- 378.13 KB

- 2022-04-29 14:05:41 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

'GlobalResearch13February2018UBSGlobalI/OAutos/IndustrialSemiconductorsEquitiesDon"trocktheboat-afinelybalancedoutlookGlobalSemiconductorsDavidMulholland,CFAAstrongstartto2018EbutleadindicatorsarefinelybalancedAnalystWhilethestockmarkethasseenavolatilestartto2018,resultsforthesectorweredavid.mulholland@ubs.comlargelyin-lineorslightlybetterthanexpected-particularlyintermsofrevenuegrowth.+44-20-75684069Thesectorhaspulledbackc10%fromitsrecentpeakbutwewouldnotbechasingitFrancois-XavierBouvignieshereasvaluationisstillnotparticularlycheapandouranalysisoftheleadingindicatorsAnalystshowsafinelybalancedoutlook.Webelieverevenuegrowthratescouldbepeakinginfrancois.bouvignies@ubs.comQ1forthesectorandcommentaryisalmost"asgoodasitcanget"inmanyareas-how+44-20-75687105longthislastsdependsmostlyonthemacrooutlookbutstructuraltrendsareintact.NicolasGaudoisWemaintainabalancedviewonthesectorwithapreferenceforthosewithstrongAnalystlong-termstructuraldriversparticularlyinautos(Infineon-Buy)relativetothosewithnicolas.gaudois@ubs.comshort-cycleconsumerexposure(STMicro-Sell)orstretchedvaluation(Melexis-Sell).+852-29715681BillLuHeightenedinventoryatsemis-enddemandtrendsremainkeyfromhereAnalystWithinourreviewofthedatapostQ4reporting-wefoundasignificantincreaseinbill.lu@ubs.comsemisinventorydays-112daysinQ4abovetheQ4averageof109andlastyear"s107.+852-29718360Webelievethisisduetotwofactors:1)SemiscompaniespreparingforastrongstarttoKenjiYasui2018and2)OEMinventories-particularlyinindustrialwereworkeddowninQ4thatAnalystcouldseesomerebuild.Fromheregiventheinventorysituationitiscriticalweseeakenji.yasui@ubs.comsolidstarttotheyearfromanenddemandperspective-somethingthatsofarappears+81-3-52086211tobeoccurring-howeveranychangecouldcatalyseacorrectioninthesector.PatrickHummel,CFAAnalystEnddemanddatashowsasolidstarttotheyear;autossemismarketsharepatrick.hummel@ubs.comMuchofthemacrodatasincethestartoftheyearhasbeenquiterobustparticularly+41-44-2397923PMIdataandautossalesdatasolid(Chinabetter,Europelargelyin-linebutUSweaker).DavidLesneWecurrentlyexpectgrowthwithintheautos/industrialOEMstoacceleratethroughAnalystQ1/Q2.Wealsoreviewtheperformanceinautossemisin2017andbelievethatthedavid.lesne@ubs.com+44-20-75675815mainsharegainerswereInfineonandTexasInstruments(seefigures4&5).ReiterateNeutral/selectiveviewonthesectorThesectoriscurrentlytradingat19xforwardP/Einlinewithrecentpeakof22xbutabovethehistoricforwardaverageofc17x.WithinEuropewereaminselectiveandreiterateourpreferenceforInfineon(Buy)overSTMicroelectronics(Sell)/Melexis(Sell).www.ubs.com/investmentresearchThisreporthasbeenpreparedbyUBSLimited.ANALYSTCERTIFICATIONANDREQUIREDDISCLOSURESBEGINONPAGE18.UBSdoesandseekstodobusinesswithcompaniescoveredinitsresearchreports.Asaresult,investorsshouldbeawarethatthefirmmayhaveaconflictofinterestthatcouldaffecttheobjectivityofthisreport.Investorsshouldconsiderthisreportasonlyasinglefactorinmakingtheirinvestmentdecision.

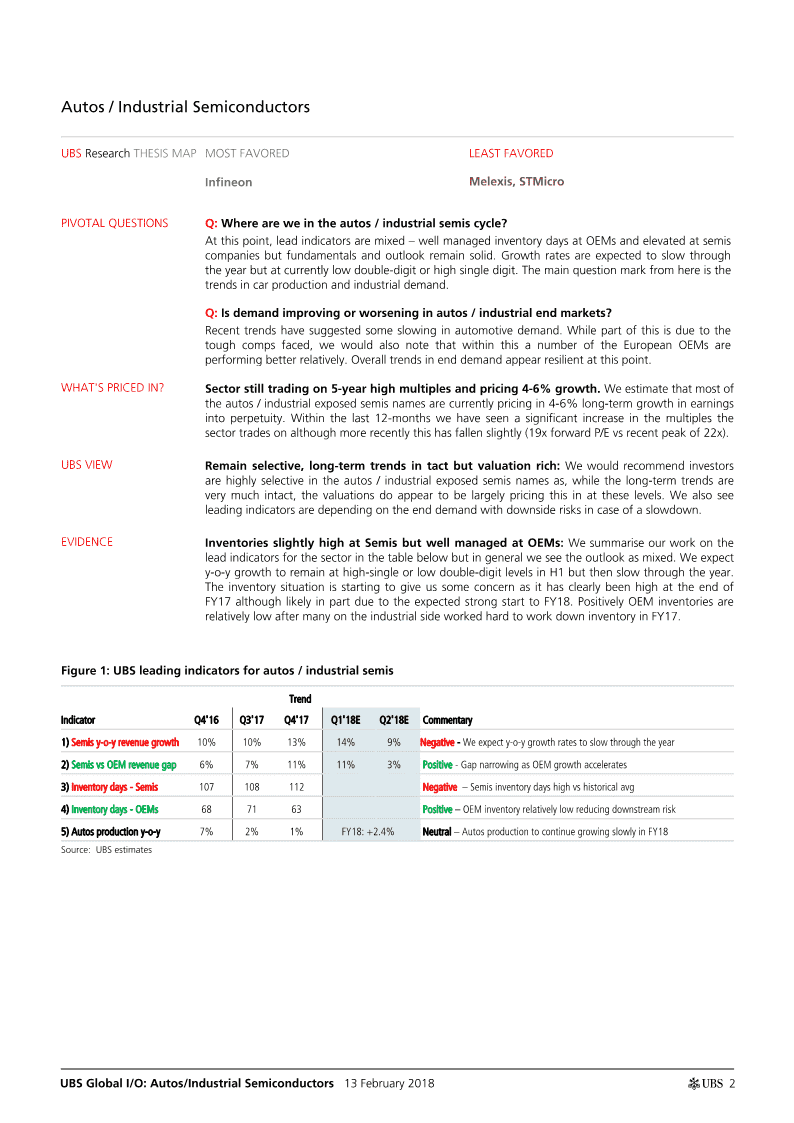

Autos/IndustrialSemiconductorsUBSResearchTHESISMAPMOSTFAVOREDLEASTFAVOREDInfineonMelexis,STMicroPIVOTALQUESTIONSQ:Whereareweintheautos/industrialsemiscycle?Atthispoint,leadindicatorsaremixed–wellmanagedinventorydaysatOEMsandelevatedatsemiscompaniesbutfundamentalsandoutlookremainsolid.Growthratesareexpectedtoslowthroughtheyearbutatcurrentlylowdouble-digitorhighsingledigit.Themainquestionmarkfromhereisthetrendsincarproductionandindustrialdemand.Q:Isdemandimprovingorworseninginautos/industrialendmarkets?Recenttrendshavesuggestedsomeslowinginautomotivedemand.Whilepartofthisisduetothetoughcompsfaced,wewouldalsonotethatwithinthisanumberoftheEuropeanOEMsareperformingbetterrelatively.Overalltrendsinenddemandappearresilientatthispoint.WHAT"SPRICEDIN?Sectorstilltradingon5-yearhighmultiplesandpricing4-6%growth.Weestimatethatmostoftheautos/industrialexposedsemisnamesarecurrentlypricingin4-6%long-termgrowthinearningsintoperpetuity.Withinthelast12-monthswehaveseenasignificantincreaseinthemultiplesthesectortradesonalthoughmorerecentlythishasfallenslightly(19xforwardP/Evsrecentpeakof22x).UBSVIEWRemainselective,long-termtrendsintactbutvaluationrich:Wewouldrecommendinvestorsarehighlyselectiveintheautos/industrialexposedsemisnamesas,whilethelong-termtrendsareverymuchintact,thevaluationsdoappeartobelargelypricingthisinattheselevels.Wealsoseeleadingindicatorsaredependingontheenddemandwithdownsiderisksincaseofaslowdown.EVIDENCEInventoriesslightlyhighatSemisbutwellmanagedatOEMs:Wesummariseourworkontheleadindicatorsforthesectorinthetablebelowbutingeneralweseetheoutlookasmixed.Weexpecty-o-ygrowthtoremainathigh-singleorlowdouble-digitlevelsinH1butthenslowthroughtheyear.TheinventorysituationisstartingtogiveussomeconcernasithasclearlybeenhighattheendofFY17althoughlikelyinpartduetotheexpectedstrongstarttoFY18.PositivelyOEMinventoriesarerelativelylowaftermanyontheindustrialsideworkedhardtoworkdowninventoryinFY17.Figure1:UBSleadingindicatorsforautos/industrialsemisTrendIndicatorQ4"16Q3"17Q4"17Q1"18EQ2"18ECommentary1)Semisy-o-yrevenuegrowth10%10%13%14%9%Negative-Weexpecty-o-ygrowthratestoslowthroughtheyear2)SemisvsOEMrevenuegap6%7%11%11%3%Positive-GapnarrowingasOEMgrowthaccelerates3)Inventorydays-Semis107108112Negative–Semisinventorydayshighvshistoricalavg4)Inventorydays-OEMs687163Positive–OEMinventoryrelativelylowreducingdownstreamrisk5)Autosproductiony-o-y7%2%1%FY18:+2.4%Neutral–AutosproductiontocontinuegrowingslowlyinFY18Source:UBSestimatesUBSGlobalI/O:Autos/IndustrialSemiconductors13February20182

