- 1.26 MB

- 2022-04-29 14:05:35 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

'29November2017AsiaPacific/TaiwanEquityResearchSemiconductorDevicesAsiaSemiconductorSectorResearchAnalystsSUPPLYCHAINRESEARCHRandyAbrams,CFA886227156366CreditSuisseTechConference2017:Day1randy.abrams@credit-suisse.comHaasLiuhighlights—bullishsentimentprevails886227156365haas.liu@credit-suisse.comFigure1:CreditSuisseTechConference2017—keypresentationsAlibaba,AMD,Amkor,ams,AppliedMaterials,ASML,Google,Himax,IBM,Intel,Day1LamResearch,Maxim,Mellanox,Micron,Qorvo,TexasInstrumnets,XilinxADI,Corning,Cypress,IDTI,KLAC,Marvell,Microchip,Microsoft,Nvidia,SiliconDay2Motion,SiliconLab,SMIC,TeradyneSource:CreditSuisse■Techtoneandinvestorsatpost-crisishighsforoptimism.The21stCSUS/GlobalTechConferenceopenedMondaynight(27November)inScottsdale,AZ,featuring500investorsand150+companies.TheUS/GlobalTechinvestorsareattheirhighestoverweightinthepastdecadefollowingoutperformance,with70%overweighttechandmanyexpectinga5%+rallyin4Q17,1Q18and2018withoptimismhighoncontinuedinvestabilityonAI/datacentreandgraduallyapproaching5Gcycle.Investorsareoptimisticastech’sdrivershavebroadenedwithdatacentre,IoT,automotiveandmachinelearningasabackdroptodrivetechgrowth.■Businessoutlookupbeatbutintherangeofexpectations.Investorswerebroadlyexpectinganupbeattoneforbroad-basedsemisleveragedtoauto/industrial,andoptimismonlonger-termdriversaroundAI/machinelearning,IoTand5Gandcompaniesdelivered,supplementedbypresentationsfromGoogle,AlibabaandIBM’sWatsondivisionhighlightingrisingadoptionofmachinelearning.Near-termbusinessistrackingatleastinlinewithmanychipcompaniesbelievingthatinventoryisundercontrolandICdemandisoutpacingGDPathighersingle-digitrates.■Memory/Semi-capmostbullish,iPhonechainguidancemaintainedsofar.Memoryandsemi-capcompanieshadthemostbullishpresentations,withAMATandLRCXindicatingthat2018stillpointedtohealthygrowthwithincrementalChinacontribution,andMicronindicateditexpectsDRAMdemand>supplyandNANDpricedeclinesshouldbelessthancostreductionsduetopriceelasticitydrivingmoredemand.OneflipsideisskittishnessonsustainabilityofiPhonestrength,withsupplycatchinguptodemand,althoughatthisstage,suppliersQorvoandAmkorhavemaintainedsoftguidanceforbetter-than-seasonal1Q18.■Asiansemishavealreadypricedinmoreoptimisminthere-rating.WehaveamoreNeutralviewonTSMCwithlessupsidetoestimatesormultipleandalsoviewsecond-tierfoundriesUMC/SMICtohavebeenimpactedbyrisingcompetitiononmature12”.Wepreferspecialtypackagingwithmoredrivers(Powertechfrommemorydemand,Kingpakinautomotive,Inarifromstrategiccustomergrowth)andRealtekforitsIoTleverage.■DaytwohighlightsaresettoincludeADI,MSFTCloud,Microchip,Cypress,KLAC,MRVL,Corning,NVIIDA,SIMO,TERandhosted1x1sbySMIC.DISCLOSUREAPPENDIXATTHEBACKOFTHISREPORTCONTAINSIMPORTANTDISCLOSURES,ANALYSTCERTIFICATIONS,LEGALENTITYDISCLOSUREANDTHESTATUSOFNON-USANALYSTS.USDisclosure:CreditSuissedoesandseekstodobusinesswithcompaniescoveredinitsresearchreports.Asaresult,investorsshouldbeawarethattheFirmmayhaveaconflictofinterestthatcouldaffecttheobjectivityofthisreport.Investorsshouldconsiderthisreportasonlyasinglefactorinmakingtheirinvestmentdecision.

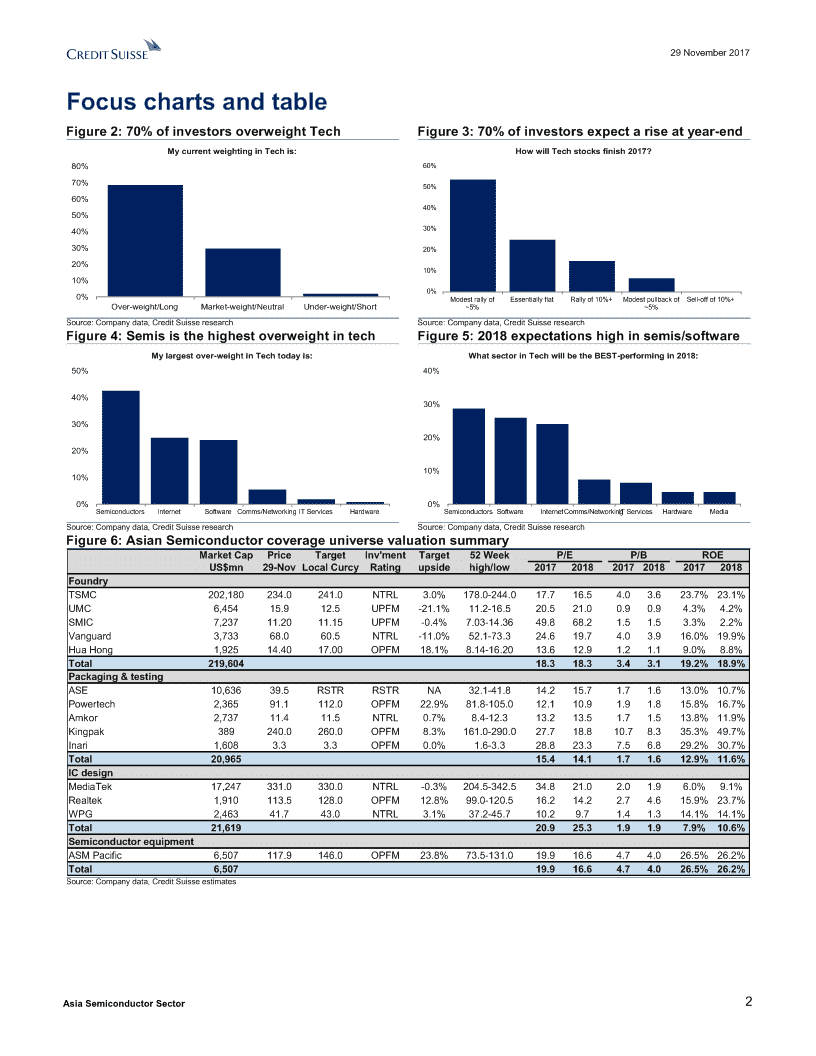

29November2017FocuschartsandtableFigure2:70%ofinvestorsoverweightTechFigure3:70%ofinvestorsexpectariseatyear-endMycurrentweightinginTechis:HowwillTechstocksfinish2017?80%60%70%50%60%40%50%40%30%30%20%20%10%10%0%0%ModestrallyofEssentiallyflatRallyof10%+ModestpullbackofSell-offof10%+Over-weight/LongMarket-weight/NeutralUnder-weight/Short~5%~5%Source:Companydata,CreditSuisseresearchSource:Companydata,CreditSuisseresearchFigure4:SemisisthehighestoverweightintechFigure5:2018expectationshighinsemis/softwareMylargestover-weightinTechtodayis:WhatsectorinTechwillbetheBEST-performingin2018:50%40%40%30%30%20%20%10%10%0%0%SemiconductorsInternetSoftwareComms/NetworkingITServicesHardwareSemiconductorsSoftwareInternetComms/NetworkingITServicesHardwareMediaSource:Companydata,CreditSuisseresearchSource:Companydata,CreditSuisseresearchFigure6:AsianSemiconductorcoverageuniversevaluationsummaryMarketCapPriceTargetInv"mentTarget52WeekP/EP/BROEDivYldUS$mn29-NovLocalCurcyRatingupsidehigh/low201720182017201820172018FoundryTSMC202,180234.0241.0NTRL3.0%178.0-244.017.716.54.03.623.7%23.1%UMC6,45415.912.5UPFM-21.1%11.2-16.520.521.00.90.94.3%4.2%SMIC7,23711.2011.15UPFM-0.4%7.03-14.3649.868.21.51.53.3%2.2%Vanguard3,73368.060.5NTRL-11.0%52.1-73.324.619.74.03.916.0%19.9%HuaHong1,92514.4017.00OPFM18.1%8.14-16.2013.612.91.21.19.0%8.8%Total219,60418.318.33.43.119.2%18.9%Packaging&testingASE10,63639.5RSTRRSTRNA32.1-41.814.215.71.71.613.0%10.7%Powertech2,36591.1112.0OPFM22.9%81.8-105.012.110.91.91.815.8%16.7%Amkor2,73711.411.5NTRL0.7%8.4-12.313.213.51.71.513.8%11.9%Kingpak389240.0260.0OPFM8.3%161.0-290.027.718.810.78.335.3%49.7%Inari1,6083.33.3OPFM0.0%1.6-3.328.823.37.56.829.2%30.7%Total20,96515.414.11.71.612.9%11.6%ICdesignMediaTek17,247331.0330.0NTRL-0.3%204.5-342.534.821.02.01.96.0%9.1%Realtek1,910113.5128.0OPFM12.8%99.0-120.516.214.22.74.615.9%23.7%WPG2,46341.743.0NTRL3.1%37.2-45.710.29.71.41.314.1%14.1%Total21,61920.925.31.91.97.9%10.6%SemiconductorequipmentASMPacific6,507117.9146.0OPFM23.8%73.5-131.019.916.64.74.026.5%26.2%Total6,50719.916.64.74.026.5%26.2%Source:Companydata,CreditSuisseestimatesAsiaSemiconductorSector2

29November2017TableofcontentsFocuschartsandtable2CreditSuisseTechConference2017:Day1highlights—bullishsentimentprevails4Investorsurveypointstoaninvestorbasethatisoverweightandbullishontech..4Alibaba......................................................................................................................6AMD..........................................................................................................................7AmkorTechnology....................................................................................................9amsAG...................................................................................................................10AppliedMaterials....................................................................................................11ASMLHoldings.......................................................................................................12Google....................................................................................................................13Himax.....................................................................................................................14IBM–CognitiveSolutionsDivision.........................................................................14Intel.........................................................................................................................15LamResearch........................................................................................................17MaximIntegratedProducts....................................................................................19MellanoxTechnologies...........................................................................................20MicronTechnology.................................................................................................21Qorvo......................................................................................................................22TexasInstruments(TXN,$99.53,OP,TP$110)...................................................23Xilinx(Xilinx,$71.97,OP,TP$75).........................................................................24AsiaSemiconductorSector3

29November2017CreditSuisseTechConference2017:Day1highlights—bullishsentimentprevailsstCreditSuisse"s21annualtechnologyconferencekickedoffMondayevening,27November,inScottsdale,Arizona,featuring500+investorsandover150companies.Fortheopeningday,weattendedsemiconductorpresentationsacrossthechainincludingIDMs(Intel,TI,MaximandQorvo),equipment(AppliedMaterials,ASMLandLamResearch),back-end(Amkor),memory(Micron),andfabless(Mellanox,amsandXilinx),IBMCognitiveSolutionsandInternetcompaniesGoogleandAlibaba.Wehighlightfeedbackfromourannualtechinvestorsurveywhichhadaverypositivebiasonthetechoutlook,andalsosummarisethetakeawaysfromthefirstday"spresentations.InvestorsurveypointstoaninvestorbasethatisoverweightandbullishontechTheUSS&P500indexisnowup16%withUStechnologystocksup40%YTDandmanyAsiantechstockshaveleveragedtogrowththemeskeepingpace,sothesurveywasagaugeonwhethersentimenthasgonetoofarandtoofastorhasmoreroomtosustain.Thesurveyrevealedaverybullishsentimentconsistentwiththestockperformance,withinvestorsoverweightpositionintech,thehighestsincethesurveybegan,with70%ofsurveyparticipantsoverweightontech.Thenextmoveintheportfolioonlyhad20%settoadd,whichisalsotheleastinthesurvey,indicatinginvestorsarealreadybullishlypositionedbutuncertainonthenextpositioning.Inthesurvey,mostinvestablethemeisAIfor2018.Positioningtodayforinvestorsishighestinsemiconductorsamongthesectorsandoptimismishighestonthatsectorinto2018.Techhasastrongrun,butdifferentthan2000:(1)valuations40-50%below2000levels,withsomesectorsseeingmultiplecontractionasearningshaveoutpacedstocks,(2)fundamentaldriversaremoreR&DdrivenarounddataandanalyticsvstechbubblebeinglessR&Dintensive-Techhasmovedupfrom35%to50%S&PR&Dsince2000.Figure7:Techoverweightatfive-yearhighsFigure8:Lessinvestorshaveconvictiontoaddnow%ofRespondentsOverweightinTech%ofRespondentsBelieveNextMajorPortfolioMoveistoAddTech70%40%65%38%36%60%34%32%55%30%28%50%26%45%24%22%40%20%2013201420152016201720132014201520162017Source:Companydata,CreditSuisseresearchSource:Companydata,CreditSuisseresearchWesummarisekeytakeawaysfromthesurvey:■Investorspositionedforcontinuedupside.Thetechinvestorbaseis69%overweighttech,30%marketweightand2%underweight,with48%ofinvestorsexpectingtechtooutperformin2018and40%performanceatleastinlinewiththeS&P500.Moreinvestorsexpecttomaintaintheoverweight(42%),with21%expectingtoadd,25%reduceandonly11%undecided.Investorsexpectgoodperformanceintoyearend,with54%expectingabouta5%rally,25%aflatmarketandonly6%amodestpullback,withnoneexpectingovera10%sell-off.For1Q18,over42%againAsiaSemiconductorSector4

