- 160.39 KB

- 2022-04-29 14:03:04 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

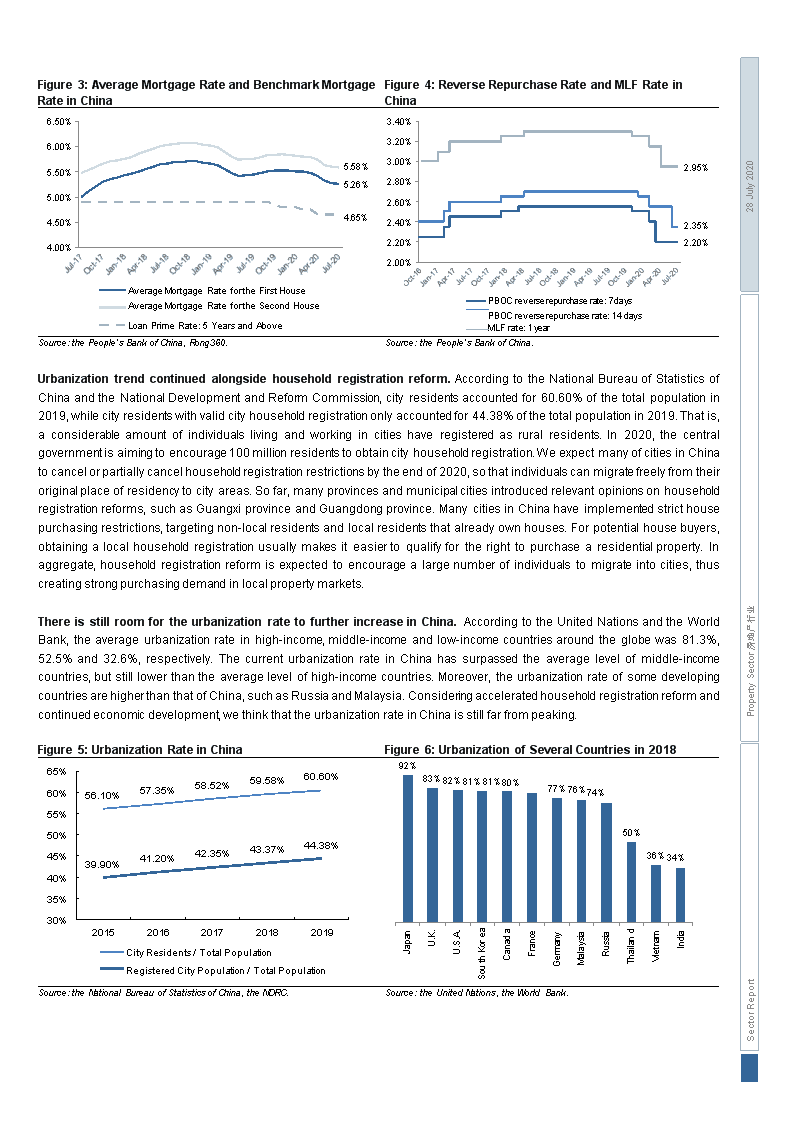

'PropertyDevelopmentIndustryinChina28July2020PropertysalesperformancehitbottominFeb.2020;salesrecoveryisexpectedtocontinuein2H2020.Inthefirstfewmonthsof2020,theCOVID-19pandemiccastashadowovertheeconomyinChina,withtherealestatemarketinChinaexperiencingshort-termdownsidepressure.SincelateJan.2020,manylocalgovernmentsinChinasuspendedpropertysalesactivitiesandpostponedconstructioncommencementofmanypropertyprojectsduetotheCOVID-19pandemic.Asaresult,commodityhousingsalesamountinJan.-Feb.2020declinedby35.9%YoY.SinceMar.2020,wehaveseencustomervisitsandpropertysalesresumingtoaconsiderabledegreeweekbyweek,especiallyinhigher-tiercitiesaroundkeyurbanclusterssuchastheYangtzeRiverDeltaandtheGreaterBayArea.During1H2020,commodityhousingsalesamountdroppedby5.4%YoY,indicatingstrongsalesrecovery.Inthemedium-to-longterm,webelievetheimpactislikelytoeaseasthepandemichasbeeneffectivelycontrolledinChinaasaresultofstrictmeasuresimplementedbytheChinesegovernmenttocontainthespreadofCOVID-19,aswellasincentivemeasurestakentoboosttheeconomy.Figure1:CumulativeHouseSalesAmountinChinaFigure2:CumulativeHouseSalesGFAinChina18,000RMBbn16,00014,00012,00010,0008,0006,0004,0002,0000AmountSoldofCommodityHouses(LHS)AmountSoldofResidentialHouses(LHS)AmountSoldYTDYoYofCommodityHouses(RHS)AmountSoldYTDYoYofResidentialHouses(RHS)50%40%30%20%10%0%-10%-20%-30%-40%2,000Mnsq.m.1,7501,5001,2501,0007505002500GFASoldofCommodityHouses(LHS)GFASoldofResidentialHouses(LHS)GFASoldofCommodityHousesYTDYoY(RHS)GFASoldofResidentialHousesYTDYoY(RHS)40%30%20%10%0%-10%-20%-30%-40%-50%Source:theNationalBureauofStatisticsofChina,GuotaiJunanInternational.Source:theNationalBureauofStatisticsofChina,GuotaiJunanInternational.PropertySector房地产行业Propertyindustrypoliciesareexpectedtoremainstable.The2020GovernmentWorkReportmentionedthat"Housesareforlivinginandnotforspeculativeinvestment"(房住不炒)and"Targetedpoliciesshouldbeimplementedonacity-by-citybasis"(因城施策).Thatis,theChinesegovernmentwillnotusethereal-estateindustryasatoolforshort-termstimulationoftheeconomy.Sincethebeginningof2020,manycentral-levelmeetingsemphasizedthatoneofthemostsignificanttasksin2020willbeensuringstabilityinemployment,financialoperations,foreigntrade,foreigninvestment,domesticinvestment,andexpectations(六稳),aswellasensuringsecurityinemployment,basiclivingneeds,operationsofmarketentities,foodandenergysecurity,stableindustrialandsupplychains,andthenormalfunctioningofprimary-levelgovernments(六保).ThepropertysectorstillplaysanimportantroleintheChineseeconomyandisrelatedtothedevelopmentofmanyotherindustriessuchasmaterials,steel,cement,furniture,homeappliances,etc.Webelievethatthereisnomoreroomforfurthertighteningofregulationsandpoliciesinthepropertysector.Thepurposeoftargetedpolicieswillbemaintainedaspromotingthesteadyandsounddevelopmentofthepropertysector.ThemonetaryenvironmentinChinaeasedin1H2020,benefitingbothhousebuyersandpropertydevelopers.In1H2020,thePeople’sBankofChinaperformedmultipleroundsofRRRcuts.AsattheendofJun.2020,theaverageRRRlevelhasbeenreducedto9.4%from14.9%inthebeginningof2018.During1H2020,the1-yearMLFratedecreasedfrom3.25%to2.95%,whilethe5-yearLPRdeclinedfrom4.80%to4.65%.SinceOct.2019,commercialbanksinChinastartedtoapplythe5-yearLPRasabenchmarkforthepersonalmortgageinterestrate.Theaveragelevelofmortgagerateforfirstandsecondhouseshasbeendecreasingsincethebeginningof2020.Declininginterestlevelalsoreducedfinancecostsofcorporateloansandfixed-incomeinstrumentsinChina,thusbenefitingpropertydevelopers.SectorReportWeexpectmonetaryenvironmenttoremainrelativelyloosein2H2020.InMar.2020,theUSFederalReservecuttheFederalFundsRateto0%-0.25%andplannedtorestartlarge-scalequantativeeasing(QE).WeareoftheviewthattheChinesegovernmentwillcontinuetoeasethemonetaryenvironmentin2020butwillbelessradicalcomparedtotheUS.Inaggregate,weexpectreducedinterestratestostimulatetherealeconomyandbenefitbothhousebuyersandthepropertysectorin2H2020.