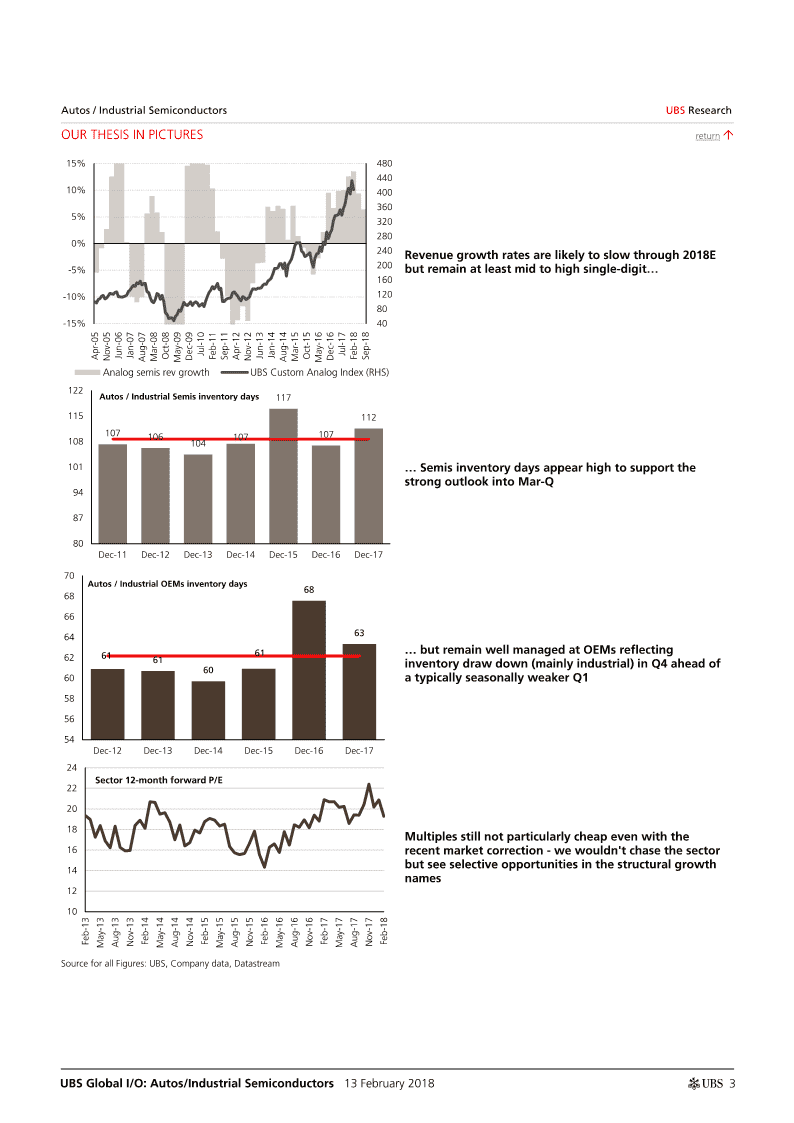

Autos/IndustrialSemiconductorsUBSResearchOURTHESISINPICTURESreturn15%48044010%4003605%3202800%240Revenuegrowthratesarelikelytoslowthrough2018E-5%200butremainatleastmidtohighsingle-digit…160-10%12080-15%40Apr-05Nov-05Jun-06Jan-07Aug-07Mar-08Oct-08May-09Dec-09Jul-10Feb-11Sep-11Apr-12Nov-12Jun-13Jan-14Aug-14Mar-15Oct-15May-16Dec-16Jul-17Feb-18Sep-18AnalogsemisrevgrowthUBSCustomAnalogIndex(RHS)122Autos/IndustrialSemisinventorydays117115112107106107107108104101…SemisinventorydaysappearhightosupportthestrongoutlookintoMar-Q948780Dec-11Dec-12Dec-13Dec-14Dec-15Dec-16Dec-1770Autos/IndustrialOEMsinventorydays6868666364626161…butremainwellmanagedatOEMsreflecting61inventorydrawdown(mainlyindustrial)inQ4aheadof6060atypicallyseasonallyweakerQ1585654Dec-12Dec-13Dec-14Dec-15Dec-16Dec-1724Sector12-monthforwardP/E222018Multiplesstillnotparticularlycheapevenwiththe16recentmarketcorrection-wewouldn"tchasethesectorbutseeselectiveopportunitiesinthestructuralgrowth14names1210Feb-13May-13Aug-13Nov-13Feb-14May-14Aug-14Nov-14Feb-15May-15Aug-15Nov-15Feb-16May-16Aug-16Nov-16Feb-17May-17Aug-17Nov-17Feb-18SourceforallFigures:UBS,Companydata,DatastreamUBSGlobalI/O:Autos/IndustrialSemiconductors13February20183

Autos/IndustrialSemiconductorsUBSResearchKEYTRENDSINQ2returnOverallgrowthacceleratedinQ4andlikelytostabiliseinQ1/Q2Q4sawagainastrongperformanceofsemisoutperformingOEMssignificantlydrivenbycontentgrowthandtheimpactofsomeconsumerramps(iPhoneX).Encouragingly,consensusnowforecastsanaccelerationofgrowthatOEMsinQ118EandthenfurtherstrengtheningintoQ218EsuchthatinQ2wenolongerforecastsemistobeoutperformingtheirpeers.Wecontinuetobelievethatthefundamentalsandoutlookaresolidthoughmarginoferrorislimitedgivenwherevaluationsarecurrentlyandslightlyelevatedinventoriesatsemis.Figure2:Semisrevenuegrowthy-o-ysurprisedagainFigure3:Semisoutperformancegaptonarrow16%20%30%14%15%20%12%10%10%5%10%0%0%8%-10%-5%6%-20%-10%4%-15%-30%2%-20%-40%0%Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Mar-18Jun-18Q2"11Q4"11Q2"12Q4"12Q2"13Q4"13Q2"14Q4"14Q2"15Q4"15Q2"16Q4"16Q2"17Q4"17Dec-17Sep-17Aug-17Jun-17Q2"18ESpread(%pts)(RHS)Semisrevs%y-o-ySource:UBS,Datastreamconsensus,CompanydataSource:UBS,CompanydataAutossemissharegainerswereInfineonandTexasInstrumentsWithannualdatareportedbymostsemiconductorcompaniesandbettervisibilityontheirendmarketexposures-wetakethisopportunitytorevisitouranalysisofthemarketsharetrendswithinautosinFigures4and5below.WefindthatTIandInfineonhavebeenthemostsuccessfulatgainingshareinthemarket.Conversely,whilestillgrowingstrongly(9-11%),NXP,STMicroandRenesasappeartobetheoneslosingshareasothersgrewinthehigh-teensin2017.WecontinuetohaveconfidencethatInfineoncansustainsharegainsbothintraditionalareas(MCU)andasnewareasitiswellexposedtogrow(e.g.EV/ADAS).Figure4:UBSestimatesofautossemismarketshare"17Figure5:Autossemissharechange("17vs."16)0%5%10%15%20%(50bps)(30bps)(10bps)10bps30bps50bpsNXP19.7%TexasInstruments35bpsRenesas19.1%Infineon23bpsInfineon18.1%Maxim13bpsTexasInstruments14.5%Nvidia6bpsSTMicro11.7%Melexis2bpsONSemi8.7%ONSemi0bpsNvidia2.9%NXP-17bpsMelexis2.7%STMicro-29bpsRenesas-33bpsMaxim2.5%Source:UBSestimatesSource:UBSestimatesUBSGlobalI/O:Autos/IndustrialSemiconductors13February20184

CommentsfromOEMsconsistentwithouranalysisWealsolookedatcommentsfromsomeselectOEMsregardinginventoriesinthetablebelow.Asasummary,webelievethesituationisstillundercontrolbutwithsomeriskifenddemandmateriallyslows.Therewasaclearfocusintheindustrialspaceoninventorymanagement.Figure6:CommentsoninventoryfromAutomotiveOEMsCompaniesCommentsTheyreducedtheirU.S.dealerinventoryasplanned.Endedtheyearwith63dayssupplyand753,000unitsofdealerinventory,down8daysandGeneralMotors92,000unitsfromtheendof2017,bothfarsurpassingthetargets.Theyexpecttocontinuetorunleaninventoriesonago-forwardbasis.Theyhadtoreducedealerinventoriesduringthe3Q.TheyareimplementingmeasuressuchasthereductioninU.S.inventorytoaligntheirU.S.NissanbusinesswithmarkettrendsandarealsoontracktofullrecoveryfromthevehicleinspectionissueinJapanbytheendoftheFY.InQ4,expectinventorywillbenarroweddownby100,000unitsorevenmorethan100,000unitsbytheendofQ4vsQ3end.Theyhavelowinventorylevelsandthey"reallmovingveryquickly.Lowinventorylevelswereforusedandnewtrucks.BothinventorylevelsandVolvoactuallyturnaroundratesandpricingaresomewhatpositiveprimarilyontheVolvoside...Source:Companyconferencecalltranscript,UBSFigure7:CommentsoninventoryfromindustrialOEMsCompaniesCommentsInventorydaysdeclinedy-o-y,whentheirbusinessstartedtocapturesignificantgrowth.NorthAmericacustomersurveyshowedthattheArrowElectronicscompanyhadarecordlownumberofcustomerssayingtheyhadtoomuchinventory.Thecompanyisstayingaheadofthatandkeepingtheirinventorylevelswheretheycansupporttheircustomers.Theincreaseininventoryrepresentsadditionalinvestmentsrelatedtoastrongbook-to-billandextendingleadtimestosupporttheseasonallyAvnetstronggrowthintheWesternregionsintheMarchquarter.Theyfeelprettygoodwiththeinventorylevelsrightnow,anddon"tseethemincreasingintheMarch-Q.Betterinventoryflowsfromhighershipmentsandhigher-than-expectedprogressflowsofabout$700mn.Thefinishedgoodsburn-downwasreallyfavorable.Turnswereflatfortheyearoninventory.TheCompanyexpectstoimproveinventoryturnsforthePowerbizby2xby2020fromGeneralElectricthecurrent4turnsin2018,eveninalowervolumeworldthroughagreatfocusonmaterialmanagementprocesses,acommitmenttolean,andtheliquidationofexistingfinishedgoods.Thisrequiresa$1bnreductionininventorybalancesin2018.TheydrivetoincreaseworkingcapitalefficienciescontinuedtoyieldresultsasinventoryasapercentageofsalescontinuedtodecreasetoPhillips13.2%,ay-o-yimprovementof120basispoints...Asignificantgrowthcontributioncamefromtheshort-cyclebusinesses,drivenbystrongdemandfromautomotiveandmachinebuildingSiemenscustomers.Again,Chinawasstandingoutwith24%revenuegrowth,benefitingalsofromrestockingeffectinthedistributionchannels.Thecompanyexpectstheshort-cyclemomentumtomoderategoingforward..Source:Companytranscript,UBSLookingattheinventorylevelbysubsector,weseeautosOEMSstillareatslightlyhighlevelsalthoughwewouldnotethatsomeofthemajorOEMs(VW,Daimler)haveyettoreport.ForindustrialwefoundsignificantlylowerinventoryinQ4reflectingstrongworkingcapitalmanagementbycorporatestodrivecashgenerationandalsoaheadofatypicallyseasonallyweakerQ1.TheIndustrialOEMinventorydaysweshowbelowhasbeenadjustedtoexcludecompanieswherewehaveseenastepchangeininventoriesrelatedtoeitheracquisitionsofdisposalswhichdisruptthetimeserieselementofourdata.UBSGlobalI/O:Autos/IndustrialSemiconductors13February20185