29November2017expectovera5%rally,with30%expectingcontinuedflatperformanceand28%a5%ormoresell-off.Carryingthatforward,overhalfofinvestorsexpecttheS&P500tobeupover505in2018,with15%expecting10%+and20%flat+/-.Backingtheoptimism,mostinvestorsbelievemanagementteamswillbebullishandright(45%)orcautiouslyoptimisticandright(40%),alsothehighestinthesurvey,withonly15%believingbullishandwrongtone.Figure9:70%ofinvestorsoverweightTechFigure10:70%ofinvestorsexpectariseatyear-endMycurrentweightinginTechis:HowwillTechstocksfinish2017?80%60%70%50%60%40%50%40%30%30%20%20%10%10%0%0%ModestrallyofEssentiallyflatRallyof10%+ModestpullbackofSell-offof10%+Over-weight/LongMarket-weight/NeutralUnder-weight/Short~5%~5%Source:Companydata,CreditSuisseresearchSource:Companydata,CreditSuisseresearch■Sectorpositioningbiasedtosoftwareandsemis.Investorslargestoverweightissemiconductors(43%),followedbyInternet(25%)andsoftware(24%).Largestunderweightishardware(33%)andComms/Networking(31%).Thegrowthoutlookfortechproductsisalsorelativelymodest,withover57%expectingin-linecorporateITspendat4-6%,48%expectingflat-to-down3%PCunits,50%expecting0-5%smartphoneunitgrowthand35%expecting5-10%unitgrowth.■Stockperformanceexpectedtocontinuewiththedecentmacrobackdrop.Investorsgenerallyexpectthemodestgrowthtocontinue,with46%/46%expecting2-3%/3-4%globalGDPin2018andonly5%below2%.DespitesomeconcernsontheApplesupplychain,investorsstillbelieveInformationTechnologywillbebestperformingintheS&Pnextyear(over37%),with21%expectingfinancialsand17%energy,withmaterialandconsumermostpessimisticaboutoutperforming.Thebiggesttechsectorconcernbyfarisrotation(39%),followedbyoverallmarketsentimentandstretchedvaluation(37%)andslowdowninApplesupplychainpostChineseNewyear(16%).■InvestablethemesledbyAIanddatacentre.Investorsrankingofinvestablebuzzwordsfor2018areAI/Deeplearning(34%),DataCenter/Cloud(22%),5G(15%),ElectricVehicles(8%),AutonomousDriving(6%)andSecurity(6%).Only15%stronglyagreewiththeviewofaniPhonesupercycle,with25%disagreeingand55%onlysomewhatagreeing.■Stocks.InvestorstargetonAppleiscenteredon$190(withequalsplitat$170and$210+,andMicronat$55,thoughmoreexpecting$70+than$45.FortheFANGstocks,optimismwashighestonAmazonandlowestonNetFlix.Acrossthesectors,investorsaremostcomfortableowningMicrochipinsemis,Appleinhardware,GoogleandAmazoninInternetandMicrosoftinSoftware.Thefollowingarethekeytakeawaysfromthedayonesemiconductorrelatedpresentations:AsiaSemiconductorSector5

29November2017AlibabaPresenter:JosephC.Tsai,ExecutiveChairman■Chinaconsumptiongrowth–potential8%CAGRthrough2035.ChinaGDPpercapitahasgoneup10xin20yearsfromUS$800toUS$8,000withmiddle-classconsumersrisingto300mnontheindustrialisationandurbanisation.Wagegrowthhasbeengrowingdoubledigitsandsavingsrateishigh,withconsumption40%ofGDPand40%householddebttoGDP(mostconsumersactuallynetcashpositive)vsUSat70%ofGDPfromconsumptionand80%householddebttoGDP.IfChinaGDPgrows5%peryear,but2035,Chinawouldhavea$26tneconomyandifconsumptionreachesUS70%ofGDP,itwouldimplyconsumptionup4xfrom4.5to$18tnor8%CAGRover18years.Alibabaalsoseesitsconsumptionplatformfastexpandingfromphysicalgoodstoservices(movies,groceries,fooddelivery).■Alibaba’scloudbusinessoffersuniquesoftwarecapabilityinChina.Thecompany’scloudbusinesshasbeenrunning10years,whenthecompanydevelopedaproprietaryoperatingsoftware(Apsera)capableofoverlayingtensofthousandsofserversandthinkinglikeonemachine.ItthinksaboutcloudbyreducingcomputecostandmakingavailabletothirdpartiesandbelievesitisonlyoneinChinathatcanofferthatcloudplatformwithitssoftware.ForSinglesDay,itcouldborrowcapacityfromitscloudbusiness,whichforthisyearprocessed250,000transactionspersecondinpayments,2xtheprioryearandalsoaworldrecord.Thecompanyworkswith15lastmiledeliverycompaniestodeliver50mnpackagesdailyandismakinginvestmentsforfasterdeliverytimesandbetterpredictabilityofpackagedeliverytimes.■Machinelearningenhancingtheplatform.Alibabacitedanareawhereitisusingmachinelearninginitsproductassortment,citingawayforittodetectuserscrollingspeedasameasureofinteresttovarythenextitemsthatshowupinthescrollingstream.■Taobaohassignificantadditionalopportunitiesformonetisation.TheTaobaoapplicationnowhas200mnpageviewsperdaywithhighengagementandoffershighmonetisationopportunities.Withintheplatform,italsohas10channelswith10mn+userswithcapabilitiessuchasnewsfeeds,broadcastingandlike-mindedusergroupsthatAlibabacouldstillmonetiseinthefuture.■Globalstrategytargetedatemergingcountriesrequiringleapfrogtechnologies.AlibabaislookingattheexperiencesithasinChinaandhowcanitplantthatinothermarkets.Withusersonmobile,itlooksfordevelopingmarketswithlessestablishednetworkswhereitcanintroducenewleapfrogtechnologies.Inbanking,itdoesnothavetoworryaboutestablishedbankbranchesforonlinebankingintroductioninsomemarkets.MostInternetcompaniesseeIndonesiaasattractivewith200mnyoungandmobileconsumerswithUS$800bnGDP.Alibabaviewsitdifferentlyandlessexcitingwithoutthemanufacturingbase.Pakistanhasasimilar200mnpopulation,soAlibabacouldconsiderthatopportunity.■IndiaisabattlegroundwhichAlibabaistryingtoavoid.IndiaishavingafiercebattlebetweenAmazonandFlipKart.AlibabawantstoavoidtheelectronicsSKUbiasinthatmarketwhereconsumershaveloyaltytotheproductbrandratherthantheretailer.Thecompanyhasspunoffane-commercebusinesstotargetofflineretailers.AlibabaisstillavoidingheadoncollisioninmostmarketswithAmazon,thoughatsomepointwillcompeteonthefringes.■Alibabamergingonlineandofflinecommerce.Withmobilephones,onlineandofflinecommercehasblurredsinceausercanscanastorecodetofindthesizingfromthestoreonline.Alibabaisworkingondigitisingofflineplayersbyidentifyingandcapturingcustomersinthestoreandmappingtoonlineandalsointothecompany’sAsiaSemiconductorSector6

29November2017ERPsystems.Thecompany’sHeManggrocerybrandcanmanageonlineandofflinebehaviourforfreshfooddeliverydownto30minuteswithfulfillmentclosetohome.ItacquiredSunArttoimplementitstechnologyinitsretailstores.Italsohasareastoenhancecustomersbrandbyofferingwaystoengagewithcustomers(broadcasting,livechat,Q&A).■Investingonlongproductcycleopportunities.Alibabaismakinginvestmentsinentertainment,newmediaandAI.Itsruleofthumbfornewbusinessesrequirethreeyearsforproofofconceptandayear5-7conversationonmonetisation,years7-10onharvestingandthen10yearsonreinvention.■M&Aimplementation.StrategicM&AisdrivenbythebusinessunitsatAlibaba,andJosephTsaiwilldotheimplementationtofillinthepieces.Thecompanyiscommittedtodeployingcapitalforretail,includingSunArt.AMDPresenter:LisaSu,PresidentandCEOAnalyst:JohnPitzerFigure11:AMDearningssnapshotAMDSep-17Dec-17Mar-18ECY2017ECY2018EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$1,643$1,397$1,397$1,347mto$1,446m$1,236$1,249$5,246$5,246$5,642$5,900%Q/Qchng34.5%-15.0%-15.0%-12%to-18%-11.5%-10.6%%Y/Ychng25.7%26.3%25.6%22.8%22.8%7.6%12.5%Seasonality(q/q)12.6%-9.7%-12.1%GrossMargin34.9%35.0%35.0%~35%36.2%35.8%34.3%34.3%36.3%36.4%OperatingExpenses$419$410~$410m$385$1,573$1,631OperatingMargin9.4%5.6%5.7%4.0%5.3%5.3%8.0%8.5%NetIncome$110$49$46$140$351NetMargin4.9%1.4%1.4%0.7%4.2%EPS(GAAP)$0.06$0.01$0.01($0.01)$0.17EPSPF(exoptions)$0.10$0.04$0.04Implies$0.04$0.04$0.03$0.13$0.13$0.31$0.35Fullydiultedshares1,143.01,143.01,143.01,065.31,143.0Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■AMD’sgrowthhasimprovedwithitsstrongproductlaunchyear–2018tobetheyearofrevenueramps.LisaSuhasbeenCEOforthreeyears,andhasworkedonpositioningthecompanyasahigh-performancecomputingleader.Herfirsttwoyearswereaboutimprovingthefinancialsandproductdevelopment,withthisyearbeingaboutproductlaunchesof10newfamiliesofcrossclient,serverandgraphics.Thecompanybelievesithasdonewell,growingover20%YoYvsinitialdouble-digitstarget,addingUS$1bnofsalesfromthesenewproducts.For2018,itseesitastheyearofrevenueramps,nowthattheproductshavebeenlaunched.■Newplatformsrampingwell.Thecompanyisoptimisticoncontinuedgrowth:(1)RyzenseeingrisingASPsandgettingaliftnowwithitsrecentmobilelaunch,(2)graphicsplatformlaunchedacrossgamingandmachinelearning,and(3)serversgettingtractionwithcloudandOEMcustomers.■Epycwellreceivedforitsperformanceenhancements–morecloudstannouncementsbetweennowandyear-end.TheEpycisthe1generationoftheZenproductlineintroducingperformance(morecoresandpercoreperformance)andmorebalancedsystems(CPU,fabricandchipletoffersflexibilitymanagingworkloadsbetterhandlingI/O,bandwidthandmemory)whichhasimprovedperformanceinmachinelearning,virtualisationandstorageapplications.CustomerreceptionhasbeenAsiaSemiconductorSector7

