesnotapplytocertainscenarios.Forexample,COLI[688.HK]hadstrongcontractedsalesin2018(+33.5%YoY),buttheGFAsoldgrewbyonly10.5%YoYbecauseCOLIfocusedonacquiringlandbanksinTier1–2citiesandbenefitedfromrisingpropertypricesthere.ThisindicatesthatGFAgrowthofCOPL[2669.HK]willberelativelymildcomparedtoitspeers’.Figure5:Contractedsalesofthetop15propertydevelopersinChina(note:certainfiguresmaydifferfromtheofficialfiguresannouncedduetodifferentreportingstandards)DeveloperTickerContractedSales(RMBbn)Sales-YoYGFASold(millionsq.m.)GFA-YoY2016201720182017201820162017201820172018CountryGarden2007HK30955072978.0%32.5%37.860.277.359.0%28.5%Vanke2202HK/000002CH36252460744.6%15.8%27.635.240.227.7%14.1%Evergrande3333HK37351355137.5%7.4%44.751.652.415.5%1.5%Sunac1918HK150362460141.3%27.1%7.321.430.2195.1%40.8%PolyRealEstate600048CH22031540543.0%28.6%16.622.927.237.4%18.7%GreenlandHoldings600606CH25130438121.0%25.3%20.224.635.722.2%45.1%COLI688HK1932012694.6%33.5%13.414.816.310.5%10.5%FutureLand1030HK6512622193.7%75.5%5.89.318.161.4%95.2%CRLand1109HK10815121140.0%39.3%7.89.712.124.0%24.6%Longfor960HK8615620181.8%28.6%5.910.212.572.2%21.7%Shimao813HK6810117648.3%74.3%4.96.010.723.0%76.2%ChinaMerchantsShekou001979CH7411317153.2%51.4%4.75.58.218.3%47.0%ChinaFortune600340CH12015416828.2%9.2%9.89.915.41.3%55.8%SunshineCity000671CH499216387.9%77.9%3.56.612.486.7%87.9%CIFI884HK6510415259.2%46.2%3.76.29.668.5%53.9%2018Top15Sub-total2,4933,7664,86451.1%29.1%213.6294.2378.137.7%28.5%SOURCES:CGISRESEARCHESTIMATES,COMPANYDATA,CRIC第18页共18页