Figure8:AutoOEMsinventorydaysvshistoricstillFigure9:IndustrialOEMsinventorydayslowerthanrelativelyhighvstheaverageofthelast5yearsnormalseasonality4988488648864747464684818246824545804580784478754376427441724070Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17InventoryDaysAverageInventoryDaysAverageSource:UBS,CompanydataSource:UBS,Companydata,excludingAvnet,JohnsonControlsandEmersonthatwewouldnormallyincludeforcomparabilityreasonsWeanalysebelowtheprincipaldrivers.Fromaquantitativeperspective,NissanandToyotaaredrivingtheincreaseinautosatOEMsoffsetbyVolvoandSuzuki.Ontheindustrialside,restockingatdistributorchannels,inventorydrawdowninQ4andliquidationofshipmentshadledtosignificantlylowerinventoryatGE,SiemensandPhilips.Figure10:Autoinventorydayschangey-o-y:NissanandFigure11:Industrialinventorydayschangey-o-yToyotadrivingthedecreaseoffsetbySuzukideclining2515020100155010500(50)(5)(100)(10)(150)(15)Jun-15Dec-15Jun-16Dec-16Jun-17Dec-17(20)SiemensGEABBJun-15Dec-15Jun-16Dec-16Jun-17Dec-17HoneywellPhilipsAvnetJohnsonControlsArrowEmersonToyotaGMNissanFordVolvoDensoSuzukiLegrandAtlasCopcoSource:UBSestimates,CompanydataSource:UBSestimates,CompanydataUBSGlobalI/O:Autos/IndustrialSemiconductors13February20186

Autos/IndustrialSemiconductorsUBSResearchPIVOTALQUESTIONSreturnQ:Whereareweintheanalogsemiscycle?UBSVIEWAtthispoint,leadindicatorsaremixed–wellmanagedinventorydaysatOEMsandelevatedatsemiscompaniesbutfundamentalsandoutlookremainsolid.Growthratesareexpectedtoslowthroughtheyearbutatcurrentlylowdoubledigitorhighsingledigit.Themainquestionmarkfromhereisthetrendsincarproductionandindustrialdemand.EVIDENCEOuranalysisshowsthaty-o-yrevenuegrowthislikelytosustainatleasthigh-singledigitlevelsthroughQ1/Q2.Inventoryatsemisarehigh(betteroutlookforMar-Q)butaregenerallywellmanagedatOEMsaheadofatypicallyseasaonllyweakerQ1(especiallyinIndustrial).WHAT"SPRICEDIN?Withthesectoron5-yearhighmultiplesandpricinginsolidlong-termgrowth,webelievethemarketisassumingtherecentstrengthwillsustainandisnotpricinginasignificantcorrection(wedon"tenvisageoneatpresent).Leadindicators#1y-o-ysemisgrowthThefirstleadingindicatorwefocuson,andoftenthemostimportantone,isthetrendiny-o-ygrowthforthesector.Lookingattheautosandindustrialsemiscompanies,mostguidedforhighsingledigittolowteensgrowthinrevenueonay-o-ybasisforQ1.TheexceptionsthatareoutperforminginQ1are:STMicrowithcontinuedstronggrowthy-o-yasitscontentgainsintheiPhoneXannualiseandInfineonbenefitsfromgreaterEurorevenueexposurebenefitingfromcurrency.Figure12:y-o-yrevenuetrendcomparison(inUS$)Figure13:q-o-qrevenuetrendcomparison(inUS$)35%20%30%16%25%22%12%21%8%8%20%6%15%13%4%3%11%10%9%0%10%7%7%-4%5%-1%-1%-3%-8%0%-12%STMIFXTXNONN-9%MLXSIFXRenesasMaximMCHPONNTXNSTM-10%MLXSMaximMCHPRenesasDec-QMar-QguideDec-QMar-QguideSource:Companyreports;NOTE:Dec-QguidehasbeenconvertedintoUS$usingSource:Companyreports;NOTE:Dec-QguidehasbeenconvertedintoUS$usingassumedexchangeratesbycompanyorspotratewherenonespecifiedassumedexchangeratesbycompanyorspotratewherenonespecifiedHistoricallyithasprovenrighttoturnmorecautiousonthesectorafewmonthsaheadofthepeakasthey-o-ygrowthtrendsslow.However,inmorerecentcyclesthestocks–drivenbyfiscaleasinginparticular–havecontinuedtoseemultipleUBSGlobalI/O:Autos/IndustrialSemiconductors13February20187

expansionevenaftertheleadindicatorshaveturned.Atthispoint-theupcycleforthesectorhassustainedlongerthaniteverdoes(longernowthantheup-cyclepostthefinancialcrisis)andascompsbecometougheritishardtobelievethatgrowthratescancontinuetosurpriseontheupside.Weexpectgrowthrateswillstarttoslowthrough2018andthatthiswillbecomeanincreasingheadwindforthestocks.Werecognisethereismuchgreaterconfidenceinthestructuraldriversforthesectorthatmaydampenthedownsidecorrectionasgrowthratesslow.Figure14:RevenuegrowthlikelytopeakinQ4andslowinQ1/Q215%48044010%4003605%3202800%240200-5%160-10%12080-15%40Apr-05Jul-05Oct-05Jan-06Apr-06Jul-06Oct-06Jan-07Apr-07Jul-07Oct-07Jan-08Apr-08Jul-08Oct-08Jan-09Apr-09Jul-09Oct-09Jan-10Apr-10Jul-10Oct-10Jan-11Apr-11Jul-11Oct-11Jan-12Apr-12Jul-12Oct-12Jan-13Apr-13Jul-13Oct-13Jan-14Apr-14Jul-14Oct-14Jan-15Apr-15Jul-15Oct-15Jan-16Apr-16Jul-16Oct-16Jan-17Apr-17Jul-17Oct-17Jan-18Apr-18Jul-18AnalogsemisrevgrowthUBSCustomAnalogIndex(RHS)Source:UBSestimates,Companydata,IBESconsensusNOTE:AnalogsemisindexcalculatedasasimpleaverageoftheperformanceofthesharepricesofAnalogDevices,ams,TexasInstruments,STMicro,Infineon,ONSemi,Microchip,Maxim,MelexisandNXP#2–Semisvs.OEMsrevenuegap-supportiveAnotherfactorwewatchcloselyistherelativeperformanceofthesemisandtheirOEMcustomers.Withintheautosandindustrialspace-thesemisgrowthrateshaverecentlybeenboostedbythecontentwinsoftheseminameswithiPhoneexposureandweareencouragedthatastheseannualisethetrendsaremoreconsistentbetweensemisandOEMs.IndeedbyQ2weseethegapdisappearingwhichweseeasencouraging.Figure15:Autos/industrialsemisvs.OEMrevs(y-o-y)20%30%15%20%10%10%5%0%0%-10%-5%-20%-10%-15%-30%-20%-40%Q2"11Q4"11Q2"12Q4"12Q2"13Q4"13Q2"14Q4"14Q2"15Q4"15Q2"16Q4"16Q2"17Q4"17Q2"18ESpread(%pts)(RHS)Semisrevs%y-o-ySource:Companydata,IBESconsensusdata,UBSestimates,(13semis,23OEMs)UBSGlobalI/O:Autos/IndustrialSemiconductors13February20188

#3–Inventories-risksriseonsemibalancesheetsLookingattheinventories,atsemis,wenoticethatthetheyareparticularlyhighgivenastrongoutlookforthefirsthalfoftheyear.Figure16:Autos/industrialsemisinventorydaysFigure17:Autos/industrialsemisinventory(US$bn)12010.511510.01109.51051009.0958.5908.085807.5Dec-10Jun-11Dec-11Jun-12Dec-12Jun-13Dec-13Jun-14Dec-14Jun-15Dec-15Jun-16Dec-16Jun-17Dec-17Dec-10Jun-11Dec-11Jun-12Dec-12Jun-13Dec-13Jun-14Dec-14Jun-15Dec-15Jun-16Dec-16Jun-17Dec-17Source:UBS,CompanydataSource:UBS,CompanydataWhenwelookattheOEMs,inventoryappearswellmanagedintotalalthoughisslightlyhighinautos(withsomekeyOEMsstilltoreport)butlowerthannormallyseeninQ4forsomeindustrialcompanies.Figure18:Auto/industrialOEMinventorydaysFigure19:Autos/industrialOEMinventory(US$m)73160701506714064130611201105810055Mar-11Jun-11Sep-11Dec-11Mar-12Jun-12Sep-12Dec-12Mar-13Jun-13Sep-13Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Mar-11Jun-11Sep-11Dec-11Mar-12Jun-12Sep-12Dec-12Mar-13Jun-13Sep-13Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Source:UBS,CompanydataSource:UBS,CompanydataIfweadjustforseasonalityandfocusonthey-o-ytrendsininventoryitreinforcesthetrendthatinventorylevelsishigheratsemis,howeverdeclinedatOEMs.Figure20:InventorylevelshigherthanavgatsemisFigure21:OEMinventorydaysarelowerthannormalQ4122701186868115113111109661071081061056364101626161616060945887568054Dec-11Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17Source:UBS,CompanydataSource:UBS,Companydata,excludingAvnet,JohnsonControlsandEmersonUBSGlobalI/O:Autos/IndustrialSemiconductors13February20189

Segmentingtheinventorydaysintothesub-industries,while,therehasbeenanincreasewithintheautosOEMs,industrialsupplierssawasubstantialdecline.ThetrendismoreconsistentwithintheautosOEMswherenearlyallcompanieshaveseenincreaseininventorydays(apartfromSuzukiandVolvo).FortheindustrialOEMstheprimarydeclineisfromPhillips,SiemensandGE.Themainreasonfordeclineinrestockingatthedistributionchannel,wasthatfinishedgoodsandshipmentswereliquidated.Figure22:AutosOEMsinventorydaysFigure23:IndustrialOEMsinventorydays50494910049959449489593924848489189899190904847898947904786474686464685464546818245454580787544437543704265416040Sep-13Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Sep-13Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Source:UBS,CompanydataSource:UBS,CompanydataFigure24:AutoOEMsinventorydaysvshistoricstillFigure25:IndustrialOEMsinventorydayvshistoricisrelativelyhighvstheaverageofthelast5yearssignificantlylower4988488648864747464684818246824545804580784478754376427441724070Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17Dec-12Dec-13Dec-14Dec-15Dec-16Dec-17InventoryDaysAverageInventoryDaysAverageSource:UBS,CompanydataSource:UBS,Companydata,excludingAvnet,JohnsonControlsandEmersonforcomparabilitywhichwewouldnormallyincludeUBSGlobalI/O:Autos/IndustrialSemiconductors13February201810

Autos/IndustrialSemiconductorsUBSResearchPIVOTALQUESTIONSreturnQ:Isdemandimprovingorworseninginautos/industrialendmarkets?UBSVIEWRecenttrendshavesuggestedsomeslowinginautomotivedemand.Whilepartofthisisduetothetoughcompsfaced,wewouldalsonotethatwithinthisanumberoftheEuropeanOEMsareperformingbetterrelatively.Overalltrendsinenddemandappearresilientatthispoint.EVIDENCEDatafromQ4showthatAutomotiveproductionisgrowing+2%after+2%inQ3.WHAT"SPRICEDIN?Withthesectoron5-yearhighmultiplesandpricinginsolidlong-termgrowth,webelievethemarketisassumingtherecentstrengthwillsustainandisnotpricinginasignificantcorrection(wedon"tenvisageoneatpresent).Automotive–EmergingcountriesandEuropestrong,slightslowdowninChinabutexpectedtoaccelerateinQ4.Q4resultsand2018guidancewilllikelysupporttherecentoutperformanceofthesector,eventhoughwedon"texpectsignificantearningsrevisions(savetheimpactfromtheUStaxreformonGermanOEMsandFCA).Weexpectmoderatevolumegrowth(+2.2%globallyy/y)askeypositivedriver.Figure26:SalesgrowthinkeymarketsinDecemberFigure27:UnitsalesgrowthbyOEMinDecemberAudiRussiaBMW(incl.Mini)VWGroupBrazilHonda*Ford(USonly)JapanMerc(incl.Smart)Toyota*ChinaRenaultNissan*EUBig5GM(USonly)PSAUSHyundai**FCA(US+Europe)SouthKoreaKia**-25%-20%-15%-10%-5%0%5%10%15%20%-30%-20%-10%0%10%20%DecemberYoYFY17DecemberYoYFY17Source:Bloomberg,respectivecarassociations,UBS.Source:Companydata,UBS.Note:*DecproductiondataforToyota&HondaandDecsalesforNissan.Note:**DecsalesdataforHyundaiandKia.UBSGlobalI/O:Autos/IndustrialSemiconductors13February201811