29November2017positive,includingHPintroducingonitshigh-volumeplatform,severalcloudannouncementsbetweennowandyear-end,andeveryoneofthesuper7cloudndrdprovidersnowworkingwithAMD.New2/3generationEpycplatformsareindevelopment,andmanagementexpectsmoretractioninitsnextgeneration.■Serversharetargetat5%byend2018,25%longterm.AMDexpectsthatbytheendof2018itcangettomid-singledigitmarketshare,consistentwithOpterontaking4-5quarterstoreachthatmilestone.Itsnextobjectiveis10%whichwouldtakeanother4-5quarters.Longtermwithitsbetterplatform,ittargets25%marketshareasitisoptimisticonitsZen2potentialdoingevenbetter.■Ryzendouble-digitgrowthexpectedtocontinuein2018.ThecompanyisgettinganupliftonmarginsandASPsfromRyzen.ThecompanyhasmadeprogresswithDIY(doityourself)andenthusiasts.ItnotedthatitsshowingonBlackFridayattope-tailershaditachieve3of5or6of10top-sellingSKUsItlaunchedprocessorwithintegratedgraphicsin4Q17andrampingupfurtherin1Q18.Ithasthetop-threeOEMsDell,HPandLenovocommittedtoplatformsforRyzen.ItexpectsRyzentogetto50%ofitsshipmentsby1Q18.Managementexpectstogetbacktoitshistoricalhighteenstolow20%marketshare,asitnowcanaddressthepricepointsfromUS$99toUS$999.Growthisstrongdoubledigitsin2017,andthecompanyexpectsthattocontinuein2018.■Vegagraphicsrampingacrossitsplatforms.ThecompanyrolledoutitsVegahigh-endin90daystoallitschannelsandexpectsastrongrampin4Q17.ThecompanyisaddingtensorflowandCaffemachinelearningandalsobelievesitsupportsgaminginterfaceslikeDX12andVulcan.■Crypto-currencyaddedmid-singledigitstogrowthin2017,nownormalising.AMDhashadanupsidedriverfromcrypto-currencyYTD.Itsguidanceis23%YoYfor2017,with“mid-singledigit”percentagefromcrypto-currency.In2H17,thecompanystillseesdemandfromenterpriseminersbutabitlessfromconsumers,andbelievesthatbusinessisnormalisingin2H17.Itsotherpiecesarestillstrong,soitstillexpectsdouble-digitYoYgrowthoverallin4Q17.ItsforwardlookingestimateshasmoreofthegrowthfromhighperformanceCPUsandGPUsbutnotfactoringinthecontinuedgrowthofcrypto-currency.ManagementindicatedBitcoinisASICdrivenbutotherslikeEthereummoreGPUdriven.■Technologymigrationscoming.Thecompanywillintroducemoreplatformson12nmin2018forperformanceenhancement.Itisinvestingaggressivelyon7nmandmakingabigbetonthattechnologynode.■Semi-customtocontinuebeingarevenuedriver.Thegameconsoleisslightlyexceedingexpectationsthisyearwithsomestrengthtowardstheendoftheyear.AMDexpectssomedeclinenextyearwiththeagingofthiscyclebuthasanewwinwithAtariandsomenewprojectsin2H18tooffsetthat.Thecompanyalsohasasemi-customdesignwinprovidingitsdiscretegraphicsforoneofIntel’shigh-endCPUsinaspecialtypackagethatiscomplementarytoitsotherproductefforts.AMDsawthisasanopportunitytobroadenitsRadeonbrandasgraphicsofchoicenowacrossSony,Microsoft,AppleandIntelwithIPacrosshardware,softwareandecosystem.■Opexinvestmentstobemaintained.AMDwillinvestoperatingexpensesat20%ofsales.ItbelievestheproductsarestandingwelltoraiseASPsandhasnotseenaresponsefromitscompetitortolowerpricing,thoughitwillkeepconservativeonitspricingassumptions.AsiaSemiconductorSector8

29November2017AmkorTechnologyPresenter:SteveKelley,PresidentandCEO,MeganFaust,CFO,GregJohnson,VPofFinanceandIR,GielRutten,EVPofAdvancedProductsAnalyst:RandyAbramsFigure12:AmkorearningssnapshotAMKRSep-17Dec-17Mar-18F2017EF2018EF2019EReportedActualConsGuidanceCSConsCSConsCSConsCSConsTotalRevenue$1,135.0$1,091.9$1,091.0$1.05-1.13bn$1,020.9$1,024.0$4,130.0$4,129.0$4,352.5$4,343.0$4,580.3$4,553.0%Q/Qchng14.7%-3.8%-3.9%-0.4%-7.5%-6.5%-6.2%%Y/Ychng4.5%6.9%6.8%11.7%12.1%6.1%6.0%5.4%5.2%5.2%4.8%TotalGM*20.0%17.9%18.0%17-18.5%16.8%17.5%17.9%17.6%18.5%19.0%18.7%19.6%OperatingExp.*$118.4$115.1$114.0$463.8$462.4$491.8OperatingMgin*9.5%7.4%7.4%5.6%6.2%6.6%6.5%7.9%8.2%7.9%8.8%GAAPNetIncome$54.4$46.8$45.0$34mnto$54mn$29.2$32.0$206.8$206.0$202.5$208.5$222.3$236.0GAAPNetMargin4.8%4.3%4.1%2.9%3.1%5.0%5.0%4.7%4.8%4.9%5.2%GAAPEPS$0.23$0.20$0.19$0.14to$0.23$0.12$0.11$0.86$0.74$0.85$0.82$0.93$0.87ProFormaEPS*$0.27$0.20$0.19$0.12$0.11$0.55$0.74$0.85$0.82$0.93$0.87Fullydilutedshares239.6239.6239.6239.7239.6239.6Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■BroadEnd-MarketBase.Amkormaintainsadiversecustomerbase–~40%ofRevintosmartphoneapplications,25%intoautomotive,25%intoindustrial,therestintocomputingnetworkingandIoT.AmkorrecentlyincreaseditsexposuretoautomotivewithJ-DevicesAcquisition(tookautosfrom11%to25%ofrevenue).■2017Recap/Positive2018Outlook.In2017,Amkorcontinuedtogaininmultiplesmartphoneecosystems-into2018AmkorguidedforC1QtobebetterthanseasonalmostlydrivenbytheextendedlaunchperiodoftheiPhoneX–thegeneralmarketcontinuestobestrong,demandsignalsarestillpositiveandAmkordoesnotseeanybuild-upofinventoryinthedistributionchannel.BeyondC1Q18,it’shardtopredictrevenuegrowth,anditdependsonhownewflagshipphoneshavebeenreceived.■StrongContentiniOSEcosystem.AmkorstrongcontentintheiPhone5,6,7,8andX–importantly,itdoesnotmatterwhichspecificiPhoneSKUsellstotheendcustomer,butratherjustthetotaliPhoneunitsales.■GreaterChinagrowthatdecentmargins.AmkorafewyearsagohadaconcernthatengaginginChinawouldyieldameaningfullynegativeimpacttomargins–however,engagingwithGreaterChinahashelpedutilisationandboostedprofitability–abitcounter-intuitivebutmakessensegiventhat60%ofAmkor’scostsarefixed.Simplyput,Amkor’sgoalistogrowrevenueandprofitabilitywillfollow.ItsChinabusinessisnowUS$250mnandittargetstoreachUS$500mnin3-4years.■Automotivegrowthshouldbeinline-to-betterthansemisautomotivegrowth.AutomotiveisAmkor’s2ndbiggestend-marketat25%ofrevenue.Amkormaintainedthatitexpectstogrowatleastinlinewithindustrygrowthat9%.Relativetomargins,AmkorcontinuestoworkthroughJ-DevicesconsolidationwhichshouldimproveOperatingMargins-Amkorexpects$30mninsavings,$25mnofwhichwillbeinmanufacturingcosts,supportinga20%GMtargetforfull-year2018.■AIOpportunity.AIusesstandardpackageswhichallowsAmkortouseexistingmachinesandtesters.TheCompanynotedthatitisbuyingsomeincrementalcapacity.AmkoralsonotedthatitisinvolvedincryptoandAIandiswellpositionedwithboth–theCompanytreatscryptoasa“bluebird”–i.e.usingittofillexistingcapacityandnotinvestingheavily.AsiaSemiconductorSector9

29November2017■AmkorbelievesmajorcustomerM&Ashouldbeaneutraloutcome.AmkorhasexperiencednumerouscustomerM&Asoverthelastfewyears–ingeneral,customerswanttodealwithfewerlargerOSATstogetbetterpricingandmoreconsistency–Amkoriswillingtoparticipate,andinreturnisbeingrewardedwithhighervolumesandhigherutilisation.SpecificallyQCOM,NXPIandAVGOareallcustomersofAmkor–AmkornotedthattheM&Awouldhaveaneutralimpactonitsbusiness.■TaiwanM&Acouldgiveitalift.AmkorisseeingmorecustomerswillingtoworkwiththeCompany.WhiletheTaiwancompanieswillgeneratesomeeconomiesofscale,Amkornotedthatitwilltakesometimetorealiseallthosesynergies.CustomerswhowereoverexposedtoASEandSPILhaveshiftedtoAmkortoprovidesomeoffset.■Trendtowardspackaginglevelintegration.Amkorisalreadyanindustryleader–mostofitsactivityiscenteredinitsKoreaK4factory,aswellasitsnewerK5factory.ThisyearAmkorestimatesthatitwillgenerate$800mninrevenuefromSiPproducts,andexpectsittobea$1bnbusinesswithinthenext2-3years.■Capexcouldstayflatin2018.Amkorreiteratedits2017capexat$550mn,and2018capexisestimatedtobeflatYoY(lowteenscapitalintensity)–whichshoulddriveover$200mnin2018FCF.Amkorcontinuestoreducedebt($13mnannualinterestsavingsasperrecentdebtrepurchase)–theCompanywillcontinuetolookatfurtherde-leveringpost-investinginthebusiness.amsAGPresenter:MichaelWachsler,CFOAnalyst:AchalSultania■amsleveragingitsopticalsensingcompetencyinto3Dsensing.amshasbeenaleaderinopticalsensingforyearsandhasleveragedthatinto3Dsensingwhichitseesforusesacrosssmartphones,facerecognitionandautomotive(whichitbelievesmaybethelargestopportunityfor3DLidar).ThecompanyacknowledgedsomecompetitorsincludingSTMwithtimeofflight,SonywithimagingandtheHimax-Qualcommpartnership,thoughamshasdemonstratedhighvolumeramp-upcapability.■3Dsensingdriversfromvolume,growthandcontentgains.Thecompanyseesgrowthfrommobilefrom(1)morevolumeexpandingintotabletsandnotebooks,(2)AndroidcampadoptionincludingrecentannouncedcooperationwithSunnyOptical,and(3)backsideofthesmartphoneforaugmentedrealityandgaming.ThecompanyhascompletedGen2ofitsdotprojectorwithanASPincreasebyimprovingpower/performance.■Androidopportunitybeyond2018.AmsbelievesAndroidwillnotmeaningfullyadoptinthenext9-12monthsduetosystemcomplexitychallenges,gettingitreadytobeintegratedintoasmartphone.Qualcomm-Himaxcouldhelpenabletheecosystembutwillhelppavethewayformoreadoptionandpenetrationforams.ThecompanybelievesaVCSELsolutionwiththelightpathwillbeusedoveredgeemittingfortheback-sidecameralongerterm.ItdoesnotbelieveitcanintegratetheViavifilter.■Growthoutlookconservativeonadditionsfromthenew3Dsensingdrivers.Thecompany’sgrowthforecastfor2018doesnotincludeAndroid,VCSELrevenueorback-side3Dcamerabusiness.Thecompanyisstillseeinggoodgrowthfromautoandindustrial.■Optimisticongrowthfromotherareas.Thecompanyseesstronggrowthinthecomingyears,alsofromaudio(MEMsmicrophonedriversandnoisecancellation),biosensorsandenvironmentalsensors.AsiaSemiconductorSector10