Figure3:AverageMortgageRateandBenchmarkMortgageRateinChinaFigure4:ReverseRepurchaseRateandMLFRateinChina6.50%6.00%5.50%5.00%4.50%4.00%5.58%5.26%4.65%3.40%3.20%3.00%2.80%2.60%2.40%2.20%2.00%2.95%28July20202.35%2.20%AverageMortgageRatefortheFirstHouseAverageMortgageRatefortheSecondHousePBOCreverserepurchaserate:7daysPBOCreverserepurchaserate:14daysLoanPrimeRate:5YearsandAboveMLFrate:1yearSource:thePeople’sBankofChina,Rong360.Source:thePeople’sBankofChina.PropertySector房地产行业Urbanizationtrendcontinuedalongsidehouseholdregistrationreform.AccordingtotheNationalBureauofStatisticsofChinaandtheNationalDevelopmentandReformCommission,cityresidentsaccountedfor60.60%ofthetotalpopulationin2019,whilecityresidentswithvalidcityhouseholdregistrationonlyaccountedfor44.38%ofthetotalpopulationin2019.Thatis,aconsiderableamountofindividualslivingandworkingincitieshaveregisteredasruralresidents.In2020,thecentralgovernmentisaimingtoencourage100millionresidentstoobtaincityhouseholdregistration.WeexpectmanyofcitiesinChinatocancelorpartiallycancelhouseholdregistrationrestrictionsbytheendof2020,sothatindividualscanmigratefreelyfromtheiroriginalplaceofresidencytocityareas.Sofar,manyprovincesandmunicipalcitiesintroducedrelevantopinionsonhouseholdregistrationreforms,suchasGuangxiprovinceandGuangdongprovince.ManycitiesinChinahaveimplementedstricthousepurchasingrestrictions,targetingnon-localresidentsandlocalresidentsthatalreadyownhouses.Forpotentialhousebuyers,obtainingalocalhouseholdregistrationusuallymakesiteasiertoqualifyfortherighttopurchasearesidentialproperty.Inaggregate,householdregistrationreformisexpectedtoencouragealargenumberofindividualstomigrateintocities,thuscreatingstrongpurchasingdemandinlocalpropertymarkets.ThereisstillroomfortheurbanizationratetofurtherincreaseinChina.AccordingtotheUnitedNationsandtheWorldBank,theaverageurbanizationrateinhigh-income,middle-incomeandlow-incomecountriesaroundtheglobewas81.3%,52.5%and32.6%,respectively.ThecurrenturbanizationrateinChinahassurpassedtheaveragelevelofmiddle-incomecountries,butstilllowerthantheaveragelevelofhigh-incomecountries.Moreover,theurbanizationrateofsomedevelopingcountriesarehigherthanthatofChina,suchasRussiaandMalaysia.Consideringacceleratedhouseholdregistrationreformandcontinuedeconomicdevelopment,wethinkthattheurbanizationrateinChinaisstillfarfrompeaking.Figure5:UrbanizationRateinChinaFigure6:UrbanizationofSeveralCountriesin201859.58%60.60%56.10%57.35%58.52%42.35%43.37%44.38%39.90%41.20%92%83%82%81%81%80%77%76%74%50%36%34%65%60%55%50%45%40%35%30%JapanU.K.U.S.A.SouthKoreaCanadaFranceGermanyMalaysiaRussiaThailandVietnamIndia20152016201720182019CityResidents/TotalPopulationSectorReportRegisteredCityPopulation/TotalPopulationSource:theNationalBureauofStatisticsofChina,theNDRC.Source:theUnitedNations,theWorldBank.