Inouranalysis,wenotethatforthetop15developers(intermsofcontractedsales)in2018,FutureLand[1030.HK]andCIFI[884HK]hadrelativelyhighgrowthintermsofGFAsoldin2017and2018.ThiswilltranslateintohigherGFAgrowthin2019Efortheirassociatedpropertymanagers,Xinchengyue[1755.HK]andEverSunshine[1995.HK],inourview.WealsoexpectCountryGardenServices[6098.HK]andA-Living[3319.HK]tobenefitfromtheirstrongassociateddevelopers.Smallerplayershaveissues,butnotamajorconcernintheneartermWenotethatcertaininvestorsstillholda“waitandsee”attituderegardingsmaller,newlylistedmanagers.Asidefromtheirshortlistinghistory,webelievetherearetwomajorkeyconcernsfacedbythesesmallerplayers.SustainabilityandrelianceonconnectedpartiesInvestorsmayhaveconcernsabouttherevenuegrowthofvalue-addedservicestodevelopers.Thisrevenuedependsonthelandbankoftherelevantdevelopers,anditcouldberelatedtotheconnectedparties(i.e.theassociateddevelopers).Therefore,sustainabilitymaybeaquestionforsmallerplayers.FundingacquisitionsassmallerplayersItwillalsobemoredifficulttoexecuteacquisitionscomparedtobiggerplayers,sincethefundsraisedduringtheIPOprocesswerealsosmaller.Inrecentcases,certaincompaniesmaypurchasecompaniesownedbyconnectedparties.Thisagainmaycreatesomeconcernsaboutsustainability.However,wedonotseetheseasmajorriskstonear-termearningsgrowth.Therecouldbewaystotackletheseissuesinthemediumtermifmanagedproperly.Forexample,thesmallerplayerscouldbecomemajorplayersinthemarketandgainmoreprojectsfromotherdeveloperswiththeirbrandname.Figure6:Peercomparison(note:thevaluationisbasedonCapitalIQconsensus)CompanyTickerTradingCurrencyPriceMktCapHK$mLTMPER(x)2019E2020ELTMEV/EBITDA2018E2019EPBR(x)2018ROE(%)LTMCountryGardenServicesHoldingsCompanyLimited6098HKHKD15.4841,31237.2228.9922.9531.6122.1715.9915.0348.26A-LivingServicesCo.,Ltd.3319HKHKD10.9214,56015.5211.979.398.275.584.392.3623.22GreentownServiceGroupCo.Ltd.2869HKHKD5.7515,97229.0223.7017.7522.2714.5710.906.0221.19ChinaOverseasPropertyHoldingsLimited2669HKRMB3.6511,99729.8423.3419.0718.0213.5411.0310.7140.83ColourLifeServicesGroupCo.,Limited1778HKUSD4.465,92610.348.646.855.595.384.701.6615.32EverSunshineLifestyleServicesGroupLimited1995HKHKD2.944,51729.1719.8712.3017.7310.336.404.3117.47XinchengyueHoldingsLimited1755HKHKD6.275,14123.1515.7510.9416.18N/AN/A5.3430.91AoyuanHealthyLifeGroupCompanyLimited3662HKHKD4.012,91221.2918.5512.1519.4713.318.5214.7165.96SimpleAverage22.7617.2312.2615.408.516.137.3534.10SOURCES:CGISRESEARCH,COMPANYDATA,CAPITALIQ第18页共18页