Figure28:EUbig5-Carsalesgrowth(rollingquarters)Figure29:China-Carsalesgrowth(rollingquarters)3,700,00012%7,900,00030%7,200,00024%3,200,0009%6,500,00018%2,700,0006%5,800,00012%2,200,0003%5,100,0006%4,400,0001,700,0000%3,700,0000%1,200,000-3%3,000,000-6%Sep-13Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Jul-13Oct-13Jan-14Apr-14Jul-14Oct-14Jan-15Apr-15Jul-15Oct-15Jan-16Apr-16Jul-16Oct-16Jan-17Apr-17Jul-17Oct-17carsales(units)%y-o-ycarsales(units)%y-o-ySource:UBS,ACEASource:UBS,CAAMAsshownbelow,wecontinuetoexpect2%salesgrowthforthefullyear2018globallyand+2.4%y-o-yfortheproduction.Figure30:US-Carsalesgrowth(rollingquarters)Figure31:UBSsalesforecastacrossregions30.07%14%12%12%12%25.04%12%10%10%10%10%1%20.08%-2%6%5%15.0-5%4%2%3%2%2%3%2%10.0-8%2%0%0%0%0%5.0-11%-2%0%0.0-14%-4%-2%WesternRussiaUSABrazilChinaGlobalJul-14Jul-15Jul-16Jul-17EuropeOct-13Jan-14Apr-14Oct-14Jan-15Apr-15Oct-15Jan-16Apr-16Oct-16Jan-17Apr-17Oct-17Jan-182017A2018E2019Ecarsales%y-o-ySource:UBS,BloombergSource:UBSIndustrialbookingsstillfavourableInQ4’17,orderbookingswerepositivelyskewedforthemajorindustrialOEMs(exceptGE)postingincreaseinorders.BothSiemensandAtlasCopcoreportedstrongordergrowthof14%and10%y/y,respectively.Figure32:Ordersgrowth(y-o-y)–Q4"17Figure33:Ordersgrowth(y-o-y)15%14%40%10%25%10%10%5%5%-5%0%-20%-35%-5%-3%-5%-50%-10%SiemensAtlasCopcoJohnsonABBGE*Dec-13Mar-14Jun-14Sep-14Dec-14Mar-15Jun-15Sep-15Dec-15Mar-16Jun-16Sep-16Dec-16Mar-17Jun-17Sep-17Dec-17Controls**SiemensGE*JohnsonControls**Source:UBS,companydata(*GEEquipment**BuildingEfficiency)Source:UBS,companydata(*GEEquipment**BuildingEfficiency)UBSGlobalI/O:Autos/IndustrialSemiconductors13February201812

Autos/IndustrialSemiconductorsUBSResearchWHAT"SPRICEDIN?returnTocalculatewhatispricedinatcurrentlevels,weusearesidualincomemodelbasedoncurrentbookvalueandtwoyearsforwardconsensusforecasts.Thisshows(usingaconsistentdiscountrateof9%),theimpliedvalue(betweenshort-termandlong-termgrowth)foreachofthekeystocksinthesector.Figure34:CreationofvaluehorizonacrosstheAutos/IndustrialSemisspace(pricedasof08February2018)100%90%80%70%60%50%40%30%20%10%0%InfineonSTMicroMelexisRenesasCurrentearningsShort-termgrowthLong-termgrowthSource:UBSestimatesTherehasbeenasignificantincreaseinthegrowthoutlookbeingpricedintothesectorthroughthisyear.Whiletherearestillgrowthopportunitiesinthesectorweareconcernedatthecurrentvaluationlevelsacrossthesector.Theanalogandindustrialsemissectoriscurrentlytradingonone-yearfwdP/Eof19.3xbelowtherecentpeakof22xandcomparedtoitshistoricalaverageofc17.3xbutEV/EBITDAmultipleatc11.5xisstillaboveitsaveragec8.0x.WeremainNeutralinouroverallviewontheautosandindustrialnamesasvaluationmultiplesremainshigh.Figure35:Autos/IndustrialsemisForwardEV/SalesFigure36:Autos/IndustrialsemisForwardP/E5.0244.5224.03.5203.0182.5162.01.5141.0120.5-10Feb-12Jun-12Oct-12Feb-13Jun-13Oct-13Feb-14Jun-14Oct-14Feb-15Jun-15Oct-15Feb-16Jun-16Oct-16Feb-17Jun-17Oct-17Feb-18Feb-13May-13Aug-13Nov-13Feb-14May-14Aug-14Nov-14Feb-15May-15Aug-15Nov-15Feb-16May-16Aug-16Nov-16Feb-17May-17Aug-17Nov-17Feb-18Source:UBS,DataStreamSource:UBS,DataStreamUBSGlobalI/O:Autos/IndustrialSemiconductors13February201813

Weshowthemultiplesforeachcompanyinthesector;thehistoricmultiplesthesectorhastradedonandachartshowingEV/SalesagainstEBITDAmarginwhichwebelieveprovidesagoodvisualindicatortovaluationdiscrepancies.Figure37:Autos/IndustrialsemisForwardEV/EBITDAFigure38:Autos/IndustrialsemisForwardP/BV145.5135.012114.5104.093.5873.062.5542.0Feb-12Jun-12Oct-12Feb-13Jun-13Oct-13Feb-14Jun-14Oct-14Feb-15Jun-15Oct-15Feb-16Jun-16Oct-16Feb-17Jun-17Oct-17Feb-18Feb-12Jun-12Oct-12Feb-13Jun-13Oct-13Feb-14Jun-14Oct-14Feb-15Jun-15Oct-15Feb-16Jun-16Oct-16Feb-17Jun-17Oct-17Feb-18Source:UBS,DataStreamSource:UBS,DataStreamFigure39:2019EEV/Salesvs.EBITDAmarginforanalogsemis7.0EV/SalesTexasInstruments6.0AnalogDevicesMelexis5.0MicrochipTechnologyamsAGMaximIntegrated4.0R²=0.79453.0Infineon2.0ONSemiEBITDAmarginSTMicroelectronicsRenesasElectronics1.015%20%25%30%35%40%45%50%Source:UBS;Datastreamconsensususedfornon-coveredcompaniesUBSGlobalI/O:Autos/IndustrialSemiconductors13February201814

Figure40:AnalogSemisGlobalValuationMultiples(Pricedon12Feb2017)PricePriceMarketEV/SalesEV/EBITDAPrice/EarningsEBITDAMarginCompanyRating(lc)Target(lc)Cap($m)2018E2019E2018E2019E2018E2019E2018E2019EAnalogDevicesNotCovered83.93-31,2795.86.011.912.716.014.948.3%47.7%amsAGNeutral103.5092.009,3025.44.515.111.125.218.535.5%40.7%InfineonBuy21.4126.0029,4653.12.911.410.121.518.927.3%28.5%MaximIntegratedNotCovered57.95-12,6454.54.411.010.621.119.341.1%41.6%MicrochipTechnologyNotCovered81.04-18,9915.04.710.910.514.213.345.7%44.7%MelexisSell84.6057.004,1865.95.418.517.027.925.831.8%31.6%NXPNotCovered115.78-39,2534.64.010.810.615.814.342.1%37.7%ONSemiNotCovered21.15-8,9712.01.88.57.412.211.023.5%24.5%RenesasElectronicsNeutral1180.001,28018,0182.01.87.87.429.519.325.8%24.2%STMicroelectronicsSell17.2315.5018,7301.91.89.38.418.516.620.8%21.5%TEConnectivityNotCovered96.40-33,8722.62.511.510.617.316.022.3%23.0%TexasInstrumentsNotCovered100.49-99,0396.36.013.513.020.117.746.6%46.4%Mean4.13.811.710.819.917.134.2%34.3%AnalogSemisMedian4.54.211.210.619.317.133.6%34.6%Source:UBSestimates,IBESconsensususedfornon-coveredstocksButwedorecognisethatreturnsintheindustryhaveimprovedOnefactorthatdoesinpartjustifytheincreaseinmultiplesforthesectoristheincreaseinprofitabilitythatwehaveseenwhichisarguablyastructuralchangetowardshigherearningsqualityinthesectorthatithashadhistorically.Figure41:ForwardEV/EBITDAmultiplevs.EBITDAmarginFigure42:ForwardEV/EBITDAmultiplevs.EBITDAmargin1438%1440%36%121235%34%1032%1030%830%825%628%26%620%424%2415%22%020%210%Aug-11Nov-11Feb-12May-12Aug-12Nov-12Feb-13May-13Aug-13Nov-13Feb-14May-14Aug-14Nov-14Feb-15May-15Aug-15Nov-15Feb-16May-16Aug-16Nov-16Feb-17May-17Aug-17Nov-17Feb-18Nov-05Jun-06Jan-07Aug-07Mar-08Oct-08May-09Dec-09Jul-10Feb-11Sep-11Apr-12Nov-12Jun-13Jan-14Aug-14Mar-15Oct-15May-16Dec-16Jul-17Feb-18EV/EBITDAmultipleEV/EBITDAmultipleSource:UBS,DatastreamSource:UBS,DatastreamUBSGlobalI/O:Autos/IndustrialSemiconductors13February201815