29November2017■GMstargetedina50-55%range.ThecompanyhassetaGMrangeof50-55%andguided4Q17at26-28%.TheHeptagonbusinessishighercapitalintensityandlowerGM,andlargehighvolumecustomersinconsumerapplicationwillalsobebelowcorporateaverage,thoughhasloweropexratiosduetothevolumescalebenefits.Theauto/industrial/medicalbusinessoffershighermarginsthoughrequiresmoreopex.AppliedMaterialsPresenter:DanielDurn,SVPandCFOandMichaelSullivan,VPofInvestorRelationsAnalyst:FarhanAhmadFigure13:AppliedMaterialsEarningsSnapshotAMATOct-17Jan-18Apr-18CY17ECY18EReportedCSConsGuidanceCSConsCSConsCSConsTotalRevenue$3,969.0$4,100.0$4,111.8$4.00-$4.20bn$4,521.6$4,111.8$15,359.0$15,370.8$17,605.0$17,160.5%Q/Qchng6.0%3.3%3.6%10.3%0.0%%Y/Ychng20.4%25.1%25.4%27.5%25.4%29.7%29.8%14.6%11.6%TotalGM*46.2%46.6%46.6%46.2%46.4%46.7%R&DExpense*$466.0$480.1$497.1$1,837.1$2,010.9OperatingMgin*28.7%29.2%29.0%29.8%29.0%28.6%29.7%NetIncome*$1,005.0$1,048.1$1,185.9$3,841.1$4,587.3NetMargin*25.3%25.6%26.2%25.0%26.1%EPS$0.93$0.98$0.98$0.94-$1.02$1.11$0.98$3.56$3.56$4.31$4.14Fullydilutedshares1,076.01,071.31,068.41,079.31,064.0Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastreamth■AI’simpactonAppliedMaterials.ThecompanybelievesAIissettingupa4waveofdemand,drivenbyAIandbigdataanalyticsandIoTwhichcanbeworthtrillionsofdollars.ThecompanyexpectssemiconductorstogrowaboveGDPandsemi-capin-linewithsemiconductorsfromthesetrends.■SlowingMoore’sLaw.Appliedmaterialsbelieves2Dscalingisgettingmoredifficult,requiringself-aligneddoubleandquadruplepatterningwillallowgreaterresolution.Capitalspendingwillincreasewhilepricingperbitwilldeclineataslowerbase.Forlogic,itisearlyinexplorationofmoreverticalstructureslikethe3DNANDstructuretobringthattothelogiccustomers.■WFEexpectationfor2018.WFEspendingisaboutUS$32bnperyearforPCsplushandsetsbuthasliftedtoUS$45bnonthenewdrivers.Thecompanyisseeingmorestrengththatcouldallow2019plus2020tobeafewbillionabovetheUS$90bnguidedattheanalystdaywithmorevisibilitythaneverbeforeduetoendmarketstrength.■Mixin2018drivenbyNANDandlogic.Thecompanybelieves2017mixis50/50logic/foundryandmemoryandwithinfoundry/logic,1/3islogicand2/3isfoundryandwithinmemory,1/3isDRAMand2/3isNAND.For2018,thecompanyexpectsthemixinlogictoshifttologicoverfoundry,andinmemoryitwillshifttoNANDoverDRAM.■Chinacapex.AppliedMaterialsexpectsanincrementalUS$2bnofspendingin2018over2017.ThespendisstillcomingfromInternationalcompanies,withlessthan50%fromdomesticcompanies.Capexin2018willstillbedrivenbymemory.■Displaymarketoptimismincreasing.Displayisgrowingata21%growthrate,3xthesemiconductorbusiness.ThecompanyseesstrengthinTVandhandsetsandwillneedtomakeupgradestolargergenerationfabstogetmoreefficientoncuttingpanels.■Servicebusinessagoodcashgenerator.Theservicebusinessiscashflowgenerative,helpingtoincreasetheinstalledbaseandmanagesemiconductorcomplexity.Toolsunderaservicecontractcanalsohelpthemimprovetheyieldcurve.AsiaSemiconductorSector11

29November2017■GMsstable.ThecompanytargetsincreasingGMs70bpperyearatconstantmix.Theservicesanddisplayarefastergrowingbutdilutivetocorporatemargins.ASMLHoldingsPresenter:WolfgangNickl,EVPandCFOAnalyst:FarhanAhmadFigure14:ASMLEarningsSnapshotASML-AESep-17Dec-17Mar-182017E2018EReportedCSConsGuidanceCSConsCSConsCSConsBookings€2,154.0€1,720.4€1,900.4€8,013.0€7,734.6%Q/Qchng-9.3%-20.1%10.5%48.5%-3.5%TotalRevenue€2,447.4€2,100.0€2,447.4E2.2bn€2,583.8€2,148.9€8,592.4€8,582.6€10,873.9€9,903.7%Q/Qchng16.5%-14.2%0.0%23.0%-12.2%%Y/Ychng34.9%10.1%34.9%32.9%12.7%26.5%26.3%26.6%15.4%TotalGM*42.9%44.0%39.9%43.0%46.1%44.0%44.7%44.8%44.5%OperatingExp.*-€417.8-€425.0-€420.0-€479.7-€1,671.2-€1,915.0OperatingMargin*26.8%24.9%26.8%27.6%25.5%26.4%26.8%NetIncome*€557.1€438.9€613.6€1,914.4€2,515.3NetMargin*22.8%20.9%23.7%22.3%23.1%EPS*€1.29€1.02€1.29ImpliedE1.07€1.42€1.07€4.43€4.51€5.87€5.53Fullydilutedshares432.0432.0432.0432.2428.5Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■GrowthacceleratingasEUVtoolshipmentsrise.ASMLbelievesitwillgrow25%+thisyearvs13%growththelastfiveyears.EUVwasUS$350mnlastyear,aboutUS$1bnthisyearandUS$2.5bnnextyear.Therestofthebusinesswillmaintainthesamelevel.Thecompanyseeshealthybusinessfrommemoryandalsofromlogicwiththeroll-outof10nm.■EUVinsertionview.Thecompanysees6-10exposuresinlogicfortrue7nmwithTSMCimplementingseverallayersonits7+nodeandatorabovethat6-10layerrangefor5nmriskproductioninearly2019.Itexpects1-2layersfor1yforDRAMwithabigcandidatepoolofwafers.Thattoolunderpins20toolsin2018andatleast30toolsin2019whichmaybesupplyconstrainedand40toolsby2020.Itindicateditcouldhave30%upsidetothat30tooldemandrequirementsowillworkwithcustomersonallocationbasedonwhentheycommunicatetheirrequirementsandalsoongettingthetoolstohigherproductivitytosolvetheunder-supplyissue.■EUVimplementationchallengesgettingworkedout.Thecompanybelievesprogressisgoingwellwithresists,maskinspectionmakingprogressincludingwithitsHMItoolacquisition,andwillpelliclewhichASMLhasdevelopedthatisnowdefectfreeandcanwithstand250watts.■Maturetoolsseeingcontinuedinvestment.ThecompanyisstillspendingUS$400mnayearonolderDUVR&DasotherlayerswillseemoregrowthiftheEUVcriticallayersrise.■Servicebusiness.ServicebusinessoptionsandupgradeshasgrownsignificantlythisyeartoUS$2.6bn,upfromUS$2.1-2.2bnlastyear.Managementexpectsabout10%steadygrowthfromitsgrowinginstalledbaseeachyearbuthadmoreupgradesthisyear.TheservicebusinesswillgrowdisproportionallyasEUVriseswithmoreservicerequirementsandmorespareparts,withUS$5-7mnpertoolservicevs1mnforimmersion.The110mntoolswoulddriveUS$550-770mnincrementalservicerevenue.■Capitalallocationplans.Thecompany’sR&Dhascomedownfrom18%to14%,andwilldropfurtherto13%ofsales.ItinvestedinCarlZeissandacquiredHMIbutdoesnotseemeaningfulM&Acoming.Thecompany’soptimalcashbalanceisUS$2-2.2bnwithexcessgoingtodividendsthatcansteadilygroworsharebuybacks.AsiaSemiconductorSector12

29November2017■ChinaopportunityaUS$3-4bnopportunitythenext3-4years.ASMLhas700headcountand400machineswith11-12offices,andisnowseeinglargerrulefromtheChinesedomesticcompanies.ItisdoingbusinesswithfiveoriginalChinesecustomers(2foundrieswithlong-timeoperationswithagoodpositionand3greenfieldmemoryopportunities).ASMLhasvolumepurchaseagreementswithall5andwillshiptoallnextyear,withtargetamountsevenwithcushionwouldmakeitaUS$3-4bnopportunityoverthenext3-4years.Thecompanyseestheroll-outmethodicalanddisciplined.■Waferinspectiongrowthwithanewpatternfidelitytool.HMIofferscomputationallithographyandsupplementsthecompany’ssuccessfulYieldstaroverlaymetrology.ASMLwillgointopatternfidelitymetrologytoimprovethequalityofthetool,withfirsttoolshippingandcombininge-beamandthesoftwareguidingthebeam.HMIwilladdaUS$1bnopportunityby2020dependingontheguidedbeamandmulti-beamtechnology.GooglePresenter:PhilippSchindler,SVP,ChiefBusinessOfficer,GoogleAnalyst:StephenJu■Operationalfocusin4areas.Mr.Schindler’sfocusison(1)helpingensureitsadvertiserssuccess,(2)focusingonGoogle’spartnershipsandservices,(3)expandinginhighgrowthmarketslikeAsiaandLatinAmerica,and(4)leadershiptohavetherightpeopleandsystemstoscalegloballybutstilloperatelocally.■Googledevelopingnewhumaninterfacesforinputandoutput.Googlecontinuestoexpandfunctionalitybeyondtheinterfaceoftextandnowvoicequeriescominginandout.Italsobelievesvoicein,visualoutisanattractiveusecaseandeventuallyseesusecasessuchasimageorvideointogetdifferenttext,videoorvoiceresponses.Itindicated20%ofitsmobilequeriesarevoicebased.■GoogleExpressimprovingfunctionality.Thecompany’sGoogleExpressServiceisexpandinginassortment(addingmoreWal-Martproductavailability)andfunctionalitywiththeadditionofvoiceandabilitytolinkaccountsforamorefrictionlessserviceforcustomers.■Furthersearchoptimisationusingmachinelearning.Googlestillseesopportunitieswithshifttomobile(abilitytoswipeandscroll)andrunshundredsofexperimentseachquarterwhichstillderiveshundredsofimprovementseachquarter.Itisactivelyusingmachinelearningtocontinuetoimproveitsplatformforadvertisers.■MeetingrequirementsfortheEuropeanruling.TheEUruledinJunethatGooglemustputrivalshoppingservicesonequaltermswithGoogle.Googlenowbelievesithasasolutiontomeettheserequirements.■Investinginimprovinginformationquality.Google’sgoalistoimproveinformationqualitysotryingtoimproveitssearchinresponsetomoreconcernsaboutfakeorpoliticallyslantednews.Thecompanyhasalreadyscreened1.7bnadvertisementsandisonlyofferingverylimitedadvertisingoptionsforpoliticalpurposes.Thecompanyisalsotakingswiftchangestosearchalgorithmstoscreenoutfakenews.Itaddedafactchecktagongooglesearchandresults.Itusesmachinelearningalgorithmstoimproveitsscreening.■Machinelearningtoimprovetheadvertisingexperience.Googleisusingmachinelearninginseveralareas:(1)advertisingtoimprovetargetingandidentifyingnewaudiences,(2)GooglecreativelabtobetterbringGoogleservicestousers,3)smartbiddingalgorithmstogettherightbiddingattherighttime,(4)improvingattributionforuserclicks.Itsintentisstilltoimproveitspartners/advertisersROI.AsiaSemiconductorSector13