HongKongEverSunshineLifestyleNONRATEDGrowingbeyondCIFICurrentprice:HK$2.94■EverSunshine(ES)isapropertymanagersupportedbyCIFI(884HK),sotheConsensusTgtPrice:N/AprojectsESmanagesarelocatedmainlyinTier1–2citiesineasternChina.Up/downside:N/A■GFAsoldbyCIFIanditspartnersachievedaCAGRof81%from2016to2018,leadingtopromisingGFAgrowthforES.Reuters:■Managementisconfidentinachievingfastergrowthin2019E,thankstoasolidprojectBloomberg:1995HKpipelineandefficientcostcontrol.Marketcap:US$575m■AsthelistingexpensesofRMB25.7mwillnotbeincurredagain,themarketisHK$4,517mexpecting2019EEPStobeRMB0.13(+47%YoY,onareportingbasis).Averagedailyturnover:US$1.03mCloserelationshipwithCIFIHK$8.07mCurrentshareso/s:1,536mThehistoryofEScanbetracedbacktoYongshengProperty,apropertymanagerlistedFreefloat:31.2%ontheNEEQ.ThemajorshareholdersofESnowareCIFIandLinZhong,whichtogetherholda44.99%stake.ESwaslistedontheHKExon17Dec2018.BecauseofitsEyesontheGroundLifestyles│HongKong│May29,2019第18页共18页PriceCloseRelativetoHSI(RHS)4.0000207relationshipwithCIFI,ithassecuredmanagementprojectsdevelopedbyCIFI.ProjectsmanagedbyESarethereforenationwide,butaremostlyconcentratedineasternChina,whichaccountsfor~70%ofthemanagementfeesearned.第18页共18页3.50003.00002.50002.0000Volm40Dec-18Jan-19Mar-19Apr-19183159135111StrongGFAgrowththankstotheCIFIdevelopmentmodelCIFIhasrapidlyemergedasaTop-15developerintermsofcontractedsalesin2018.Theriseisattributedtoitsresilientlandacquisitionstrategy.Itacquiredlandnationwidewithmanydifferentpartners.Asaresult,itsGFAsoldachievedaCAGRof81%between2016and2018.Therefore,ES’stotalcontractedGFAreached65.5msqm,representing第18页共18页Source:BloombergaCAGRof69.9%between2016and2018.Thiswillhelpitsrevenue-bearingGFAunder第18页共18页Priceperformance1M3M12MAbsolute(%)-8.12.1Relative(%)-0.66.4management(40.24msqmin2018)growfurther,supportingfuturerevenuegrowth.第18页共18页Majorshareholders%heldLinZhong&Family28.6CIFIHOLDINGS(GROUP)CO.LTD21.5ThisEyesOntheGroundreportrepresentsapreliminaryassessmentofthesubjectcompany,anddoesnotrepresentinitiationintoCGI"scoverageuniverse.ItdoesnotcarryinvestmentratingsandCGIdoesnotcommittoregularupdatesonanongoingbasis.SolidearningsgrowthwithmarginimprovementWithstrongsupportfromCIFI,ESachievedstronggrowthinbothtopandbottomlines.RevenuereachedRMB1,076min2018,up48.33%YoY.Netprofitin2018wasup31.1%YoYtoRMB141.8mdespitelistingexpensesofRMB25.7m.ItsGPMexpandedfor3consecutiveyearsto28.7%in2018aswell.Inadditiontocostsavingsinitscoremanagementbusiness,ESbenefitedfromthehigh-marginvalue-addedservicesitprovidestobothpropertyownersanddevelopers.Managementconfidentaboutsustainingmomentumin2019Managementisupbeatabout2019earningsandmaintainsthatnetprofitgrowthcouldaccelerate.Somereasonsforthisconfidencecouldbe(1)nomorelistingexpensesincurredin2019;(2)alargeportionofprojectsstartingtocontributerevenuein2019,assuggestedbytheuptickinCIFI’sgrowthin2017;and(3)continuedcostsavings.Also,thegrowthfromthird-partyprojectscanbesustainedinthemediumrun,ifCIFIcancontinuetoacquirelandplotswithitspartners.ValuationIn2018,listingexpensesofRMB25.7mwereincurred,sonetprofitgrowthin2018wasdraggeddownto31%.Giventhegrowthdriversmentionedabove,themarketisnowexpecting2019EnetprofittobeRMB211m(+110%YoY,onareportingbasis),while2019EEPSwillbeup47%YoYtoRMB0.13,accordingtoCapitalIQconsensus..第18页共18页AnalystsTonyLiT(852)36986392Etonyli@chinastock.com.hkWongChiManT(852)36986317Ecmwong@chinastock.com.hkFinancialSummaryDec-17ADec-18ADec-19EDec-20ERevenue7251,0761,7022,564NetProfit(Rmbm)76101211316NetMargin10.5%9.3%12.4%12.3%EPS(Rmb)0.070.090.130.21EPSGrowthN/A30%47%62%DPS(Rmb)N/A0.020.040.06第18页共18页

DividendYieldN/A0.0%1.5%2.3%P/E(x)38.629.319.912.3P/BV(x)N/A4.43.73.0ROE(%)37.117.519.723.7SOURCES:CGISRESEARCH,COMPANYDATA,CAPITALIQPoweredbythe第18页共18页