UBSGlobalI/O:Autos/IndustrialSemiconductorsFigure43:RecentcommentaryfrommajoranalogsemiscompaniesCommentsCompanyDateCurrentQNextQguideInventoriesAutostrendQ3IndustrialstrendQ3Ordersandbook-to-billGeneralcommentsCo.intendstomaintaininventorybufferDown8.9%q/q,Inventorydayswereup8daysy/ytoAutodemandcontinuedtoDemandremainsstrongwithwhenaddressingtheindustrial&autoTexasInstruments23-JanDown2.9%q/qUp9.8%y/y134.Dist.Inventorystableat4wksbestrongbroad-basedgrowthmarket.AlsotocontinueincreasingconsignmentengagementFocusingoninventorybuildsandUp2%q/q,ExpectedtobegrowinMarginincreasefrombroadeningleadXilinx24-JanUp3.0%q/qinventoryisgrowinginanticipationofExpectedtobeflatq/qUp8%y/ysingledigitagainstthecompetitionandcertainmarketsthebusinessDistributorchanneldown11daysq/qExpecttobeupq/qledbyMacrolooksgood,andmfgPMIisaboveDown8.2%q/q,drivenbystrongresalesMaxim25-JanUp2.8%q/qExpectittobeupq/qfactoryautomationproduct-50%.LeadtimesarewithinnormalrangeUp13.0%y/yInventorydaysup9daysq/qforandSMBbizandnosupplyconstraintsrevenuerampinMarQSeasonalityisevolvingasportfolioevolves,Up15.4%q/q,13February2018STMicro25-JanDown10.0%q/qInventorydaysdownq/qTobeupy/y-leadingtowardshighersalesinQ3andQ4Up32.7%y/yofayearInventorylevelsdecliningatOverall1.4(vs1.2inCQ4),1.3Thedemandhasbecomemoresolid.Down2.5%q/q,BusinessmomentumInfineon31-JanUp4.0%q/qdistributors.TempinventoryadjatRemainssolidinautos(vs.1.3),1.4inIPC(vs.InventorylevelsinthedistributorspaceisonUp7.9%y/ycontinuestobestrongcustomers1.3),1.6inPMM(vs.1.2)theveryleanside.IndicationfromcustomersandmacrodataDown1%q/q,Inventorydaysat115days(+6dayExpectdtobeupq/qsiliconOnSemi5-FebDown0.9%q/qExpectedtobeflatq/qpointstocontinuingstrengthindemandinUp9.2%y/yq/q);Distisinventorywasdownq/qcarbideontracktheneartomidtermCompanyhadbroad-basedchallengesonInventorywas105days,(+10dayq/q).Down1.8%q/q,B2Bwas1.0(vs1.05inSep-theAtmelbiz.TheyexpecttotakeuntilMicrochip6-FebDown1.0%q/qDistributorsinventorywasup3daysExpecttodowellinMar-QExpecttogrowUp12.8%y/y17)aboutJuneof2018forallbizunitstogetq/qhealthySource:Companyresults,calltranscripts16

ValuationMethodandRiskStatementTheupsideriskstothesemiconductorsectorincludestrongerenddemandfromOEMsandtightnessofsupplyduetothefinancialdistressofcompetitors.Downsiderisksincludemacro-economicfactors,over-capacityintimesofpeakingdemandandpooryields.Thesemiconductorsectorishighlycyclicalandvulnerabletosuddenshiftsincustomersentimentwhilemanycompaniesalsohavehighcostbasesmeaningtheycangoloss-makinginthedownturn.Infineonisatop10globalsemiconductorcompanywithexposuretoauto,industrialandchipcardsemiconductorsandhence,inspiteofitsbroadportfolio,thecompanyisexposedtofluctuationsofthesemiconductorcycle.Thecompanyisalsoexposedtooverallautosproductionvolumesandthemixtowardshybridandelectricvehicles(whichhavehighersemiconductorcontent).Therearealsorisksofdisruptionswithnewforthcomingtechnologiessuchassiliconcarbide.InfineonalsohasongoinglitigationrelatedtotheQimondabankruptcythatcouldbeanegative.ThecompanyisalsoexposedtofluctuationsintheUSD:EURexchangeratewithastrongUSDpositiveforthebusiness.WevalueInfineonusingaDCFmethodologywithaWACCof9%andaterminalgrowthrateof2%.Melexis:ThereareanumberofcompanyspecificrisksfacingMelexisincluding1)Customerconcentrationwithitslargestcustomerbeing17%ofsales,2)Significantdependenceonasingleproductfamilywithmagneticsensoraccountingfor43%ofsales,3)RiskofdisruptionifOEMsweretochangetoadifferentmagneticsensortechnology.Moregenerallythebusinessisexposedtofluctuationsinboththesemiconductorinventorycycleandunderlyingdemandforautomotivevehiclesinparticular.Thecompanyisalsoexposedtothepricingandcompetitiveriskinkeymarketsgivenitoperatesinattractivegrowthmarkets.WevalueMelexisusingaDCFbasedonaWACCof9%andgof2%.STMicro:RiskfactorsincludeGDPgrowthrates,continuingweakeningofUS$/EUROexchangerate,technologyproductlifecycles,capacitygrowth,demandandsupplyandutilisationrateswhichcontributetogeneralsemiconductorgrowth.STMicro"sbiggestmediumtermriskiscentredonbeingabletodelivernewimagesensingproductsintosmartphones.OurvaluationforSTMicroisbasedonaDCFmethodologywithaWACCof9%andaterminalgrowthrateof2%.UBSGlobalI/O:Autos/IndustrialSemiconductors13February201817

RequiredDisclosuresThisreporthasbeenpreparedbyUBSLimited,anaffiliateofUBSAG.UBSAG,itssubsidiaries,branchesandaffiliatesarereferredtohereinasUBS.ForinformationonthewaysinwhichUBSmanagesconflictsandmaintainsindependenceofitsresearchproduct;historicalperformanceinformation;andcertainadditionaldisclosuresconcerningUBSresearchrecommendations,pleasevisitwww.ubs.com/disclosures.Thefigurescontainedinperformancechartsrefertothepast;pastperformanceisnotareliableindicatoroffutureresults.Additionalinformationwillbemadeavailableuponrequest.UBSSecuritiesCo.LimitedislicensedtoconductsecuritiesinvestmentconsultancybusinessesbytheChinaSecuritiesRegulatoryCommission.UBSactsormayactasprincipalinthedebtsecurities(orinrelatedderivatives)thatmaybethesubjectofthisreport.Thisrecommendationwasfinalizedon:13February201806:04AMGMT.UBShasdesignatedcertainResearchdepartmentmembersasDerivativesResearchAnalystswherethosedepartmentmemberspublishresearchprincipallyontheanalysisofthepriceormarketforaderivative,andprovideinformationreasonablysufficientuponwhichtobaseadecisiontoenterintoaderivativestransaction.WhereDerivativesResearchAnalystsco-authorresearchreportswithEquityResearchAnalystsorEconomists,theDerivativesResearchAnalystisresponsibleforthederivativesinvestmentviews,forecasts,and/orrecommendations.AnalystCertification:Eachresearchanalystprimarilyresponsibleforthecontentofthisresearchreport,inwholeorinpart,certifiesthatwithrespecttoeachsecurityorissuerthattheanalystcoveredinthisreport:(1)alloftheviewsexpressedaccuratelyreflecthisorherpersonalviewsaboutthosesecuritiesorissuersandwerepreparedinanindependentmanner,includingwithrespecttoUBS,and(2)nopartofhisorhercompensationwas,is,orwillbe,directlyorindirectly,relatedtothespecificrecommendationsorviewsexpressedbythatresearchanalystintheresearchreport.UBSInvestmentResearch:GlobalEquityRatingDefinitions12-MonthRatingDefinitionCoverage1IBServices2BuyFSRis>6%abovetheMRA.46%27%NeutralFSRisbetween-6%and6%oftheMRA.39%24%SellFSRis>6%belowtheMRA.16%13%Short-TermRatingDefinitionCoverage3IBServices4StockpriceexpectedtorisewithinthreemonthsfromthetimeBuy<1%<1%theratingwasassignedbecauseofaspecificcatalystorevent.StockpriceexpectedtofallwithinthreemonthsfromthetimeSell<1%<1%theratingwasassignedbecauseofaspecificcatalystorevent.Source:UBS.Ratingallocationsareasof31December2017.1:Percentageofcompaniesundercoveragegloballywithinthe12-monthratingcategory.2:Percentageofcompanieswithinthe12-monthratingcategoryforwhichinvestmentbanking(IB)serviceswereprovidedwithinthepast12months.3:PercentageofcompaniesundercoveragegloballywithintheShort-Termratingcategory.4:PercentageofcompanieswithintheShort-Termratingcategoryforwhichinvestmentbanking(IB)serviceswereprovidedwithinthepast12months.KEYDEFINITIONS:ForecastStockReturn(FSR)isdefinedasexpectedpercentagepriceappreciationplusgrossdividendyieldoverthenext12months.MarketReturnAssumption(MRA)isdefinedastheone-yearlocalmarketinterestrateplus5%(aproxyfor,andnotaforecastof,theequityriskpremium).UnderReview(UR)StocksmaybeflaggedasURbytheanalyst,indicatingthatthestock"spricetargetand/orratingaresubjecttopossiblechangeinthenearterm,usuallyinresponsetoaneventthatmayaffecttheinvestmentcaseorvaluation.Short-TermRatingsreflecttheexpectednear-term(uptothreemonths)performanceofthestockanddonotreflectanychangeinthefundamentalvieworinvestmentcase.EquityPriceTargetshaveaninvestmenthorizonof12months.EXCEPTIONSANDSPECIALCASES:UKandEuropeanInvestmentFundratingsanddefinitionsare:Buy:Positiveonfactorssuchasstructure,management,performancerecord,discount;Neutral:Neutralonfactorssuchasstructure,management,performancerecord,discount;Sell:Negativeonfactorssuchasstructure,management,performancerecord,discount.CoreBandingExceptions(CBE):Exceptionstothestandard+/-6%bandsmaybegrantedbytheInvestmentReviewCommittee(IRC).FactorsconsideredbytheIRCincludethestock"svolatilityandthecreditspreadoftherespectivecompany"sdebt.Asaresult,stocksdeemedtobeveryhighorlowriskmaybesubjecttohigherorlowerbandsastheyrelatetotherating.Whensuchexceptionsapply,theywillbeidentifiedintheCompanyDisclosurestableintherelevantresearchpiece.UBSGlobalI/O:Autos/IndustrialSemiconductors13February201818

Researchanalystscontributingtothisreportwhoareemployedbyanynon-USaffiliateofUBSSecuritiesLLCarenotregistered/qualifiedasresearchanalystswithFINRA.SuchanalystsmaynotbeassociatedpersonsofUBSSecuritiesLLCandthereforearenotsubjecttotheFINRArestrictionsoncommunicationswithasubjectcompany,publicappearances,andtradingsecuritiesheldbyaresearchanalystaccount.Thenameofeachaffiliateandanalystemployedbythataffiliatecontributingtothisreport,ifany,follows.UBSLimited:DavidMulholland,CFA;Francois-XavierBouvignies;DavidLesne.UBSAGHongKongBranch:NicolasGaudois;BillLu.UBSSecuritiesJapanCo.,Ltd.:KenjiYasui.UBSAG:PatrickHummel,CFA.CompanyDisclosuresCompanyNameReuters12-monthratingShort-termratingPricePricedateInfineonTechnologiesAG7IFXGn.DEBuyN/A€21.8812Feb2018MelexisNVMLXS.BRSellN/A€84.9012Feb2018STMicroelectronics5,7,16STM.PASellN/A€17.4412Feb2018Source:UBS.Allpricesasoflocalmarketclose.Ratingsinthistablearethemostcurrentpublishedratingspriortothisreport.Theymaybemorerecentthanthestockpricingdate5.UBSAG,itsaffiliatesorsubsidiariesexpecttoreceiveorintendtoseekcompensationforinvestmentbankingservicesfromthiscompany/entitywithinthenextthreemonths.7.Withinthepast12months,UBSSecuritiesLLCand/oritsaffiliateshavereceivedcompensationforproductsandservicesotherthaninvestmentbankingservicesfromthiscompany/entity.16.UBSSecuritiesLLCmakesamarketinthesecuritiesand/orADRsofthiscompany.Unlessotherwiseindicated,pleaserefertotheValuationandRisksectionswithinthebodyofthisreport.Foracompletesetofdisclosurestatementsassociatedwiththecompaniesdiscussedinthisreport,includinginformationonvaluationandrisk,pleasecontactUBSSecuritiesLLC,1285AvenueofAmericas,NewYork,NY10019,USA,Attention:InvestmentResearch.InfineonTechnologiesAG(€)PriceTarget(€)StockPrice(€)30.020.010.00.045555556666667777778-1-11r--1-11t--1-11r--1-11t--1-11r--1-11t--1-1cebepnuguccebepnuguccebepnuguccebe-D-F1-A1-J1-A-O1-D-F1-A1-J1-A-O1-D-F1-A1-J1-A-O1-D-F1100001001000010010000100100BuyNeutralUBSGlobalI/O:Autos/IndustrialSemiconductors13February201819