29November2017HimaxPresenter:CFOJacky;IRmanagerOpheliaLinAnalyst:JerrySu■4Q17trackingslightlyahead.HimaxsaidatourAnnualTechConferencethatits4Qsalesistrackingslightlybetterthanitsguidanceof4-10%QoQdecline(down3.5%toup3.0%QoQexcludingone-offreimbursement).ItseessalesforlargedriverICtrackingbetterthanthemoderateQoQguidance,whileS/MsizeDDIsalescouldalsobeattheflattishQoQguidance.Non-driverICsalesexcludingtheone-offUS$13.3mnreimbursementisontracktomeetthe10%QoQguidance,whileWLOshipmentshouldgrow20%QoQasitscustomercontinuesthepullin.WeexpectHimax’s4Q17salestoarriveatUS$189mn(down4%QoQ)andOPofUS$6.8mn(OPM3.6%)on24.8%GM(down0.7ppQoQ).Itwillbookone-offdisposalgainof~US$21mn($0.12/share)in4Q17,andweestimate4Q17EPSofUS¢14.6vsguidanceofUS¢13-15.■MoreengagementsonAndroid3Dsensing.Managementsaiditisseeingmoreengagementsonits3DsensingsolutionfromleadingAndroidsmartphonemakersgiventhatitsSLiMsolutioniscurrentlytheonlydesignapprovedbyQualcomm.WethinkHimaxwillhavemorevalue-addintheAndroid3Dsystemasaresultofitsproprietaryknow-howonhighsensitivityNIRsensor,assemblyandtestingofedge-emittinglaserprojectormodule,WLO/DOEmanufacturingcapability,andsoftwareforfine-tuningthesystem.HimaxhasnotfinalisedthephaseIIcapexyetbutitexpectsthetotalamountcouldbeover$100mn,vs$80mnforphaseIthatwasannouncedinAugust2016.Itisstilltargetingtobuild2mnunits/monthcapacitybeforeend-1Q18,andwethinkitscapacitycouldreach6mn/monthorhigherbyend-2018,ifitcontinuestowinmorefrontfacing3Dsensingprojects.Wethinktherear3Dcamerashouldbe2H19or2020storyfortheindustry(iPhone2H19,Android2020).WeexpectHimaxtostartsmallvolumeshipmentof3Dsensingmodulein2Q18(pilotproductionin1Q18),withOppoandXiaomilikelytobeitsinitialcustomers.WethinkHuaweiandSamsungarealsoconsideringHimax’ssolutionbutwebelieveitwilltakeafewmoremonthstofinaliseasthiswillinvolveinchangeoftheirprocessorplatformsfortheirflagshipmodels.Asaresult,wenowexpectits3Dsensingtotalsolutionshipmentsof10.4mnin2018(vsourpriorassumptionof~9mn)for17%ofsalesandcouldincreaseto36mnunits(36%ofsales)in2019.ForiPhoneWLObusiness,weseebettervolumein2018-19onmulti-iPhoneadoptionsandproliferationintoiPadsandMacBooks.Weestimateittoaccountfor8%ofsalesin2018and6%ofsalesin2019vsprior~6%ofsalesin2018-19.■S/MDDItooutgrowlargeDDI.HimaxsaiditbelievesitslargesizeDDIwillgrowwithBOEandHKC’snewcapacityrampin2018-19,althoughitfaces8”waferconstraint.ItsS/Msizeshouldseebettergrowththanthelargesize,drivenbyTDDIand18:9DDIwithCOFpackage.WeexpectitsTDDIshipmenttoreach63mnunitsin2018(vsprior57mn)for9%oftotalsales.■MaintainOUTPERFORM.Wekeepour2018-19EEPSandmaintainTPat$15.10basedonourrevisedDCFmodel,implying25x2018-19EEPS.WebelieveHimaxisamajorbeneficiaryfromthe3DsensingproliferationintoAndroid.IBM–CognitiveSolutionsDivisionPresenter:Dr.JohnKellyIII,SVP,CognitiveSolutionsandIBMResearchAnalyst:JamesDisneyAsiaSemiconductorSector14

29November2017■Watson’sLawofdataproliferationrequiringAItoenhanceknowledge.IBMbelievestheindustryisfollowinganewpacecalledWatson’sLawwhichindicatesthatdatawilldoubleeveryyear,puttinganintenseneedforAIimprovementstoprocessthatdata.■AImovingfromnarrowtobroadAI.Machinelearningfrom2010-15was“narrowAI”todoverynarrowreinforcedlearningtechnology(identifyingobjectsandlabeling)andattheotherextremein2050+forartificialgeneralintelligence.Forthenext35years,itsees“broadAI”from2015-50,whereWatsonservicewillbetoextractdata.■OpportunityforAIinenterpriseandindustryforIBMWatson.ThecompanyforecastsaUS$2tnopportunityfordecisionmakingsupportby2025andUS$1.5tnforenhancedproductivityoftraditionalITby2020(CRM,ERP,infrastructure,processautomation).ItoffersWatsonserviceintheIBMcloudandservicesforverticalswithanalyticsitcanprovideonIBMprovideddata,publiclysourceddata,partnerprovideddataandprivateclientdata.IBMispledgingtoprotectthedata,notsharethedataandwillsharethealgorithms.■IBMcognitivesolutionsbusiness.IBM’scognitivesolutionsbusinessisUS$18bnand70%software(Watsonsoftware,WatsonHealth,analyticsanddatabusiness,serviceandsecurity)and30%transactionsprocessing.IBMhas1,000researchersworkinginAIandhasaUS$250mnpartnershipwithMITtoadvancethefieldwiththeUniversityacrossdisciplines.■QuantumComputingwillemergeinthepresenters’careerspan.IBMindicatedQuantumComputingwouldbeordersofmagnitudefasterthananythingbuiltonaMoore’sLawcurveandshouldcometomarketinthepresenters’career,apull-infromhisviewthatitwouldnotbedevelopedinhislifetime.Oncebuiltitwouldbeequaltothelast50yearsofMoore’sLaw.Thepresenterindicatedthatthecompanyhasdemonstrateda50cubitsystem,upfromthe17cubitbeingdemonstratedandtheperformanceincreasesbythesquareofthenumberofcubits.Quantumcomputingcouldallowoptimisationofthesupplychainandfinancialservices/tradingormoleculeanalysisfordrugdiscoveryatspeedscurrentsystemscouldnottouch.IntelPresenter:RobertSwan,EVPandCFOAnalyst:JohnPitzerFigure15:IntelearningssnapshotINTCSep-17Dec-17Mar-18ECY2017ECY2018EReportedCSConsGuidanceCSConsCSConsUpdatedGuidanceNewCSConsRevenue$16,149$16,300$16,317$16.3bn+/-$500m$14,940$15,030$62,008$62,025$62.0bn$64,089$63,801%q/q9.4%0.9%1.0%-2.2%to+4.0%q/q-8.3%-7.9%Seasonalq/q%5.2%2.6%-7.7%%y/y2.4%-0.5%1.0%4.2%5.4%+4.2%y/y3.4%2.9%GrossMargin63.9%63.0%62.9%63%+/-afewpctpts63.1%62.4%63.3%63.0%63.7%62.8%OpEx(R&DplusMG&A)$4,776$5,050~$5.1bn$5,000$20,385$20,700OperatingMargin34.4%32.0%29.6%30.4%30.3%31.4%NetIncome$4,848$4,149$3,531$15,721$15,992NetMargin30.0%25.5%23.6%25.4%25.0%EPS(w/options)$1.01$0.86$0.86$0.86+/-$0.05$0.73$0.73$3.25$3.25$3.25$3.33$3.31EPSpf(w/ooptions)$1.07$0.93$0.80$3.53$3.60EPS(GAAP)$0.94$0.80$0.66$2.93$3.02Fullydilutedshares4,8214,8214,8164,8424,809Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastreamAsiaSemiconductorSector15

29November2017■CFOfocusingonenablingInteltotransformfromaPCcentrictodatacentriccompany.RobertSwanhasbeenCFOfor13monthsandseesopportunitiesinthecompany’stransformationfromaPCcentriccompanytoaddressingbigbetsinmemory,modems,andautomotive(Mobileyeacquisition).Itiswillingtomaketrade-offsincluding(1)financingitsdatacentricbetswithsacrificeofnon-strategicassetslikesellingMcAfee,(2)investinginitsownmemorycapacityforalong-termbenefit,and(3)controlsonopexwhiletryingtoreacceleratesaleswithitsnewgrowthdriversandinitiatives.■TransitionawayfromPCsalreadywellunderway.Intelhasalreadyraisednon-PCdatacentricbusinessesfrom30%to45%ofsales.ThePCTAMdeclinehasdeclined35%butIntelhasstillgrown20%andnowhasmoredata-centricbusinessesgrowingmid-teens.ThecompanybelievesitismovingfromaUS$60bnTAMwith95%+sharetoaUS$260bnwith30%marketsharewiththisdatacentricshift.PCsarestill55%andgeneratescashflowforshareholderreturnsandthenewinvestments.■Growthdriversbecomingmoremeaningful.RobertSwandiscussedprogressonIntel’sgrowthareas:(1)Memory:Intel’scoreNANDbusinessbecameprofitableearlierthanexpectedandwillbeprofitableforthewholeyearandwholememorybusinessprofitablefortheyear,(2)Mobile:growthhasbeendramaticandisexpectedtocontinue,and(3)IoT:NowoverUS$3bnandisexpectedtocontinuetogrowdoubledigits.■MemorykeytoIntel’sdatacomputestrategy–a20%growthCAGRopportunity.Thecompanyseesincreasingcomputingneedsbothatthecloudandattheedgefortheprocessortogetaccesstodatafaster.Compute,analytics,storageandretrievalisgettingmoreimportant,requiringbettercouplingofmemoryandprocessorandalsoacompetencyofIntelthatcanbenefitIoT,dataandPCcustomers.ThecompanyisnottargetingtheUS$100bnslowergrowthpartofstorageandfocusedmoreonSSDand3DNAND,whichthecompanybelieveswillgrowata20%CAGRinthenextfiveyears.IntelbelievesNANDperformancegainscansolveareasHDDandDRAMperformedwithbetterdensityandlowercost.Managementacknowledgeshighercapitalintensivesowillremaindisciplinedondeployingcapitaltophasegrowthinabalancedway.■Modemstilltargetedatbecomingbestin-classandshippingin-housein2018.Intel’sgoalisaboutbuildingthebestproducts.Thecompany’srevenuewasupmorethan40%intherecentquarter.Thecompany’sXMM7480isshippingnowandXMM7560stilltargetedtomovein-housein2018.WeestimatethemodemataboutUS$5foundrycontent,aboutUS$550mnor1.5-2%annualisedimpacttoTSMCa■Managementstillfeelsgoodaboutitsmargintargets,9monthsafterintroducingthem.9monthsago,Intelsetaviewthatitcanstayatthehigh-endofits55-65%long-termGM(60-65%thenextfewyears)including63%in2016/17E.ItacknowledgesamodestdecelerationinGMsthenextfewyearsbutwillimproveopexfrom36%in2015to35%in2016to33%in2017(2Hlowerthan1H).Itbelievesoperatingincomewillstillgrowfasterthanrevenueinthenextfewyearstogetoperatingmarginsataround30-32%.■IntelmanagingPCperformanceinadecliningmarket.Thecompanymaintainscommitmentto(1)annualproductcadenceofimprovements,(2)moveupinthestacktoincreaseASPs,(3)drivedownunitcostmovingtothenextnode,and(4)spendinginlinewithadecliningmarket.IntelstillisseeingthemarketpayingforperformanceinsomesegmentssuchasgamingbutisnotbankingonastrongASPuplift.AlthoughPCunitsarenowstabilising,IntelisconservativethatthePCTAMwillcontinuetodecline,sowillmaintainacautiousstanceoninvestmentsandcosts.Itwouldhaveupsideonprofits/cashflowsifdemandupsidesthatconservativebasecase.AsiaSemiconductorSector16

29November2017■Datacentermaintaininghighsingle-digitgrowthonshifttocloud/communications.Intelismigratingfromenterprisefocustoclouds/communicationsemphasiswith50%nowdrivenbythelatterareaswhicharemorethanoffsettingtheenterprisedeclinetostilldrivehighsingle-digitYoYgrowthwhichitexpectstocontinue.ThecompanyplansanannualcadenceindatacentrelikeinPCstosatisfydatacentrecustomers’needsforbettercomputeatlowercost.ItnotedPurleycontinuestorampuponschedule.■AIanascentgrowthopportunity–InteltoprotectitsstrengthininferencewhileusingacquisitionstoenhancetrainingandedgeAIcompute.IntelindicatedAIisstillrelativelynascentbutgrowthcharacteristicsveryattractiveandInteltargetstowinthatmarket.IntelindicateditsperformanceisverystrongininferenceandcanbeleveragedwithaXeonoptimisedforinference.ItlaunchedXeonscaleabletooptimiseforAIworkloadsforinference.XeonandFPGAscanprotectinferencewhileitsacquisitionslikeNervanacanextentIntelintotraining.ItbelievestheNervanaacquisitioncanstrengthenIntel’spositionagainstNVIDIA’sGPUinthetrainingsegment.ItlaunchedaproductwithFacebookandwillhaveanannualisedcadencewithNervanaforahigh-performanceproductfortraining.Fortheedge,itwilldrivelowerpowerperformance,helpedbyitsMovidiusacquisition.■Pragmaticfinancialguidancephilosophy.Intel’sCFOhopestobuildcredibilityandaccountabilityby“doingwhatyousay”.Itwantstosetguidancetodriveitsteamtobegreatbutgiveinvestorspragmaticconfidencethattheycantrusttheoutlook.■Driverofcashflowgap.Intelisdoingafewinvestmentsforlong-termbenefitwithatemporaryfreecashflowgap:(1)investinginmemoryforlong-termpotentialalthoughhelpingmanagingthecapitalexpendituresbyusingsomecustomers’prepaymentsofmemorycapexinstrategicsupplyagreements,(2)investingin10nmthatwillbedepreciatingandwouldcontributetoabitofGMerosion,(3)investingininventorytosupportcustomerprograms.Thecompanybelievesitcannarrowthatgapinthemediumterm.LamResearchPresenter:MartinAnstice,PresidentandCEOAnalyst:FarhanAhmadFigure16:LamearningssnapshotLRCXSep-17Dec-17Mar-18CY17ECY18EReportedCSConsGuidanceCSConsCSConsCSConsShipment$2,381.6$2,600.0$2350m±100m$2,928.6$9,936.9$11,049.5TotalRevenue$2,478.1$2,550.0$2,478$2450m±100m$2,764.3$2,566$9,527.0$9,543$10,966.7$10,562%Q/Qchng5.7%2.9%0.0%8.4%3.5%%Y/Ychng51.8%35.5%51.8%28.3%36.3%49.4%49.7%15.1%10.7%%q/qseasonal0.0%0.0%0.0%0.0%0.0%TotalGM*47.2%47.5%46.5%±1%47.0%46.9%46.6%R&DExpense*$275.1$281.0$289.5$1,107.7$1,169.5SG&AExpense*$163.0$166.5$171.5$632.1$692.9OperatingExp.*$438.1$447.4$461.1$1,739.8$1,862.4OperatingMargin*29.6%30.0%29.6%28%±1%30.3%29.0%28.6%29.6%NetIncome*$627.8$664.5$733.4$2,365.6$2,844.6NetMargin*25.3%26.1%26.5%24.8%25.9%EPS*$3.46$3.65$3.46$3.00±0.12$4.03$3.68$13.01$13.05$15.63$14.87Fullydilutedshares181.4182.0180182.0181.8182.0Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastreamAsiaSemiconductorSector17

29November2017■AIadriveracrosstechandfacilitatedbysemiconductors.ManagementviewsAIcuttingacrossallapplications(industrial,agriculture,consumer)asitmakestheworldabetterplace.Semiconductorsprovideaplatformbyallowingubiquitousconnectivity,cloudandadvancedcomputation.■SlowingMoore’sLawhelpingdistributionofvalueintheindustrytowardsemiconductorsandLam’scorecapabilities.Lamseesapositiveoftherisingtechnologychallengesbyimprovingeconomicsforsemiconductorsbyplacingmorevalueontheseaskeyenablers.Newmaterials,chipintegrationandadvancedpackagingarepermanentfixturesfortheindustrythatwillalsoenhancethevalueofdepositionandetch.■Targetingsustainableprofitablegrowthandoutperformance.Lamhasgrown25%inthepast4yearsandwantstocontinuetooutperformbothinrevenuethroughhigherrelevancetocustomerswithkeymetricasdollarsofprofitanddollarsofcashderived.■ServicesoutgrowthforLam.Servicesare25%ofsalesandgrowingata25%CAGRand2xtheinstalledbasegrowth.Thecompany’sobjectiveisforits34,000processchamberinstalledbase(willgrowto50,000bytheendoftheyear)andwillcontinuetoservicethatwithupdates,training,upgrades,spareparts,andrefurbishedequipmentfor8”/12”.Lambelievesitisoutgrowingthroughhigherfocus,singlefacingunitforitsinstalledbase,activeproductdevelopmentinservices,andleveragetoetchwhichisdestructiveprocess(etchprocesschambersdestructovertimesorequiremoreservicing).Lam’sspaceisgrowingfastestandismoredestructive.■Lammaintainsitsgrowthforecastin2018.Lamgrew2xtheindustryin2017andistargetingstronggrowthatthestartoftheyear.LamexpectswaferfabequipmentlevelstobeupYoYin2018with1H18strongerthan1H17andMarchwillbemeaningfullystrongerforshipmentsandoutput.Itstillframestheyearsimilartoitsviewwith80%drivenbymemoryrelatedinvestmentmostlytiedto3DNANDbutalsoinvestmentacrossothernewmemorydevices.Thecompany’spresenceisnowmorebalancedthanbeforeacrossallaspectsofthebusiness.■Chinaprogressingbuttakingtimeandwillprogressinadisciplinedway.LambelievesdomesticChinaplayerswillhaveUS$1-2bnofgrowthin2018over2017sostillrelativelymodest.Lamsees4waystoacquireknow-how:(1)acquisitions–difficultforChina,(2)licensing–notmuchoccurring,(3)hiring–muchstrongerandmoreeffectivenowvs1-2yearago,and(4)creationofnewtalent–extraordinaryactivityinthatareanow.ThecompanyseesmorecommitmentstoIC2020/25agendasthanayearago.Thecompanyistracking12of18newfabsintheworldinChina,with6domesticfabsinChinaand6foreignplayersfabsinChina.Itbelievescapacityinstallationwillbeinadisciplinedwayduetothesizeoftheinvestmentsandtheexpectationsofbothinvestorsandthegovernmentsinvolved.ShellsexistbutLambelievestheequipmentinvestmentswillbemoremirroredtodemand.■Lam’slogicmarketexpansioncontinues.SAMexpansioncontinuestogrowthrough3/5nmasmulti-patterningwillcontinue.NANDisdoingverticalscalingbutDRAMandlogichavesignaltonoiseandelectomigrationchallengesrequiringnewmaterialsthatmakeEUVinsufficienttosolvingalltheissuestoaccomplishthenextcouplenodes.Lambelievesthevalueisgoingupordown.Lamviewsetchanddepositionstepswillremainpositivestoriesandthevalueofthosestepswillbemorecriticallyimportant.Itisnowcompetingfor40%ofWFEbyintroducingportfoliosmorerelevanttocustomers.ItstoolASPshavealsoincreasedfromUS$6-7mntoUS$10mnversusafewyearsago.■M&Astillapossibility.ThecompanybelievesithasacorecompetencyinM&Abutdoesnotdominatetheagendaandseesopportunitytogrowitsportfolio.Itwillstilllookfornewareas,indicatingitacquiredCoventortocontroltheprocesswindows.AsiaSemiconductorSector18

29November2017MaximIntegratedProductsPresenter:TuneDoloca,CEO,BruceKiddoo,CFO,KathyTa,VPofIRAnalyst:JohnPitzerFigure17:MaximearningssnapshotMXIM-USF1Q18(Sep)F2QE18(Dec)F3QE18(Mar)FY2018EFY2019EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$575.7$620.0$620.5$600mto$640m$593.9$601.7$2,402$2,418$2,455$2,498%Q/Qchng-4.4%7.7%7.8%+4.2%to+11.2%-4.2%-3.0%%Y/Ychng2.5%12.5%12.6%2.2%3.5%4.6%5.0%2.2%3.3%Seasonal(5YMedian)-3.4%-2.3%1.8%GrossMargin66.9%67.0%66.8%66%to68%66.8%66.8%67.0%66.6%67.3%66.9%OperatingExpenses$182$193.7$190.4$760.5$764.7OperatingMargin35.2%35.8%34.7%35.3%36.2%NetIncome$172$184.4$171.3$708.8$737.5NetMargin29.9%29.7%28.9%29.5%30.0%EPS(Cont.Ops,ex-opts)*$0.66$0.71$0.66$2.72$2.82EPS(Cont.Ops,w-opts)*$0.60$0.64$0.65$0.61-$0.67$0.60$0.62$2.48$2.53$2.58$2.67Fullydilutedshares286.4286.4286.4286.4286.3Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■DiversifiedanalogexposureoutsidetraditionalPCs.Maximisdiversifiedwithexposuretoallthemarketsexceptcomputingwithgoodexposureacrossauto,factoryautomation,datacenterandconsumer.Thecompanyhasmadetransformationalapproachestonarrowitsproductlinesandimproveitsmanufacturingstrategy.■NewfinancialtargetsinSeptember.ThecompanyraisedGMsfrom67-70%andoperatingmarginsto37-40%longtermwithopexgrowingathalftherateofsaleswhichcaneventuallydriveUS$3.50FCF/share.■Cyclemetricsingoodshape.Maximbelievescyclicalityiscomingdownanditisnotseeingbigsignsinitsowndataofcyclechangessuchasleadtimescomingfromcustomersorabilitytodeliverextendingorinventoryrisinginthechannel.■Short-termchannelinventorygrowthtocomebackdown.Lastquarteritdidseeabitofincreaseindistributorchannelinventoryfrom61daysto68daysvs55-60daystargetlevelfordiscreteevents(stockingofFutureelectronicsadded1-2days,movinglowermarginproductsinTaiwanfromdirectanddistributionandrampforahotproductlaunchwhichadded2-3days)butexpectsthattocomebackdowntolow60sdays.■Growthratesathighsingledigitslongterm.Maximlong-termviewsitsgrowthashigh-singledigitsbasedonablendofautomotivemaintaininglow-teensgrowth,industrialinhighsingledigits,communicationsinmid-singledigitsandconsumerflattish.■4Q17growthhasacoupleone-timefactorshelpingit.MaximguidedUS$620mnatthemidpointfor4Q17with(1)US$20mntotransitionAvnetNorthAmericafromsell-throughtosell-inasdeferredrevenueisrecognizedinaone-timeevent,and(2)4Q17isa14weekquarteraddingChristmasweekandUS$20mn,implyingabasein4Q17ofUS$580mn(+1%QoQvsnormal-1-2%QoQ,stillup5%YoY).■AutomotivehastwogrowthdriversbeyondinfotainmentforMaxim.Infotainmentisabout2/3’softheautomotivebusiness(powermanagement,USBcharging,remotetuners,seriallinks)but2otherpiecesaregrowingfaster:(1)ADASpowerandseriallinks(addsUS$50-100/contentpercar),and(2)batterymanagementchipstomonitordrainingandchargingofthebattery(uptoUS$100+).■Industrialautomationdrivingthatcategory’sgrowthuplift.MaximseesindustrialgrowthliftedbyindustrialautomationwithmorefactoryelectronicsonthefactoryfloorforsensorswhichcanimproveusefulnesswithbetterconfigurabilityaddingAsiaSemiconductorSector19

29November2017communications(Maximcandoingitusingexistingwiredtechnology).Thefactoryflooralsoneedsmoredistributedpowerwhichalsoaddsanalogcontent.■Scaleissufficienttocompete.Thecompanybelievesithasrightscaleonsalesforceandmanufacturingdemonstratedbyitsprofitabilityandcancontinuetorunindependentlyforalongperiodoftime.■Strongcashflowsandreturns.AnalogisveryprofitablewithGMsmovingfrommid-60%tohigh-60%andwiththemanufacturingtransformationtoanoutsourcevariablecostmodelisnowinthe1-3%capex/salesrangesoallowsstrongreturnsofcapital.Thecompanyisat35%FCFmarginsandnowatUS$2.86FCF/shareandcangettoUS$3.50FCF/shareinthenextfewyearsandcommitstoreturn80%toshareholders.Itsdividendisgoinguphighsingledigitsperyearwiththeremainderbackfrombuybacks.MellanoxTechnologiesPresenter:JacobShulman,CFOAnalyst:JohnPitzerFigure18:MellanoxearningssnapshotMLNX-USSep-17Dec-17EMar-18ECY2017ECY2018EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$225.7$235.0$235.5$230-240m$217.5$218.4$861.3$861.8$986.5$966.1%Q/Qchng6.5%4.1%4.4%+1.9%to+6.3%q/q-7.4%-7.3%%Y/Ychng0.7%6.0%5.0%15.3%(1.5%)0.4%0.5%14.5%12.1%Seasonality6.0%1.4%1.4%-6.5%-6.5%GrossMargin(Non-GAAP)70.7%69.5%69.8%69-70%69.5%69.8%70.6%70.7%70.1%69.3%OperatingExpenses(Non-GAAP)$121.0$126.0$125-127m$127.9$489.8$539.7OperatingMargin(Non-GAAP)17.1%15.9%10.7%13.7%15.4%NetIncome(ex-options)$36.6$35.5$21.7$109.2$144.4NetMargin16.2%15.1%10.0%12.7%14.6%EPS(Non-GAAPex-SBC)$0.71$0.68$0.68Implied~$0.68$0.42$0.46$2.13$2.11$2.75$2.59EPS(GAAP)$0.07$0.07-$0.19-$0.26$0.47Non-GAAPFullyDilutedShares51.752.051.7-52.2m52.251.352.6Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■MellanoxWell-LeveredtoDataGrowth.NetworkisbecomingamoreimportantcomponentoftheDataCenter–specificallyMoore’sLawisslowingdownwhichhasledtoincrementalinnovationinnetworking.MellanoxwillcontinuetobenefitfromtheongoingtransitiontoEthernet–50%ofrevenuetoday.■IBHeadwindsSubsiding.MellanoxsufferedIBheadwindsdriveninpartbycustomerM&A–goingforward,MellanoxbelievesthatcustomershavecompletedM&Aintegrationandthatthebusinesswillimprove.MellanoxisalsoseeingothercustomerscomeoutwithnewproductsusingIBinstorage–whichwillhelpIBtogrowin2018.■SignificantGrowthinEthernet.Mellanoxhasestablishedleadershipin25Gb/s+-andasadoptioncontinuesexpectstoseesignificantgrowth.MellanoxhasalreadypenetratedU.S.hyperscalersandisgainingtractioninAsia(BABAthefirsttodeploy)withotherstoadoptin2018.■EthernetSwitchingisshowinghighergrowth.Nowamaterialcontributiontorevenuegrew27%QoQinC3Q–andwillcontinuetobeasignificantgrowthdriver.Mellanoxisseeingvariousformsofengagementfromswitchtoboxwithseveralsignificantdesignwins(HPEandahandfulofotherOEMs).AsiaSemiconductorSector20