SOURCES:CGISRESEARCHFigure5:ES’sGFAundermanagementbyregion,relatedtoprojectsdevelopedbyCIFIHoldingsFigure6:Revenuefrompropertymanagementservices(RMB"000):similarpatterntoGFAundermanagementWesternregion,2,495Northeasternregion,930Westernregion,48,389Northeasternregion,7,432CentralSouthernregion,4,831CentralSouthernregion,64,462Northernregion,4,118Easternregion,27,865Northernregion,99,071Easternregion,447,499,COMPANYDATA,SOURCES:CGISRESEARCH,COMPANYDATA,KeychartsFigure1:ContractedsalesofCIFIHoldings(884HK),theaffiliateddeveloperofES160,000120%140,00096.2%100%Figure2:GFAsoldbyCIFIHoldings(884HK),theaffiliateddeveloperofES12115.8%10140%120%120,00075.4%100%80%8100,00080%80,000152,00060%69.5742.5%60%60,00041.8%104,00046.2%40%452.1%40,0006.2940%18.6%20,00053,00220%220%30,2102.062.9200%00%20152016201720182015201620172018ContractedSalesofCIFI(RMBm,LHS)YoYGrowth-RHSGFASoldbyCIFI(msq.m,LHS)YoYGrowth-RHSSOURCES:CGISRESEARCH,COMPANYDATA,SOURCES:CGISRESEARCH,COMPANYDATAFigure3:ES’scontractedGFA(propertiesdevelopedbythird-Figure4:ES’srevenue-generatingGFAundermanagementpartiesaremainlyprojectsdevelopedbyCIFIHoldingswithlessthana50%stake)70120%6096.7%100%42.204045403530252015105070%64.9%64.2%60%52.0%5050%80%25.6040%60%3049.3%46.7%17.9013.2830%40%2030,88620%2.109.001.051023.3020%13.1013.7015.408.7311.5713.2014.6410%00%0%20152016201720182015201620172018PropertiesDevelopedbyThird-parties(LHS,msqm)PropertiesDevelopedbyThird-parties(LHS,msqm)PropertiesDevelopedbyCIFI(LHS,msqm)PropertiesDevelopedbyCIFI(LHS,msqm)YoYGrowthofTotalContractedGFA(RHS,%)YoYGrowthofTotalGFAunderManagement(RHS,%)SOURCES:CGISRESEARCH,COMPANYDATA,SOURCES:CGISRESEARCH,COMPANYDATA,第18页共18页

Figure7:Revenuebysegment(unit:RMB’000)Figure8:Grossmarginbysegment:overallGPMisliftedbyimprovingcorebusinessandhigh-marginvalue-addedservices1,200,00070%1,000,000198,44760%50%800,000210,53040%110,064600,000142,98530%51,775400,00020%24,309100,74530,886666,85310%200,000472,268208,948296,1330%20152016201720180201520162017PropertymanagementservicesVAStononpropertyowners2018CommunityVASPropertymanagementservicesCommunityVASVAStononpropertyownersOverallGPMSOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERGSOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERG第18页共18页