DateStockPrice(€)PriceTarget(€)Rating2014-11-127.619.5Buy2014-11-277.889.4Buy2015-01-309.9811.0Buy2015-05-0610.9812.5Buy2015-07-3110.2112.1Buy2015-08-179.6212.0Buy2015-10-2811.6112.0Neutral2015-11-2713.613.0Neutral2016-02-0112.4414.0Buy2016-02-0311.4813.8Buy2016-08-0313.9113.8Neutral2016-09-2014.9614.7Neutral2016-11-2416.3716.2Neutral2017-01-0616.2217.5Neutral2017-02-0317.7618.0Neutral2017-03-3119.1519.0Neutral2017-06-0720.3121.5Neutral2017-08-0419.2321.0Buy2017-11-0124.4926.0Buy2017-11-1624.5126.5Buy2017-11-2824.3327.0Buy2018-02-0123.1326.0BuySource:UBS;asof12Feb2018MelexisNV(€)PriceTarget(€)StockPrice(€)10080604020045555556666667777778-1-11r--1-11t--1-11r--1-11t--1-11r--1-11t--1-1cebepnuguccebepnuguccebepnuguccebe-D-F1-A1-J1-A-O1-D-F1-A1-J1-A-O1-D-F1-A1-J1-A-O1-D-F1100001001000010010000100100NeutralSellDateStockPrice(€)PriceTarget(€)Rating2014-11-1237.0235.0Neutral2014-12-1035.1337.0Neutral2015-02-0545.0144.0Neutral2015-04-2456.8456.0Neutral2015-07-3050.651.0Neutral2015-10-2242.6543.0Neutral2016-02-1541.7639.0Sell2016-09-2060.6542.0Sell2017-01-0664.4148.0Sell2017-02-1378.8352.0Sell2017-08-0278.3953.0Sell2017-10-2787.3755.0SellSource:UBS;asof12Feb2018UBSGlobalI/O:Autos/IndustrialSemiconductors13February201820

STMicroelectronics(€)PriceTarget(€)StockPrice(€)25.020.015.010.05.00.045555556666667777778-1-11r--1-11t--1-11r--1-11t--1-11r--1-11t--1-1cebepnuguccebepnuguccebepnuguccebe-D-F1-A-J1-A-O1-D-F1-A-J1-A-O1-D-F1-A-J1-A-O1-D-F1100100100100100100100100100100NeutralSellNoRatingDateStockPrice(€)PriceTarget(€)Rating2014-11-125.515.0Neutral2014-12-106.095.5Sell2015-01-297.396.7Sell2015-05-017.126.0Sell2015-07-247.155.7Sell2016-01-286.15.6Sell2016-02-174.98-NoRating2016-02-185.244.7Neutral2016-05-044.855.0Neutral2016-07-286.446.2Neutral2016-09-207.136.7Neutral2016-10-318.698.1Neutral2017-01-0610.2110.0Neutral2017-01-2712.512.0Neutral2017-04-1114.0514.3Neutral2017-04-2814.8514.6Neutral2017-05-1215.1714.8Neutral2017-06-0715.0515.0Neutral2017-08-0414.5613.0Sell2017-10-2719.9215.0Sell2017-11-2820.2815.5SellSource:UBS;asof12Feb2018UBSGlobalI/O:Autos/IndustrialSemiconductors13February201821

GlobalDisclaimerThisdocumenthasbeenpreparedbyUBSLimited,anaffiliateofUBSAG.UBSAG,itssubsidiaries,branchesandaffiliatesarereferredtohereinasUBS.GlobalResearchisprovidedtoourclientsthroughUBSNeo,incertaininstances,UBS.comandanyothersystem,ordistributionmethodspecificallyidentifiedinoneormorecommunicationsdistributedthroughUBSNeoorUBS.comasanapprovedmeansfordistributingGlobalResearch(eacha"System").ItmayalsobemadeavailablethroughthirdpartyvendorsanddistributedbyUBSand/orthirdpartiesviae-mailoralternativeelectronicmeans.ThelevelandtypesofservicesprovidedbyGlobalResearchtoaclientmayvarydependinguponvariousfactorssuchasaclient"sindividualpreferencesastothefrequencyandmannerofreceivingcommunications,aclient"sriskprofileandinvestmentfocusandperspective(e.g.,marketwide,sectorspecific,long-term,short-term,etc.),thesizeandscopeoftheoverallclientrelationshipwithUBSandlegalandregulatoryconstraints.AllGlobalResearchisavailableonUBSNeo.PleasecontactyourUBSsalesrepresentativeifyouwishtodiscussyouraccesstoUBSNeo.WhenyoureceiveGlobalResearchthroughaSystem,youraccessand/oruseofsuchGlobalResearchissubjecttothisGlobalResearchDisclaimerandtothetermsofusegoverningtheapplicableSystem.WhenyoureceiveGlobalResearchviaathirdpartyvendor,e-mailorotherelectronicmeans,youagreethatuseshallbesubjecttothisGlobalResearchDisclaimer,whereapplicabletheUBSInvestmentBanktermsofbusiness(https://www.ubs.com/global/en/investment-bank/regulatory.html)andtoUBS"sTermsofUse/Disclaimer(http://www.ubs.com/global/en/legalinfo2/disclaimer.html).Inaddition,youconsenttoUBSprocessingyourpersonaldataandusingcookiesinaccordancewithourPrivacyStatement(http://www.ubs.com/global/en/legalinfo2/privacy.html)andcookienotice(http://www.ubs.com/global/en/homepage/cookies/cookie-management.html).IfyoureceiveGlobalResearch,whetherthroughaSystemorbyanyothermeans,youagreethatyoushallnotcopy,revise,amend,createaderivativework,providetoanythirdparty,orinanywaycommerciallyexploitanyUBSresearchprovidedviaGlobalResearchorotherwise,andthatyoushallnotextractdatafromanyresearchorestimatesprovidedtoyouviaGlobalResearchorotherwise,withoutthepriorwrittenconsentofUBS.Thisdocumentisfordistributiononlyasmaybepermittedbylaw.Itisnotdirectedto,orintendedfordistributiontooruseby,anypersonorentitywhoisacitizenorresidentoforlocatedinanylocality,state,countryorotherjurisdictionwheresuchdistribution,publication,availabilityorusewouldbecontrarytolaworregulationorwouldsubjectUBStoanyregistrationorlicensingrequirementwithinsuchjurisdiction.Thisdocumentisageneralcommunicationandiseducationalinnature;itisnotanadvertisementnorisitasolicitationoranoffertobuyorsellanyfinancialinstrumentsortoparticipateinanyparticulartradingstrategy.Nothinginthisdocumentconstitutesarepresentationthatanyinvestmentstrategyorrecommendationissuitableorappropriatetoaninvestor’sindividualcircumstancesorotherwiseconstitutesapersonalrecommendation.Byprovidingthisdocument,noneofUBSoritsrepresentativeshasanyresponsibilityorauthoritytoprovideorhaveprovidedinvestmentadviceinafiduciarycapacityorotherwise.Investmentsinvolverisks,andinvestorsshouldexerciseprudenceandtheirownjudgmentinmakingtheirinvestmentdecisions.NoneofUBSoritsrepresentativesissuggestingthattherecipientoranyotherpersontakeaspecificcourseofactionoranyactionatall.Byreceivingthisdocument,therecipientacknowledgesandagreeswiththeintendedpurposedescribedaboveandfurtherdisclaimsanyexpectationorbeliefthattheinformationconstitutesinvestmentadvicetotherecipientorotherwisepurportstomeettheinvestmentobjectivesoftherecipient.Thefinancialinstrumentsdescribedinthedocumentmaynotbeeligibleforsaleinalljurisdictionsortocertaincategoriesofinvestors.Options,derivativeproductsandfuturesarenotsuitableforallinvestors,andtradingintheseinstrumentsisconsideredrisky.Mortgageandasset-backedsecuritiesmayinvolveahighdegreeofriskandmaybehighlyvolatileinresponsetofluctuationsininterestratesorothermarketconditions.Foreigncurrencyratesofexchangemayadverselyaffectthevalue,priceorincomeofanysecurityorrelatedinstrumentreferredtointhedocument.Forinvestmentadvice,tradeexecutionorotherenquiries,clientsshouldcontacttheirlocalsalesrepresentative.Thevalueofanyinvestmentorincomemaygodownaswellasup,andinvestorsmaynotgetbackthefull(orany)amountinvested.Pastperformanceisnotnecessarilyaguidetofutureperformance.NeitherUBSnoranyofitsdirectors,employeesoragentsacceptsanyliabilityforanyloss(includinginvestmentloss)ordamagearisingoutoftheuseofalloranyoftheInformation.Priortomakinganyinvestmentorfinancialdecisions,anyrecipientofthisdocumentortheinformationshouldseekindividualizedadvicefromhisorherpersonalfinancial,legal,taxandotherprofessionaladvisorsthattakesintoaccountalltheparticularfactsandcircumstancesofhisorherinvestmentobjectives.Anypricesstatedinthisdocumentareforinformationpurposesonlyanddonotrepresentvaluationsforindividualsecuritiesorotherfinancialinstruments.Thereisnorepresentationthatanytransactioncanorcouldhavebeeneffectedatthoseprices,andanypricesdonotnecessarilyreflectUBS"sinternalbooksandrecordsortheoreticalmodel-basedvaluationsandmaybebasedoncertainassumptions.DifferentassumptionsbyUBSoranyothersourcemayyieldsubstantiallydifferentresults.Norepresentationorwarranty,eitherexpressedorimplied,isprovidedinrelationtotheaccuracy,completenessorreliabilityoftheinformationcontainedinanymaterialstowhichthisdocumentrelates(the"Information"),exceptwithrespecttoInformationconcerningUBS.TheInformationisnotintendedtobeacompletestatementorsummaryofthesecurities,marketsordevelopmentsreferredtointhedocument.UBSdoesnotundertaketoupdateorkeepcurrenttheInformation.Anyopinionsexpressedinthisdocumentmaychangewithoutnoticeandmaydifferorbecontrarytoopinionsexpressedbyotherbusinessareasorgroups,personnelorotherrepresentativeofUBS.AnystatementscontainedinthisreportattributedtoathirdpartyrepresentUBS"sinterpretationofthedata,informationand/oropinionsprovidedbythatthirdpartyeitherpubliclyorthroughasubscriptionservice,andsuchuseandinterpretationhavenotbeenreviewedbythethirdparty.InnocircumstancesmaythisdocumentoranyoftheInformation(includinganyforecast,value,indexorothercalculatedamount("Values"))beusedforanyofthefollowingpurposes:(i)valuationoraccountingpurposes;(ii)todeterminetheamountsdueorpayable,thepriceorthevalueofanyfinancialinstrumentorfinancialcontract;or(iii)tomeasuretheperformanceofanyfinancialinstrumentincluding,withoutlimitation,forthepurposeoftrackingthereturnorperformanceofanyValueorofdefiningtheassetallocationofportfolioorofcomputingperformancefees.ByreceivingthisdocumentandtheInformationyouwillbedeemedtorepresentandwarranttoUBSthatyouwillnotusethisdocumentoranyoftheInformationforanyoftheabovepurposesorotherwiserelyuponthisdocumentoranyoftheInformation.UBShaspoliciesandprocedures,whichinclude,withoutlimitation,independencepoliciesandpermanentinformationbarriers,thatareintended,anduponwhichUBSrelies,tomanagepotentialconflictsofinterestandcontroltheflowofinformationwithindivisionsofUBSandamongitssubsidiaries,branchesandaffiliates.ForfurtherinformationonthewaysinwhichUBSmanagesconflictsandmaintainsindependenceofitsresearchproducts,historicalperformanceinformationandcertainadditionaldisclosuresconcerningUBSresearchrecommendations,pleasevisitwww.ubs.com/disclosures.Researchwillinitiate,updateandceasecoveragesolelyatthediscretionofUBSResearchManagement,whichwillalsohavesolediscretiononthetimingandfrequencyofanypublishedresearchproduct.Theanalysiscontainedinthisdocumentisbasedonnumerousassumptions.Allmaterialinformationinrelationtopublishedresearchreports,suchasvaluationmethodology,riskstatements,underlyingassumptions(includingsensitivityanalysisofthoseassumptions),ratingshistoryetc.asrequiredbytheMarketAbuseRegulation,canbefoundonUBSNeo.Differentassumptionscouldresultinmateriallydifferentresults.Theanalyst(s)responsibleforthepreparationofthisdocumentmayinteractwithtradingdeskpersonnel,salespersonnelandotherpartiesforthepurposeofgathering,applyingandinterpretingmarketinformation.UBSreliesoninformationbarrierstocontroltheflowofinformationcontainedinoneormoreareaswithinUBSintootherareas,units,groupsoraffiliatesofUBS.Thecompensationoftheanalystwhopreparedthisdocumentisdeterminedexclusivelybyresearchmanagementandseniormanagement(notincludinginvestmentbanking).Analystcompensationisnotbasedoninvestmentbankingrevenues;however,compensationmayrelatetotherevenuesofUBSand/oritsdivisionsasawhole,ofwhichinvestmentbanking,salesandtradingareapart,andUBS"ssubsidiaries,branchesandaffiliatesasawhole.ForfinancialinstrumentsadmittedtotradingonanEUregulatedmarket:UBSAG,itsaffiliatesorsubsidiaries(excludingUBSSecuritiesLLC)actsasamarketmakerorliquidityprovider(inaccordancewiththeinterpretationofthesetermsintheUK)inthefinancialinstrumentsoftheissuersavethatwheretheactivityofliquidityprovideriscarriedoutinaccordancewiththedefinitiongiventoitbythelawsandregulationsofanyotherEUjurisdictions,suchinformationisseparatelydisclosedinthisdocument.Forfinancialinstrumentsadmittedtotradingonanon-EUregulatedmarket:UBSmayactasamarketmakersavethatwherethisactivityiscarriedoutintheUSinaccordancewiththedefinitiongiventoitbytherelevantlawsandregulations,suchactivitywillbespecificallydisclosedinthisdocument.UBSmayhaveissuedawarrantthevalueofwhichisbasedononeormoreofthefinancialinstrumentsreferredtointhedocument.UBSanditsaffiliatesandemployeesmayhavelongorshortpositions,tradeasprincipalandbuyandsellininstrumentsorderivativesidentifiedherein;suchtransactionsorpositionsmaybeinconsistentwiththeopinionsexpressedinthisdocument.UBSGlobalI/O:Autos/IndustrialSemiconductors13February201822