29November2017■CompetitiveenvironmentinInfiniBand.HPCisaverylucrativemarket–ourleadershipinIBhelpsmaintainleadershipinEthernet.EDRup47%YoYinC3QwhilenonEDRdown–HDR200GB+comingoutin2018,HPCwillstartadoptingrightawayandwillfurtherMellanox’stechnologicallead.Instorageandembedded–expectmergerpainstogoawayin2018.■Scalenotessentialinproducinggoodproducts.MoredollarsdoesnotleadtosuperiorproductcitingtheexampleofIntel’sOPA.Mellanoxisinvestingforfuturegrowth–BlueField,Ethernetswitching,HDR.■OperatingIncomeleverageontheCome.MellanoxreiterateditsgoaltogrowRevfasterthanoperatingexpenseandnotedthat2019willmarkareturnto20%+OpM.Mellanoxnotedthatasignificantportionofoperatingexpenseisspentonnewproductsandthat60%ofoperatingexpenseissalaryrelated.IngeneralMellanoxwillcontinuetoinvestbutatamutedrate–operatingexpensewillbedependentontherolloutofnewproductsin2018andtheCompanyistargetingflatheadcount.MicronTechnologyPresenter:SanjayMehrotra,PresidentandCEOAnalyst:JohnPitzerFigure19:MicronearningssnapshotMUAug-17Nov-17EFeb-18ECY2018ECY2019EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$6,138$6,299$6,372$6.10-6.50bn$6,053$6,055$24,807$24,540$26,161$24,588%Q/Qchng10.3%2.6%3.8%-3.9%-5.0%%Y/Ychng90.8%58.7%30.2%9.5%8.3%5.5%0.2%GrossMargin51.3%53.2%52.5%50.0%-54.0%52.6%51.1%51.9%48.5%52.5%45.7%TotalOperatingExpenses$601$600$575-$625$590$2,409$2,448OperatingIncome$2,546$2,753$2.65-$2.85bn$2,593$10,462$11,293OperatingMargin41.5%43.7%42.8%42.2%43.2%NetIncome(w/options)$2,330$2,516$2,331$9,284$9,911NetMargin38.0%39.9%38.5%37.4%37.9%EPS(ProFormaw/options)$1.97$2.11$1.95$7.73$8.16EPS(ProFormaexoptions)$2.02$2.16$2.16$2.09-$2.23$2.00$1.91$7.92$7.36$8.35$6.21EPS(GAAP)$1.90$2.09$1.93$7.64$8.06DilutedSharesOutstanding1,181.01,191.01,194.61,200.71,214.4FreeCashFlow$1,445$1,464$1,710$6,007$8,788FCFpershare$1.22$1.23$1.43$5.00$7.24Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastream■Wellpositionedfortheseculargrowthdriversinmemory.SanjayMehrotrahasbeenatMicronforsixmonthsbutviewsitasthemostexcitingtimeinhis35yearsintheindustrywiththedriversfromAI,driverlesscarsandIoTwhichareallseculardriversformemory.ThecompanywithstrongportfolioacrossDRAM,NANDandNORcanaddressthesemarkets.Focusisonacceleratingtimetomarketonnewnodestolowercoststonarrowthegaptotheleaderandbuiltaportfolioofhighvaluesolutions.InNANDithaslowcostCMOSunderarraystructurethatitcanbuildintohighvalueSSDandMCPsolutionsformobilecombiningDRAMandNAND.■DRAMdemandmaystilloutstripsupplyin2018.MicronbelievesindustrydemandforDRAMwillbea20-25%CAGRthenextfewyears.In2018itexpectssupplygrowthwillbe20%butdemandmayremainsomewhatstronger.Itstillseesserverandautomotivedemandgrowthwellabovethedemandgrowth.■OptimisticonoverallNANDmarketconditions.ThecompanyisnottooconcernedaboutNANDsupplyover-shootingdemand.3DNANDwillget100%bitgrowthmovingfrom32-layerto64-layerbutcomesinovermulti-yearsandthenexttransitionswillofferlessbitgrowth.ThecompanystillseesahighpenetrationpotentialforSSDforcomputeanddatacenterIOPimprovement.ThecompanyisoptimisticonNANDthatcouldkeeppricedeclinesslowerthancoststructureimprovements.AsiaSemiconductorSector21

29November2017■NANDsupplygrowthhigherin2018butcouldbesoakedupbypent-updemand.Micronseessupplygrowthinthehigh-30%in2017andwillapproach50%in2018.Itbelieveswithpent-updemandacrossendmarketsforNANDwilldrivegreaterpenetrationincloud,enterpriseandmobile.Thecompanybelievesinventorylevelsareveryhealthynowandnotedthatduetothehigherpricesofmemorymeanshigherdollarvalueofinventorymeansthegrowthinbitsofmemoryinventoryisnotashigh.Thecompanyalsodoesnotseeanysignsofdouble-ordering.■NANDcompetitivenessforMicronimprovingfrom2Dto3D.Micron’slast2Dnodewasnotthatcompetitivebut3Disverycostcompetitiveon32-layerandimprovingfurtherwith64-layernowatteens%ofmixwithmatureyieldsbytheendofthisyearandgettingtomajorityby2HFY18(Aug).ThecompanyisnowfocusedonexpandingitsNANDintomoremulti-chippackagesanditsSSDportfolioforhighervaluesolutions.■IPandengineeringyearsasabarriertoChina.Micronindicatedmemorytakesmillionsofengineeringyearsofproductionandsolutiondevelopmenttohaveabroadbasedportfoliothatiscompetitive.■Usingcashtoretirehighyieldingdebt.ThecompanyexpectstobenetcashpositiveinFY18andhaslesseneddebtbyUS$2.25bninthepastyearandwillacceleratethatdeleveraging.Thecompanywasabletoeliminatealong-datedhighyielding7.75%note.ThecompanyprefersnowtoleverageitsFCFtostrengthenthebalancesheet,fundcapexandhavecashflowforanystrategicconsiderationstokeepthecompanyinastrongcompetitiveposition.ForFY18,itdoesnotseebuybacks/dividendsbutdoesnotruleitoutlong-termifthebalancesheetstrengthens.QorvoPresenter:BobBruggeworth,CEOandMarkMurphy,CFOAnalyst:JohnPitzerFigure20:QorvoearningssnapshotQRVO-USSep-17Dec-17EMar-18ECY2017ECY2018EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$820.6NA$840.0$830-850mNA$801.0NA$3,083.0NA$3,325.0%Q/Qchng28.2%NA2.4%+1.1to+3.6%NA-4.6%NANA%Y/Ychng-5.1%NA1.7%NA26.2%NA5.3%NA7.8%Seasonal(5-yrMedian)16.0%-1.0%-1.0%-14.0%-14.0%GrossMargin47.4%NA46.9%47.5%NA48.1%NA46.3%NA47.8%OperatingExpenses$158.2OperatingMargin28.1%NA28.6%NA28.0%NA25.7%NA28.2%NetIncome$198.4NetMargin24.2%EPS(cont.ops,ex-options)$1.52NA$1.60$1.60NA$1.47NA$5.24NA$6.23EPS(GAAP)$0.27NANANANAFullydilutedshares130.8NANANANASource:Companydata,ThomsonReutersDatastream■Qorvotargetstocontinueoutgrowingsemisinitstwocorebusinesses.QorvohastwomainbusinessesIDP(infrastructureanddefenseproducts)drivenbyGaNtechnology,IoTand5Ganditsmobilebusinessbeingdrivenbycontentexpansion.Thecompanyindicated4Gstillhasupgradesfromcarrieraggregation,LTEontheunlicensedbands,higherQAMmodemsand4x4MIMOtojoinmultipledatapaths.■IDPgrowthdrivers.ItsIDPisgrowing+20%YoYin2017andexpectsittocontinueover10%growthwithdriversfrom5G,defenseandalsoIoTdevices.Italsohasasmallopticalbusinessandmaylooktofurtherdevelopthatbusiness.AsiaSemiconductorSector22

29November2017■Contentgrowthopportunity.Qorvoexpectsdouble-digitRFgrowthtocontinueevenifthemarketremainsflat.Qorvoisseeinggrowthfrommorebands(onefilterperbandvsoneamplifierformultiplebands,moreintegrationoffilters,switchesandPAandmoreworldwideSKUswithdifferentcarrieraggregationcombinationswhichhashappenedatAppleandnowmovingtotheKoreancustomerandmoreChinamodels.5Gwilladdnewbandslike3.5GHzand6GHzplusopportunitiesfromrefarmedbands.■FocusedongainingBAWshare.QorvoisfocusedonwinningtheBAWbasedbusinesswithitslargestcustomerandalsosupplyingcarrieraggregationsolutionsinChina.Itisbelow50%utilizedinitsTexasBAWfabbutatlowpointofutilizationandexpectsthattoimprovethroughnextyeartoward80%withinayearwithChinacarrieraggregationmovingdowntolowerpricepointsaroundRmb1500andwouldalsobehelpedbyahighbandwinataflagshipcustomer.■Othermobileproductsseeingimprovement.Thecompanyhasalsosignificantlyimprovedrawresonatorsandenhancingitsmultiplexersolutions.QorvoisalsoimprovinginWifiPasandantennatunerswhicharegrowingfasterthanRF.■Marchquartermaintainedaboveseasonal.Qorvoguideditwouldbedownlow-mid-singledigitsintheMarchquartertakingintoaccountnewprogramramps,Asiaandothercustomersandiscomingoffnotthatstrongayear.■5Gwillcomeinthemid-rangebandsfirst,mmWavewillcomeabitlater.QorvobelievesthehighbandsinthemmWavewilltaketime(2020+)butthelowerbandslikesub-6GHzincluding3.5GHzwillcontributeearlierforhandsetsandinfrastructure.T-Mobile’s600MHzwouldalsobeaddedcontentfortheRFside.TexasInstruments(TXN,$99.53,OP,TP$110)Figure21:TIearningssnapshotTXNSep-17Dec-17EMar-18ECY17ECY18EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$4,116$3,720$3,736$3,570to$3,870$3,608$3,632$14,931$14,946$15,462$15,542%Q/Qchng11.5%-9.6%-9.2%-13.3%to-6.0%-3.0%-2.8%%Y/Ychng12.0%9.0%9.4%6.1%6.7%11.7%11.8%3.6%4.1%Seasonal6.3%-7.0%-3.2%GrossMargin64.5%64.6%64.2%64.4%63.9%64.1%64.0%64.9%64.6%OperatingExpense$787$729$773$3,136$3,109OperatingMargin45.4%45.0%43.0%43.1%44.8%NetMargin32.0%30.8%29.4%30.2%30.7%OperatingEPS(woptions)$1.31$1.14$1.05$4.45$4.70GAAPReportedEPS$1.26$1.08$1.09$1.01-$1.15$1.02$1.03$4.34$4.35$4.48$4.54FCF/sh$0.75$1.52$1.40$1.53$1.07$4.45$4.37$5.05$4.75FullyDilutedSharecount1,0081,0081,0081,0131,008Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastreamPresenter.BrianCrutcher(COO),DavePahl(IR)Analyst.JohnPitzerKeyTakeaways:■AnalogandEmbeddedB2BFocus.TI’smanufacturingcapacity,breadthofproductportfolio,salesforcecovering80%ofTAMandwebpresencearekeycompetitiveadvantages.TheCompanyremainsfocusedonAutomotiveandIndustrial–specifictoautomotive,TIhasbeeninvestingfor25-30yearsandhasadominantposition.WhilethecompanydoesnothaveterminalshareaspirationsinAnalog,TIcontinuestogain~30-50bpsofshareperyearandistargetingevenbettersharegains.SpecifictoEmbedded,TIbelievesthereisroomtogrowOperatingMarginsfurther(35%todayvsAnalogat47%).AsiaSemiconductorSector23