EyesontheGroundLifestyles│HongKong│May29,2019HongKongXinchengyueHoldingsNONRATEDPromisingfuturesupportedbyFutureLandCurrentprice:HK$6.27■Xinchengyue(toberenamedS-Enjoy)isapropertymanagersupportedbyFutureConsensusTgtPrice:N/ALand(1030HK),soitsprojectsarelocatedmainlyinlower-tiercitiesineasternChina.Up/downside:N/A■GFAsoldbyFutureLandachievedaCAGRof78%between2016and2018,leadingtopromisinggrowthforS-Enjoy’sGFA.Reuters:■Growthin2019Ewillbesupportedbyalargebatchofpropertiesdelivered,aswellasBloomberg:1755HKasignificantcontributionfromvalue-addedservicestodevelopers.Marketcap:US$655m■Takingintoconsiderationthetrajectoryofthecoredrivers,CapitalIQconsensusHK$5,141m2019EEPSisnowRMB0.35,implyingYoYgrowthof47%onareportingbasis.Averagedailyturnover:US$1.93mRisinginJiangsu,followingFutureLandHK$14.95mS-Enjoy,formerlyknownasXinchengyuewhenitwaslisted,istheassociatedpropertyCurrentshareso/s:820mmanagerofFutureLandDevelopmentHoldings(1030HK).Thecontrollingshareholder,Freefloat:26.8%Mr.WangZhenhua(holding73.2%stake),isalsothecontrollingshareholderofFutureLand,witha71.2%stake.S-EnjoywaslistedontheHKExon6Nov2018.Thebusiness第18页共18页8.3006.3004.30040PriceCloseRelativetoHSI(RHS)253196139ishighlysupportedbyFutureLand,whichisafast-growing,highlyrankedpropertydeveloperintermsofcontractedsales(ranked8thin2018).FutureLandachievedstronggrowthbyaggressivelyaccumulatinglandbanksinlower-tiercities(mainlyinJiangsu),somostofS-Enjoy’sprojectsarelocatedthere.MassiveGFAsoldbyFutureLandwillbethegrowthdriverFutureLandrecordedexplosivegrowthinitscontractedsalesin2016(+104%YoY),andthisgrowthwassustainedin2017and2018.TheGFAsoldhasalsopickedupsince第18页共18页VolmNov-18Dec-18Feb-19Apr-19Source:BloombergPriceperformance1M3M12MAbsolute(%)-10.41.5Relative(%)-2.95.8MajorshareholdersWangZhenhua%held73.2ThisEyesOntheGroundreportrepresentsapreliminaryassessmentofthesubjectcompany,anddoesnotrepresentinitiationintoCGI"scoverageuniverse.ItdoesnotcarryinvestmentratingsandCGIdoesnotcommittoregularupdatesonanongoingbasis.2016,butmorerapidlyin2018(+95%YoY).TheCAGRforGFAsoldbyFutureLandfrom2016to2018was77.5%,whichismuchhigherthanthatofmanyotherhighlyrankeddevelopers.TotalcontractedGFAforS-Enjoythereforealsostartedtoacceleratein2018,rising66%YoYto112.2msqm,achievingaCAGRof53%between2016and2018.Thefuturerevenue-generatingGFA(42.9msqmin2018)willthereforealsogrowwhentheprojectsdevelopedbyFutureLandarereadytodeliver.OverallmarginsarealsoimprovingWithstrongsupportfromFutureLand,S-Enjoyachievedstronggrowthinbothtopandbottomlinesin2018.RevenuereachedRMB1,150min2018,up32.7%YoY.Withoperatingleverage,netprofitin2018increasedstronglyby105%YoYtoRMB150mdespitelistingexpensesofRMB29.4m.Thiscouldbeduetomarginexpansion;whileGPMimprovedslightlyby1.5pptto29.5%,NPMexpandedby4.6pptto13.1%.Managementisoptimisticaboutthe2019growthoutlookManagementmaintainsapositiveoutlookontheCompany’sgrowthpotentialin2019E.WhileitssizablecontractedGFAwillbecomerevenue-generatingGFA,S-Enjoyisalsoaimingforanoverallmarginexpansion:(1)higherprofitcontributionfromvalue-addedservicestodevelopers,astheymadesomepriceadjustmentssotherewillberoomformarginimprovement;and(2)marginimprovementinitscoremanagementbusiness.ValuationIn2018,listingexpensesofRMB29.4mwereincurred,butthenetprofitgrowthin2018wasstillstrong.AccordingtoCapitalIQconsensus,themarketisnowexpectingthegrowthmomentumtobesustainedin2019Easconsensusnetprofit/EPSisestimatedtobeRMB215m/RMB0.35,implying43%/47%YoYgrowthonareportingbasis.第18页共18页AnalystsTonyLiT(852)36986392Etonyli@chinastock.com.hkWongChiManT(852)36986317Ecmwong@chinastock.com.hkFinancialSummaryDec-17ADec-18ADec-19EDec-20ERevenue8661,1501,6852,322NetProfit(Rmbm)73150215308NetMargin8.5%13.1%12.8%13.2%EPS(Rmb)0.120.240.350.50EPSGrowthN/A94%47%44%第18页共18页

P/E(x)44.122.515.310.6P/BV(x)N/A5.24.43.5ROE(%)60.130.916.115.3SOURCES:COMPANYDATA,CAPITALIQPoweredbythe第18页共18页