UnitedKingdomandtherestofEurope:Exceptasotherwisespecifiedherein,thismaterialisdistributedbyUBSLimitedtopersonswhoareeligiblecounterpartiesorprofessionalclients.UBSLimitedisauthorisedbythePrudentialRegulationAuthorityandregulatedbytheFinancialConductAuthorityandthePrudentialRegulationAuthority.France:PreparedbyUBSLimitedanddistributedbyUBSLimitedandUBSSecuritiesFranceS.A.UBSSecuritiesFranceS.A.isregulatedbytheACPR(AutoritédeContrôlePrudentieletdeRésolution)andtheAutoritédesMarchésFinanciers(AMF).WhereananalystofUBSSecuritiesFranceS.A.hascontributedtothisdocument,thedocumentisalsodeemedtohavebeenpreparedbyUBSSecuritiesFranceS.A.Germany:PreparedbyUBSLimitedanddistributedbyUBSLimitedandUBSEuropeSE.UBSEuropeSEisregulatedbytheBundesanstaltfurFinanzdienstleistungsaufsicht(BaFin).Spain:PreparedbyUBSLimitedanddistributedbyUBSLimitedandUBSSecuritiesEspañaSV,SA.UBSSecuritiesEspañaSV,SAisregulatedbytheComisiónNacionaldelMercadodeValores(CNMV).Turkey:DistributedbyUBSLimited.Noinformationinthisdocumentisprovidedforthepurposeofoffering,marketingandsalebyanymeansofanycapitalmarketinstrumentsandservicesintheRepublicofTurkey.Therefore,thisdocumentmaynotbeconsideredasanoffermadeortobemadetoresidentsoftheRepublicofTurkey.UBSLimitedisnotlicensedbytheTurkishCapitalMarketBoardundertheprovisionsoftheCapitalMarketLaw(LawNo.6362).Accordingly,neitherthisdocumentnoranyotherofferingmaterialrelatedtotheinstruments/servicesmaybeutilizedinconnectionwithprovidinganycapitalmarketservicestopersonswithintheRepublicofTurkeywithoutthepriorapprovaloftheCapitalMarketBoard.However,accordingtoarticle15(d)(ii)oftheDecreeNo.32,thereisnorestrictiononthepurchaseorsaleofthesecuritiesabroadbyresidentsoftheRepublicofTurkey.Poland:DistributedbyUBSLimited(spolkazograniczonaodpowiedzialnoscia)OddzialwPolsceregulatedbythePolishFinancialSupervisionAuthority.WhereananalystofUBSLimited(spolkazograniczonaodpowiedzialnoscia)OddzialwPolscehascontributedtothisdocument,thedocumentisalsodeemedtohavebeenpreparedbyUBSLimited(spolkazograniczonaodpowiedzialnoscia)OddzialwPolsce.Russia:PreparedanddistributedbyUBSBank(OOO).Switzerland:DistributedbyUBSAGtopersonswhoareinstitutionalinvestorsonly.UBSAGisregulatedbytheSwissFinancialMarketSupervisoryAuthority(FINMA).Italy:PreparedbyUBSLimitedanddistributedbyUBSLimitedandUBSLimited,ItalyBranch.WhereananalystofUBSLimited,ItalyBranchhascontributedtothisdocument,thedocumentisalsodeemedtohavebeenpreparedbyUBSLimited,ItalyBranch.SouthAfrica:DistributedbyUBSSouthAfrica(Pty)Limited(RegistrationNo.1995/011140/07),anauthoriseduseroftheJSEandanauthorisedFinancialServicesProvider(FSP7328).Israel:ThismaterialisdistributedbyUBSLimited.UBSLimitedisauthorisedbythePrudentialRegulationAuthorityandregulatedbytheFinancialConductAuthorityandthePrudentialRegulationAuthority.UBSSecuritiesIsraelLtdisalicensedInvestmentMarketerthatissupervisedbytheIsraelSecuritiesAuthority(ISA).UBSLimitedanditsaffiliatesincorporatedoutsideIsraelarenotlicensedundertheIsraeliAdvisoryLaw.UBSLimitedisnotcoveredbyinsuranceasrequiredfromalicenseeundertheIsraeliAdvisoryLaw.UBSmayengageamongothersinissuanceofFinancialAssetsorindistributionofFinancialAssetsofotherissuersforfeesorotherbenefits.UBSLimitedanditsaffiliatesmayprefervariousFinancialAssetstowhichtheyhaveormayhaveAffiliation(assuchtermisdefinedundertheIsraeliAdvisoryLaw).NothinginthisMaterialshouldbeconsideredasinvestmentadviceundertheIsraeliAdvisoryLaw.ThisMaterialisbeingissuedonlytoand/orisdirectedonlyatpersonswhoareEligibleClientswithinthemeaningoftheIsraeliAdvisoryLaw,andthismaterialmustnotbereliedonoracteduponbyanyotherpersons.SaudiArabia:ThisdocumenthasbeenissuedbyUBSAG(and/oranyofitssubsidiaries,branchesoraffiliates),apubliccompanylimitedbyshares,incorporatedinSwitzerlandwithitsregisteredofficesatAeschenvorstadt1,CH-4051BaselandBahnhofstrasse45,CH-8001Zurich.ThispublicationhasbeenapprovedbyUBSSaudiArabia(asubsidiaryofUBSAG),aSaudiclosedjointstockcompanyincorporatedintheKingdomofSaudiArabiaundercommercialregisternumber1010257812havingitsregisteredofficeatTatweerTowers,P.O.Box75724,Riyadh11588,KingdomofSaudiArabia.UBSSaudiArabiaisauthorizedandregulatedbytheCapitalMarketAuthoritytoconductsecuritiesbusinessunderlicensenumber08113-37.UAE/Dubai:TheinformationdistributedbyUBSAGDubaiBranchisonlyintendedforProfessionalClientsand/orMarketCounterparties,asclassifiedundertheDFSArulebook.Nootherpersonshouldactuponthismaterial/communication.TheinformationisnotforfurtherdistributionwithintheUnitedArabEmirates.UBSAGDubaiBranchisregulatedbytheDFSAintheDIFC.UBSisnotlicensedtoprovidebankingservicesintheUAEbytheCentralBankoftheUAE,norisitlicensedbytheUAESecuritiesandCommoditiesAuthority.UnitedStates:DistributedtoUSpersonsbyeitherUBSSecuritiesLLCorbyUBSFinancialServicesInc.,subsidiariesofUBSAG;orbyagroup,subsidiaryoraffiliateofUBSAGthatisnotregisteredasaUSbroker-dealer(a‘non-USaffiliate’)tomajorUSinstitutionalinvestorsonly.UBSSecuritiesLLCorUBSFinancialServicesInc.acceptsresponsibilityforthecontentofadocumentpreparedbyanothernon-USaffiliatewhendistributedtoUSpersonsbyUBSSecuritiesLLCorUBSFinancialServicesInc.AlltransactionsbyaUSpersoninthesecuritiesmentionedinthisdocumentmustbeeffectedthroughUBSSecuritiesLLCorUBSFinancialServicesInc.,andnotthroughanon-USaffiliate.UBSSecuritiesLLCisnotactingasamunicipaladvisortoanymunicipalentityorobligatedpersonwithinthemeaningofSection15BoftheSecuritiesExchangeAct(the"MunicipalAdvisorRule"),andtheopinionsorviewscontainedhereinarenotintendedtobe,anddonotconstitute,advicewithinthemeaningoftheMunicipalAdvisorRule.Canada:DistributedbyUBSSecuritiesCanadaInc.,aregisteredinvestmentdealerinCanadaandaMember-CanadianInvestorProtectionFund,orbyanotheraffiliateofUBSAGthatisregisteredtoconductbusinessinCanadaorisotherwiseexemptfromregistration.Mexico:ThisreporthasbeendistributedandpreparedbyUBSCasadeBolsa,S.A.deC.V.,UBSGrupoFinanciero,anentitythatispartofUBSGrupoFinanciero,S.A.deC.V.andisasubsidiaryofUBSAG.Thisdocumentisintendedfordistributiontoinstitutionalorsophisticatedinvestorsonly.Researchreportsonlyreflecttheviewsoftheanalystsresponsibleforthereports.AnalystsdonotreceiveanycompensationfrompersonsorentitiesdifferentfromUBSCasadeBolsa,S.A.deC.V.,UBSGrupoFinanciero,ordifferentfromentitiesbelongingtothesamefinancialgrouporbusinessgroupofsuch.ForSpanishtranslationsofapplicabledisclosures,pleasegotowww.ubs.com/disclosures.Brazil:Exceptasotherwisespecifiedherein,thismaterialispreparedbyUBSBrasilCCTVMS.A.topersonswhoareeligibleinvestorsresidinginBrazil,whichareconsideredtobe:(i)financialinstitutions,(ii)insurancefirmsandinvestmentcapitalcompanies,(iii)supplementarypensionentities,(iv)entitiesthatholdfinancialinvestmentshigherthanR$300,000.00andthatconfirmthestatusofqualifiedinvestorsinwritten,(v)investmentfunds,(vi)securitiesportfoliomanagersandsecuritiesconsultantsdulyauthorizedbyComissãodeValoresMobiliários(CVM),regardingtheirowninvestments,and(vii)socialsecuritysystemscreatedbytheFederalGovernment,States,andMunicipalities.HongKong:DistributedbyUBSSecuritiesAsiaLimitedand/orUBSAG,HongKongBranch.Pleasecontactlocallicensed/registeredrepresentativesofUBSSecuritiesAsiaLimitedand/orUBSAG,HongKongBranchinrespectofanymattersarisingfrom,orinconnectionwith,theanalysisordocument.Singapore:DistributedbyUBSSecuritiesPte.Ltd.[MCI(P)008/09/2017andCo.Reg.No.:198500648C]orUBSAG,SingaporeBranch.PleasecontactUBSSecuritiesPte.Ltd.,anexemptfinancialadviserundertheSingaporeFinancialAdvisersAct(Cap.110);orUBSAG,SingaporeBranch,anexemptfinancialadviserundertheSingaporeFinancialAdvisersAct(Cap.110)andawholesalebanklicensedundertheSingaporeBankingAct(Cap.19)regulatedbytheMonetaryAuthorityofSingapore,inrespectofanymattersarisingfrom,orinconnectionwith,theanalysisordocument.TherecipientsofthisdocumentrepresentandwarrantthattheyareaccreditedandinstitutionalinvestorsasdefinedintheSecuritiesandFuturesAct(Cap.289).Japan:DistributedbyUBSSecuritiesJapanCo.,Ltd.toprofessionalinvestors(exceptasotherwisepermitted).WherethisdocumenthasbeenpreparedbyUBSSecuritiesJapanCo.,Ltd.,UBSSecuritiesJapanCo.,Ltd.istheauthor,publisheranddistributorofthedocument.DistributedbyUBSAG,TokyoBranchtoProfessionalInvestors(exceptasotherwisepermitted)inrelationtoforeignexchangeandotherbankingbusinesseswhenrelevant.Australia:ClientsofUBSAG:DistributedbyUBSAG(ABN47088129613andholderofAustralianFinancialServicesLicenseNo.231087).ClientsofUBSSecuritiesAustraliaLtd:DistributedbyUBSSecuritiesAustraliaLtd(ABN62008586481andholderofAustralianFinancialServicesLicenseNo.231098).ThisDocumentcontainsgeneralinformationand/orgeneraladviceonlyanddoesnotconstitutepersonalfinancialproductadvice.Assuch,theInformationinthisdocumenthasbeenpreparedwithouttakingintoaccountanyinvestor’sobjectives,financialsituationorneeds,andinvestorsshould,beforeactingontheInformation,considertheappropriatenessoftheInformation,havingregardtotheirobjectives,financialsituationandneeds.IftheInformationcontainedinthisdocumentrelatestotheacquisition,orpotentialacquisitionofaparticularfinancialproductbya‘Retail’clientasdefinedbysection761GoftheCorporationsAct2001whereaProductDisclosureStatementwouldberequired,theretailclientshouldobtainandconsidertheProductDisclosureStatementrelatingtotheproductbeforemakinganydecisionaboutwhethertoacquiretheproduct.TheUBSSecuritiesAustraliaLimitedFinancialServicesGuideisavailableat:www.ubs.com/ecs-research-fsg.NewZealand:DistributedbyUBSNewZealandLtd.UBSNewZealandLtdisnotaregisteredbankinNewZealand.YouarebeingprovidedwiththisUBSpublicationormaterialbecauseyouhaveindicatedtoUBSthatyouarea“wholesaleclient”withinthemeaningofsection5CoftheFinancialAdvisersAct2008ofNewZealand(PermittedClient).ThispublicationormaterialisnotintendedforclientswhoarenotPermittedClients(non-permittedClients).Ifyouareanon-permittedClientyoumustnotrelyonthispublicationormaterial.Ifdespitethiswarningyouneverthelessrelyonthispublicationormaterial,youhereby(i)acknowledgethatyoumaynotrelyonthecontentofthispublicationormaterialandthatanyrecommendationsoropinionsinsuchthispublicationormaterialarenotmadeorprovidedtoyou,and(ii)tothemaximumextentpermittedbylaw(a)indemnifyUBSanditsassociatesorrelatedentities(andtheirrespectiveDirectors,officers,agentsandAdvisors)(eacha‘RelevantPerson’)foranyloss,damage,liabilityorclaimanyofthemmayincurorsufferasaresultof,orinconnectionwith,yourunauthorisedrelianceonthispublicationormaterialand(b)waiveanyrightsorremediesyoumayhaveagainstanyRelevantPersonfor(orinrespectof)anyloss,damage,liabilityorclaimyoumayincurorsufferasaresultof,orinconnectionwith,yourunauthorisedrelianceonthispublicationormaterial.Korea:DistributedinKoreabyUBSSecuritiesPte.Ltd.,SeoulBranch.ThisdocumentmayhavebeeneditedorcontributedtofromtimetotimebyaffiliatesofUBSSecuritiesPte.Ltd.,SeoulBranch.Thismaterialisintendedforprofessional/institutionalclientsonlyandnotfordistributiontoanyretailclients.Malaysia:ThismaterialisauthorizedtobedistributedinMalaysiabyUBSSecuritiesMalaysiaSdn.Bhd(CapitalMarketsServicesLicenseNo.:CMSL/A0063/2007).Thismaterialisintendedforprofessional/institutionalclientsonlyandnotfordistributiontoanyretailclients.India:DistributedbyUBSSecuritiesIndiaPrivateLtd.(CorporateIdentityNumberU67120MH1996PTC097299)2/F,2NorthAvenue,MakerMaxity,BandraKurlaComplex,Bandra(East),Mumbai(India)400051.Phone:+912261556000.ItprovidesbrokerageservicesbearingSEBIRegistrationNumbers:NSE(CapitalMarketSegment):INB230951431,NSE(F&OSegment)INF230951431,NSE(CurrencyDerivativesSegment)INE230951431,BSE(CapitalMarketSegment)INB010951437;merchantbankingservicesbearingSEBIRegistrationNumber:INM000010809andResearchAnalystservicesbearingSEBIRegistrationNumber:INH000001204.UBSAG,itsaffiliatesorsubsidiariesmayhavedebtholdingsorpositionsinthesubjectIndiancompany/companies.Withinthepast12months,UBSAG,itsaffiliatesorsubsidiariesmayhavereceivedcompensationfornon-investmentbankingsecurities-relatedservicesand/ornon-securitiesservicesfromthesubjectIndiancompany/companies.Thesubjectcompany/companiesmayhavebeenaclient/clientsofUBSAG,itsaffiliatesorsubsidiariesduringthe12monthsprecedingthedateofdistributionoftheresearchreportwithrespecttoinvestmentbankingand/ornon-investmentbankingsecurities-relatedservicesand/ornon-securitiesservices.Withregardtoinformationonassociates,pleaserefertotheAnnualReportat:UBSGlobalI/O:Autos/IndustrialSemiconductors13February201823