29November2017■FCFGenerationandReturn:WhereasinprioryearsonlymargingrowthandbuybackscontributedtoFCFpersharegrowth,toplinerevenuegrowthisnowasignificantcontributortoFCFgrowth–andTIexpectsthistocontinue.■DistributionandWebPresence:Approximatelythreeyearsago,TIstoppedpayingdistributorsfordesignwork–TIalreadycaptures80%ofitsTAMviaitsdirectsalesforce,andcustomerbehaviorandcomfortlevelofgettinginformationdirectfromTI’swebsitehascontinuedtoincrease.Furthermore,thecompanyisstillintheearlyinningsofseeingrevenuesynergiesfromitsinvestmentsinwebanalytics.■CyclicalSmoothSailingandSustainableGrowth:AutoandIndustrialisgrowingata5-9%CAGRovertime–expectthatgrowthtocontinuedrivenbycontentgrowth.TInottryingtocallacycle–preparingforanyscenariothatthemarketwillthrow–R&DspendismostlyLTinvestments,companyknowshowtomanageexpenses.TIworkstoscrubbookings–spendalotoftimeonqualityofbacklogratherthanrawbacklogitself.Relativetoinventory–TIoperatingwithin105-135daysrange,andseeshealthyinventorylevels.■IndustrialGrowthLT:TheindustrialmarketfitsTI’scompetitiveadvantagesalmostperfectly–diversecustomerandproductbase(14differentsub-bucketswith500categoriesbeneaththat)–productlifecyclesandstickinesssimilartoAutomotivewherecustomerswanttobuypartsfor10+years.■ReiteratedM&AStrategy:RecentM&AinthespacedoesnotchangeTI’sstrategy.SpecificallyADI+LLTChasnotchangedthecompetitivemarketdynamic–TIremains#1inAnalogand#1in¾majorAnalogcategories,andstillhastowinsocketbysocketandproductbyproduct.TIreiterateditsM&Acriteria(Analog,B2Bfocus,ROIC>WACC,catalogportfolio)andhighlightedthatit’sbeenabletoachievebetterrevenuegrowth,scaleandsharegainsfromitsorganicbusiness–specificallyTIhasbeenabletoorganicallyadd~$1.5bninRevfrom2016-2017(sameamountasLLTC).Xilinx(Xilinx,$71.97,OP,TP$75)Figure22:XilinxearningssnapshotXLNXSep-17Dec-17EMar-18EFY2018EFY2019EReportedCSConsGuidanceCSConsCSConsCSConsRevenue$619.5$630.0$630.0$615.0m-$645.0m$639.5$642.5$2,504.4$2,507.4$2,658.3$2,660.0%Q/Qchng0.7%1.7%1.7%-0.7%to+4.1%q/q1.5%2.0%%Y/Ychng7.0%7.6%7.6%4.9%5.4%6.6%6.7%6.1%6.1%Seasonality-1.6%-1.8%2.0%GrossMargin70.2%70.0%70.0%69.0%to71.0%70.0%69.7%69.7%69.5%69.8%69.7%OperatingExpenses$249.5$260.0$260.0m$252.7$1,005.2$1,040OperatingMargin29.9%28.7%28.7%30.5%30.5%29.6%29.6%30.6%30.8%NetIncome$167.5$161.9TaxRate12.5%$176.3$673$738NetMargin32.9%31.5%33.3%32.5%33.3%EPS(pf,ex-SBC)$0.79$0.77$0.83$3.14$3.48EPS(pf,w/SBC)$0.65$0.63$0.63Implied$0.63$0.69$0.69$2.60$2.59$2.91$2.86EPS(GAAP)$0.65$0.63$0.69$2.60$2.91Fullydilutedshares258.2257.0255.7259.2253.7Source:Companydata,CreditSuisseestimates,ThomsonReutersDatastreamPresenter.LorenzoFlores,CFOAnalyst.JohnPitzer■GrowthvsReturns:Xilinxbelievesitneedstocontinuetoinvesttodeliveracompellingvaluepropositiontocustomers.Whileitsproductsarerelativelyhardertousethanstandardsolutionsbecausetheyrequirecustomerstoprogramthem–theCompanyhassuccessfullyinvestedinimprovingeaseofuse.XilinxhasgrownAsiaSemiconductorSector24

29November2017revenueYoYforthelasteightquarters–indicativeofbroad-basedcustomerandend-marketdemand.■SoftwareAcceleration:SDAccelbecamebroadlyavailableonAWSinSept,andXilinxcontinuestorefineandevolveitssoftwareplatform.ImportantlyotherhyperscalershaveannouncedXilinxofferings,includingBABA,Huawei,BIDU,Tencent–nowahorizontaltechnology.■HuaweiProof-Point:Huawei’sadoptionofXilinxsolutionswasaprofoundvalidationgiventheyhaveoneofthemostsophisticatedFPGAuserbases,aswellasthepresencetodrivetheofferingasaserviceandinaproprietaryenvironment.WhileXilinxhasnotsizedtheAccelerationTAMlikepeers–thecompanyestimatesitcouldrepresentUS$250mninRev(~10%),andnotedthatitisnotgoingtoaimtoservicetheentireTAM.■CommunicationsInfrastructureand5G:Xilinxhasrecentlybenefittedfromlocalgeographybuildouts(India).XilinxpreviouslynotedthatitsWirelessbusinesswillbeflat+/-$15moverthenextfewyearsaheadofthe5Gramp.Whilethecompanydoesnotseeanyindicationsofasubstantialrampaheadof2020despitepocketsofstrength(India,China)–ifthereis,Xilinxiswell-positionedon16and20nm.■Positiveon5G:MostimportantlyXilinxremainedpositiveonbroader5Gdeploymentsgiventhecompany’sRFSoC–inaggregate5GwillbeasubstantiallylargeropportunityforXilinx,butwithalonger,lessacuterollout.Thecompanyexpects5Gradiodensitytobeamultipleof4Gradiodensity.■AutosDrivingFutureGrowth:XilinxexpectsAutotobeoneofthecompany’sfastestgrowingbusinessesovernext3-5years,andthinksthemarketisgoingtobemostlydriverassist–fullyautonomouscapabilitieswillbelimited.ThecompanyhasbeensuccessfulinworkingwithTier1OEMs–withalmost100vehiclesontheroadtodaythatofferXilinxdriverassistcapabilities.■Industrialgrowthbroadbasedandseeinggoodgrowth.Xilinx’sIndustrialbusinessremainsbroad-based(Mil/Aero,Factoryautomation,medicaldevices,test/measurementandemulation)–specificallythecompany’semulationandprototypingbusinesshasmorethandoubledoverthepast4-5years.■Tryingtodriveoperatingleverage.Xilinxisfocusedondrivingoperatingleverageandexpectstobegintape-outsfor7nminFY19–whichwillbeextendedoverthecourseofseveralyearsAsiaSemiconductorSector25

29November2017CompaniesMentioned(Priceasof29-Nov-2017)ASMLHoldingN.V.(ASML.AS,€155.2)AdvancedMicroDevices,Inc.(AMD.OQ,$11.17)AlibabaGroupHoldingLimited(BABA.N,$186.69)AmkorTechnologyInc.(AMKR.OQ,$11.42)AnalogDevicesInc.(ADI.OQ,$87.07)AppliedMaterialsInc.(AMAT.OQ,$57.33)Corning(GLW.N,$32.44)CypressSemiconductorCorp.(CY.OQ,$16.87)Google(GOOAV.OQ^D14)HimaxTechnologies,Inc.(HIMX.OQ,$13.36)IntegratedDvc(IDTI.OQ,$32.01)IntelCorp.(INTC.OQ,$44.73)InternationalBusinessMachinesCorp.(IBM.N,$152.47)KLA-TencorCorp.(KLAC.OQ,$107.16)LamResearchCorp.(LRCX.OQ,$213.14)MaximIntegratedProducts(MXIM.OQ,$53.86)MicrochipTechnologyInc.(MCHP.OQ,$90.58)MicronTechnologyInc.(MU.OQ,$47.93)Microsoft(MSFT.OQ,$84.88)NVIDIACorporation(NVDA.OQ,$210.71)Qorvo(QRVO.OQ,$79.03)SemiconductorManufacturingInternationalCorp.(0981.HK,HK$11.2)SiliconLaboratoriesInc.(SLAB.OQ,$94.15)SiliconMtnTec(SIMO.OQ,$49.5)TeradyneInc.(TER.N,$42.99)TexasInstrumentsInc.(TXN.OQ,$99.48)Xilinx(XLNX.OQ,$72.17)DisclosureAppendixAnalystCertificationI,RandyAbrams,CFA,certifythat(1)theviewsexpressedinthisreportaccuratelyreflectmypersonalviewsaboutallofthesubjectcompaniesandsecuritiesand(2)nopartofmycompensationwas,isorwillbedirectlyorindirectlyrelatedtothespecificrecommendationsorviewsexpressedinthisreport.Theanalyst(s)responsibleforpreparingthisresearchreportreceivedCompensationthatisbaseduponvariousfactorsincludingCreditSuisse"stotalrevenues,aportionofwhicharegeneratedbyCreditSuisse"sinvestmentbankingactivitiesAsofDecember10,2012Analysts’stockratingaredefinedasfollows:Outperform(O):Thestock’stotalreturnisexpectedtooutperformtherelevantbenchmark*overthenext12months.Neutral(N):Thestock’stotalreturnisexpectedtobeinlinewiththerelevantbenchmark*overthenext12months.Underperform(U):Thestock’stotalreturnisexpectedtounderperformtherelevantbenchmark*overthenext12months.*Relevantbenchmarkbyregion:Asof10thDecember2012,Japaneseratingsarebasedonastock’stotalreturnrelativetotheanalyst"scoverageuniversewhichconsistsofallcompaniescoveredbytheanalystwithintherelevantsector,withOutperformsrepresentingthemostattractive,Neutralsthelessattractive,andUnderperformstheleastattractiveinvestmentopportunities.Asof2ndOctober2012,U.S.andCanadianaswellasEuropeanratingsarebasedonastock’stotalreturnrelativetotheanalyst"scoverageuniversewhichconsistsofallcompaniescoveredbytheanalystwithintherelevantsector,withOutperformsrepresentingthemostattractive,Neutralsthelessattractive,andUnderperformstheleastattractiveinvestmentopportunities.ForLatinAmericanandnon-JapanAsiastocks,ratingsarebasedonastock’stotalreturnrelativetotheaveragetotalreturnoftherelevantcountryorregionalbenchmark;priorto2ndOctober2012U.S.andCanadianratingswerebasedon(1)astock’sabsolutetotalreturnpotentialtoitscurrentsharepriceand(2)therelativeattractivenessofastock’stotalreturnpotentialwithinananalyst’scoverageuniverse.ForAustralianandNewZealandstocks,theexpectedtotalreturn(ETR)calculationincludes12-monthrollingdividendyield.AnOutperformratingisassignedwhereanETRisgreaterthanorequalto7.5%;UnderperformwhereanETRlessthanorequalto5%.ANeutralmaybeassignedwheretheETRisbetween-5%and15%.TheoverlappingratingrangeallowsanalyststoassignaratingthatputsETRinthecontextofassociatedrisks.Priorto18May2015,ETRrangesforOutperformandUnderperformratingsdidnotoverlapwithNeutralthresholdsbetween15%and7.5%,whichwasinoperationfrom7July2011.Restricted(R):Incertaincircumstances,CreditSuissepolicyand/orapplicablelawandregulationsprecludecertaintypesofcommunications,includinganinvestmentrecommendation,duringthecourseofCreditSuisse"sengagementinaninvestmentbankingtransactionandincertainothercircumstances.NotRated(NR):CreditSuisseEquityResearchdoesnothaveaninvestmentratingorviewonthestockoranyothersecuritiesrelatedtothecompanyatthistime.NotCovered(NC):CreditSuisseEquityResearchdoesnotprovideongoingcoverageofthecompanyorofferaninvestmentratingorinvestmentviewontheequitysecurityofthecompanyorrelatedproducts.VolatilityIndicator[V]:Astockisdefinedasvolatileifthestockpricehasmovedupordownby20%ormoreinamonthinatleast8ofthepast24monthsortheanalystexpectssignificantvolatilitygoingforward.Analysts’sectorweightingsaredistinctfromanalysts’stockratingsandarebasedontheanalyst’sexpectationsforthefundamentalsand/orvaluationofthesector*relativetothegroup’shistoricfundamentalsand/orvaluation:Overweight:Theanalyst’sexpectationforthesector’sfundamentalsand/orvaluationisfavorableoverthenext12months.MarketWeight:Theanalyst’sexpectationforthesector’sfundamentalsand/orvaluationisneutraloverthenext12months.Underweight:Theanalyst’sexpectationforthesector’sfundamentalsand/orvaluationiscautiousoverthenext12months.*Ananalyst’scoveragesectorconsistsofallcompaniescoveredbytheanalystwithintherelevantsector.Ananalystmaycovermultiplesectors.AsiaSemiconductorSector26