KeychartsFigure1:ContractedsalesofFutureLand(1030HK),theaffiliateddeveloperofS-Enjoy250,000103.7%94.4%200,000120%100%Figure2:GFAsoldbyFutureLand(1030HK),theaffiliateddeveloperofS-Enjoy201895.2%1666.2%80%150,00074.8%1412108642061.4%18.1260%100,000221,09830.3%40%25.0%126,47250,0009.2865,05020%5.7531,9293.4600%100%90%80%70%60%50%40%30%20%10%0%2015201620172018YoYGrowth-RHS201520162017ContractedSalesofFutureLand(RMBm,LHS)GFASoldbyFutureLand(msq.m,LHS)2018YoYGrowth-RHSSOURCES:CGISRESEARCH,COMPANYDATA,SOURCES:CGISRESEARCH,COMPANYDATAFigure3:S-Enjoy’scontractedGFA120Figure4:S-Enjoy’srevenue-generatingGFAundermanagement65.5%70%10024.5050%40%6016.102030.8037.2010%5045403530252015105042.5%60%12.408047.7%42.1%32.0%10.106.7030%18.2%4010.5087.700.801.5020%30.5051.7026.2018.5020.8000%45%40%35%30%25%20%15%10%5%0%20152016201720182015201620172018PropertiesDevelopedbyThird-parties(LHS,msqm)PropertiesDevelopedbyThird-parties(LHS,msqm)PropertiesDevelopedbyFutureLand(LHS,msqm)PropertiesDevelopedbyFutureLand(LHS,msqm)YoYGrowthofTotalContractedGFA(RHS,%)YoYGrowthofTotalGFAunderManagement(RHS,%)SOURCES:CGISRESEARCH,COMPANYDATA,SOURCES:CGISRESEARCH,COMPANYDATA,Figure5:S-Enjoy’sGFAundermanagementbyregion:JiangsuaccountsforthemajorityoftheYangtzeDeltaregionOtherregions,867BohaiRim,708Midwest,4,105Figure6:Revenuefrompropertymanagementservices(RMB"000):similarpatterntoGFAundermanagementOtherregions,29,938BohaiRim,14,250Midwest,82,618YangtzeDelta,37,207SOURCES:CGISRESEARCH,COMPANYDATA,YangtzeDelta,605,219SOURCES:CGISRESEARCH,COMPANYDATA,第18页共18页

Figure7:Revenuebysegment(unit:RMBmillion)1,400Figure8:Grossmarginbysegment:overallGPMimproving1,200100%90%80%1,00073482978008043600382710917570%60%50%40%30%40015177473256720%10%2002943990%201520162017201802015201620172018PropertymanagementservicesCommunity-relatedservicesPropertydeveloper-relatedservicesProfessionalservicesPropertymanagementservicesCommunity-relatedservicesOverallGPMPropertydeveloper-relatedservicesProfessionalservicesSOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERGSOURCES:CGISRESEARCH,COMPANYDATA,BLOOMBERG第18页共18页'

您可能关注的文档

- 谈IT系统对物业管理行业升级的影响

- 深圳物业管理行业办法

- 潍坊市物业管理行业发展对策研究

- 2018年物业管理行业分析报告书

- 《2019年中国物业管理行业市场前景研究报告》

- 物业管理行业协会在全市社会组织专职工作人员培训班

- hg上海市物业管理行业名牌评价规范

- 月物业管理行业发展趋势与商业模式创新(谢家瑾)

- 建立有物业管理行业特点的管理处财务管理制度的研究(论

- 物业管理行业:万亿市场规模,行业迎来黄金发展期

- 物业管理行业:房地产行业战略转型,物管公司迎来上市潮

- 物业管理行业人力资源管理的思考与展望

- 2014-2020年中国物业管理行业深度调研及发展趋势分析报告

- 谈谈物业管理行业发展现状与趋势A

- 忖量物业管理行业转型升级的新思维

- 物业管理行业协会工作计划b广东省物业管理行业协会

- 物业管理行业深度报告:大行业,小公司,地产后周期的黄金赛道

- 月物业管理行业发展趋势与商业模式创新(谢家瑾