http://www.ubs.com/global/en/about_ubs/investor_relations/annualreporting.htmlTaiwan:DistributedbyUBSSecuritiesPte.Ltd.,TaipeiBranchwhichisregulatedbytheTaiwanSecuritiesandFuturesBureau.ThedisclosurescontainedinresearchdocumentsproducedbyUBSLimitedshallbegovernedbyandconstruedinaccordancewithEnglishlaw.UBSspecificallyprohibitstheredistributionofthisdocumentinwholeorinpartwithoutthewrittenpermissionofUBSandinanyeventUBSacceptsnoliabilitywhatsoeverforanyredistributionofthisdocumentoritscontentsortheactionsofthirdpartiesinthisrespect.Imagesmaydepictobjectsorelementsthatareprotectedbythirdpartycopyright,trademarksandotherintellectualpropertyrights.©UBS2018.ThekeysymbolandUBSareamongtheregisteredandunregisteredtrademarksofUBS.Allrightsreserved.UBSGlobalI/O:Autos/IndustrialSemiconductors13February201824'

您可能关注的文档

- 汇丰银行-亚洲-半导体行业-智能手机越来越智能化

- 半导体行业1月观点:新型计算架构浪潮推动,中国半导体产业弯道超车机会来临

- 瑞信-美股-半导体行业-10月sia分析报告

- 泛半导体行业专题报告:半导体投资时钟

- 瑞信-亚洲-半导体行业-瑞信技术峰会2017:第一天要点

- 半导体行业:中国崛起正当时

- 泛半导体行业专题报告:“泛半导体”星汉灿烂,“核心资产”若出其里

- 半导体行业:十大里程碑看2018中国半导体!

- 电子行业:大基金二期启航,半导体行业向好

- 半导体行业深度研究:人工智能芯片,新架构改变世界

- 半导体行业2017年9月策略:人工智能芯片发布引发资本市场关注,行业基本面收益景气度持续

- 电子行业18年度投资策略报告:led行业继续高增长,半导体行业谨慎乐观

- 半导体行业专题研究:再论半导体设备企业的需求拉动与成长路径

- 电子行业:换机潮晚至不改半导体行业景气