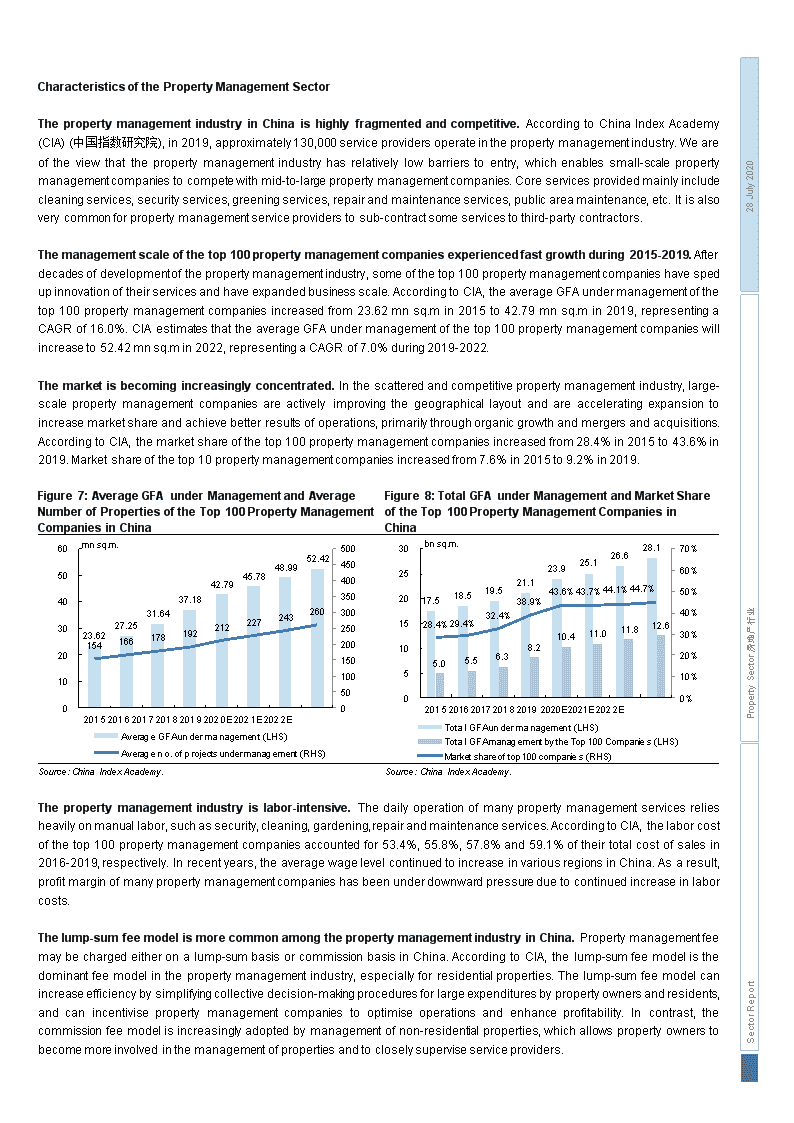

CharacteristicsofthePropertyManagementSector28July2020ThepropertymanagementindustryinChinaishighlyfragmentedandcompetitive.AccordingtoChinaIndexAcademy(CIA)(中国指数研究院),in2019,approximately130,000serviceprovidersoperateinthepropertymanagementindustry.Weareoftheviewthatthepropertymanagementindustryhasrelativelylowbarrierstoentry,whichenablessmall-scalepropertymanagementcompaniestocompetewithmid-to-largepropertymanagementcompanies.Coreservicesprovidedmainlyincludecleaningservices,securityservices,greeningservices,repairandmaintenanceservices,publicareamaintenance,etc.Itisalsoverycommonforpropertymanagementserviceproviderstosub-contractsomeservicestothird-partycontractors.Themanagementscaleofthetop100propertymanagementcompaniesexperiencedfastgrowthduring2015-2019.Afterdecadesofdevelopmentofthepropertymanagementindustry,someofthetop100propertymanagementcompanieshavespedupinnovationoftheirservicesandhaveexpandedbusinessscale.AccordingtoCIA,theaverageGFAundermanagementofthetop100propertymanagementcompaniesincreasedfrom23.62mnsq.min2015to42.79mnsq.min2019,representingaCAGRof16.0%.CIAestimatesthattheaverageGFAundermanagementofthetop100propertymanagementcompanieswillincreaseto52.42mnsq.min2022,representingaCAGRof7.0%during2019-2022.Themarketisbecomingincreasinglyconcentrated.Inthescatteredandcompetitivepropertymanagementindustry,large-scalepropertymanagementcompaniesareactivelyimprovingthegeographicallayoutandareacceleratingexpansiontoincreasemarketshareandachievebetterresultsofoperations,primarilythroughorganicgrowthandmergersandacquisitions.AccordingtoCIA,themarketshareofthetop100propertymanagementcompaniesincreasedfrom28.4%in2015to43.6%in2019.Marketshareofthetop10propertymanagementcompaniesincreasedfrom7.6%in2015to9.2%in2019.Figure7:AverageGFAunderManagementandAverageNumberofPropertiesoftheTop100PropertyManagementCompaniesinChinaFigure8:TotalGFAunderManagementandMarketShareoftheTop100PropertyManagementCompaniesinChinamnsq.m.52.4248.9945.7842.7937.1831.6426023.6215427.251662122272431781926050403020100201520162017201820192020E2021E2022EAverageGFAundermanagement(LHS)Averageno.ofprojectsundermanagement(RHS)50045040035030025020015010050030bnsq.m.28.126.623.925.121.119.543.6%43.7%44.1%44.7%17.518.538.9%28.4%29.4%32.4%12.610.411.011.88.25.05.56.32520151050201520162017201820192020E2021E2022ETotalGFAundermanagement(LHS)TotalGFAmanagementbytheTop100Companies(LHS)Marketshareoftop100companies(RHS)70%60%50%PropertySector房地产行业40%30%20%10%0%Source:ChinaIndexAcademy.Source:ChinaIndexAcademy.Thepropertymanagementindustryislabor-intensive.Thedailyoperationofmanypropertymanagementservicesreliesheavilyonmanuallabor,suchassecurity,cleaning,gardening,repairandmaintenanceservices.AccordingtoCIA,thelaborcostofthetop100propertymanagementcompaniesaccountedfor53.4%,55.8%,57.8%and59.1%oftheirtotalcostofsalesin2016-2019,respectively.Inrecentyears,theaveragewagelevelcontinuedtoincreaseinvariousregionsinChina.Asaresult,profitmarginofmanypropertymanagementcompanieshasbeenunderdownwardpressureduetocontinuedincreaseinlaborcosts.SectorReportThelump-sumfeemodelismorecommonamongthepropertymanagementindustryinChina.Propertymanagementfeemaybechargedeitheronalump-sumbasisorcommissionbasisinChina.AccordingtoCIA,thelump-sumfeemodelisthedominantfeemodelinthepropertymanagementindustry,especiallyforresidentialproperties.Thelump-sumfeemodelcanincreaseefficiencybysimplifyingcollectivedecision-makingproceduresforlargeexpendituresbypropertyownersandresidents,andcanincentivisepropertymanagementcompaniestooptimiseoperationsandenhanceprofitability.Incontrast,thecommissionfeemodelisincreasinglyadoptedbymanagementofnon-residentialproperties,whichallowspropertyownerstobecomemoreinvolvedinthemanagementofpropertiesandtocloselysuperviseserviceproviders.

28July2020Theaveragerevenueamountofthetop100propertymanagementcompaniesexperiencedfastgrowthduring2015-2019.Drivenbyorganicgrowthandexternalacquisitions,revenuefrompropertymanagementservicesregisteredsteadygrowth.AccordingtoCIA,averagetotalrevenueofthetop100propertymanagementcompaniesincreasedfromRMB540.8mnin2015toRMB1,040.2mnin2019,representingaCAGRof17.8%.In2019,averagerevenuefromcoremanagementservicesofthetop100propertymanagementcompaniesamountedtoRMB817.0mn,whichaccountedfor78.6%ofaveragetotalrevenue.Manypropertymanagementcompaniesdevelopedvalue-addedservicestofurtherexpandbusinessscope.Value-addedservices(VAS)mainlyinclude(i)VAStonon-propertyowners;and(ii)communityVAS.VAStonon-propertyownersmainlyconsistsofsalesassistanceservices,pre-deliverycleaning,repairandinspectionservices,preliminaryplanninganddesignconsultancyservicesandothertailoredservices.CommunityVASprimarilyconsistsofhomecleaningservices,shoppingservices,homedecorationservices,commonareamanagementservices,propertyagencyservices,travelagencyservices,etc.AccordingtoCIA,theaveragerevenueamountofthetop100propertymanagementcompaniesfromVASincreasedataCAGRof25.3%during2015-2019.Propertymanagementcompaniesdiversifiedtheirportfolioofpropertiesundermanagement.Amongthepropertiesundermanagement,residentialpropertiesaccountedforthelargestshareintermsoftotalGFAundermanagement.AccordingtoCIA,residentialproperties,officesandcommercialpropertiesaccountedfor68.88%,8.40%and6.63%,respectively,oftotalGFAundermanagementasattheendof2019.ManypropertymanagementcompaniesinChinahavealsosoughttomanageothertypesofproperties,suchaspublicproperties,industrialparks,schoolsandhospitals.Figure9:AverageRevenueoftheTop100PropertyManagementCompaniesinChinaFigure10:PercentageofGFAunderManagementbyPropertyTypein20191,6001,4001,200RMBmn1,040.21,165.01,304.81,461.31,115.0ResidentialCommercial1,000800600400627.8540.8519.3450.3742.1607.0886.2713.3817.0906.3258.61,005.3299.4346.3OfficesPublicPropertySector房地产行业Industrialparks200090.4108.5135.1172.9223.13.60%2.86%6.43%1.45%1.75%8.40%6.63%68.88%Schools201520162017201820192020E2021E2022EAveragerevenueAveragerevenuefromcorepropertymanagementservicesAveragerevenuefromvalue-addedservicesHospitalsOthersSource:ChinaIndexAcademy.Source:ChinaIndexAcademy.Manypropertymanagementcompanieshaveimprovedservicequalityandreducedoperatingcoststhroughadvancementofinformationtechnology.Withthehelpofinformationtechnologyapplicationssuchascloudapplications,e-commerce,internetofthings,bigdataandartificialintelligence,manypropertymanagementcompanieshavereducedlaborcostsandenhancedprofitability.Forexample,smartentrancetechnology,smartbuildingmanagement,smartenergymanagement,patrolrobots,deliveryrobotsandinquiryrobotsarelargelyreducinglaborcostsofpropertymanagementcompanies.Moreover,hi-techsolutionscanminimizehumanerrorandallowpropertymanagementcompaniestoapplystandardizedoperatingprocedures,thusimproveoverallservicequality.Forlarge-scalenationalpropertymanagementcompanies,centralizedinformationplatformsallowstaffatacompany’sheadquarterstomonitorthedailyoperationsoftheirbranches,subsidiariesandofficesacrossthecountry.SectorReportOperationofpropertymanagementcompanieshasbecomemoreindependent.Propertymanagementcompaniesusedtorelyheavilyontheiraffiliatedpropertydevelopmentcompaniesorparentgrouptoacquireprojects.Agrowingtrendisthatpropertymanagementcompaniesarebecomingmoreindependentandmarket-oriented.Manypropertymanagementcompaniesareproactivelyseekingnewopportunitiesfromindependentthird-partydevelopersaswellaspropertyownerstoexpandbusinessscaleandmarketshare.

PeersComparison&Valuation28July2020Highvaluationimpliesmarketconfidencetowardsthepropertymanagementsector.Currently,thePERofthepropertymanagementsectorisbasicallyonanupwardtrendandhasbrokenthroughitshistoricalhigh,reachingupto40.6xofforwardPER.Similarly,theforwardPBRofthepropertymanagementsectorhasachievednewhighsto9.6x.TheCOVID-19pandemichasnegativelyimpactedmanyindustriesresultinginfallingvaluations.However,thoughthevaluationofthepropertymanagementsectorwasdraggedforashortperiodduringMar.2020,thestrongrecoveryindicatesmarketconfidencetowardsthepropertymanagementsector.Wethinkthatthecurrenthighvaluationofthepropertymanagementindustryhasthreemajorsupportingfactors:1)thebusinessmodelofpropertymanagementcompaniesunderhighcontractrenewalratesissustainableandprofitable,essentiallyindicatinghighervaluationlevel;2)highcertaintyofgrowthintheshortandmediumterm,drivenbycoexistenceofinternalorganicgrowth(throughaffiliatedpropertydevelopers)andexternalstrategicexpansion(throughbidsandM&A);and3)long-termrichimaginationofmarketsize.Overall,thepropertymanagementindustryishighlydefensiveandhasbeenrelativelylessaffectedbytheCOVID-19pandemic,withvaluationsstayingstronginanunfavorablemarket.Figure11:ForwardPERinthePropertyManagementSector5045403530252015105030.21.13.Figure12:ForwardPBRinthePropertyManagementSector12.010.08.06.04.02.00.07.75.83.8PropertySector房地产行业P/EAVGSTD-1STD+1P/BAVGSTD-1STD+1Source:Bloomberg,GuotaiJunanInternational.Source:Bloomberg,GuotaiJunanInternational.Valuationvarianceamongpropertymanagementcompaniesisquitelarge.Wehaveselected26HKEX-listedcompaniesinthataremainlyengagedinpropertymanagementinthePRCasindustrypeers(the"peersgroup").Mostofthecompaniesinthepeersgrouparepropertydeveloper-affiliatedpropertymanagementserviceprovidersandareexpectedtomaintainfastgrowthtrendsinthecomingyears,alongwiththeirparentgroups’expansion.The2020FPERandPBRofthepeersgrouprangedfrom9.7xto56.8xandfrom1.1xto14.8x,respectively.Wethinkthatthevaluationvarianceofthepropertymanagementcompaniesismainlyattributableto1)varyingbackgroundsofaffiliatedpropertydevelopers,2)thegrowthrateofpropertymanagementcompanies,and3)scaleofpropertymanagementcompanies.SectorReportPropertymanagementcompaniesbackedbyalargerbackgroundofaffiliatedpropertydevelopershaverelativelyhighervaluation.Amongthepeersgroup,thevaluationsofpropertymanagementcompaniesshowedapositivecorrelationwiththescaleoftheirparentpropertydevelopmentcompanies.AccordingtoCRIC,thepeersgroup,whichissecondarytothetop-20largestpropertydevelopersrankedbycontractedsalesduringJan.-Jun.2020,hasgainedhighervaluations,with2020FPERrangingfrom40.0xto56.8xand2020FPBRrangingfrom7.2xto14.8x.ThepredominantwayofinternalorganicgrowthtoincreaseGFAundermanagementistoacquirefromparentpropertydevelopers.Theprojectareaindependentlydevelopedbydevelopmentcompanieswillbetransformedintomanagementareasofpropertyservicecompanies.Propertymanagementcompaniesderivedfromlargerdevelopershaveadoptedfollow-upstrategies.Byfollowingtheexpansionofaffiliateddevelopersandtakingadvantageofdevelopers"brands,propertymanagementcompaniesarebenefittingfromsynergybetweenexistingandnewmarkets.

28July2020Propertymanagementcompanieswithhighergrowthrateenjoycomparativelyhighervaluation.Amongthepeersgroup,EverSunshine(01995.HK)andTimesNeighborhood(09928.HK)hadhighCAGRofrevenueduring2019-2022,bothbeyond50%,with2020FPERreaching54.4xand47.2x,respectively,reachingthetoplevelofthepeersgroup.Incontrast,ColorfulLife(01778.HK)hadaCAGRofrevenueduring2019-2022below10%,resultinginalowvaluationwith2020FPERof8.8xand2020FPBRof1.1x.Wethinkthatthefastgrowthrateofpropertymanagementcompaniesisconducivetoliftinguptheirvaluationbystrengtheningearningsandenrichingcashflows.Valuationsarecategorizedbythescaleofthepropertymanagementcompanies.Amongthepeersgroup,largerpropertymanagementcompaniesgenerallyearnhighervaluations.Thesimpleaverage2020FPERoftop-10,11-20and21-26propertymanagementcompaniesamountsto43.8x,18.6xand9.7x,respectively.ScaleisthecornerstoneofthedevelopmentofpropertymanagementcompaniesandtheMattheweffectofthereserveareagraduallybecomesprominent.Underthestablegrowingmarket,leadingcompaniesoflargescalearemorelikelytohavelargermarketsharethroughpropertyprojectsdeliveredbytheparent/relatedcompanies,andthroughbiddingandM&As.Table1:PeersComparison2019Ranking2019-202220192021F2022F2020FCAGR2019-2022(HK$m)2020F2021F2022FPBPEParents’ContractedCAGRSales1H20NetProfit(RMBmn)Revenue(RMBmn)StockCodeMktCapCompanyCountryGardenServices06098HK120,99914,19119,03724,75136.9%2,2533,0854,13635.3%161.619.8A-LivingServices03319HK60,6679,90513,23516,27347.0%1,7202,2342,78731.3%2443.68.8PolyPropertyDevelopment*06049HK46,3428,17710,88914,28233.8%7331,0021,34540.0%461.07.9GreentownServiceGroup02869HK34,35710,56313,01215,93322.9%6338291,05730.3%755.49.7ChinaOverseasProperty02669HK27,6106,1977,7829,63226.0%6268071,00428.4%651.318.2EverSunshine01995HK23,7202,9844,4866,36750.2%36857283955.3%1885.917.0S-EnjoyService01755HK19,2252,9604,2505,90042.9%42361986645.4%1460.918.6CentralChinaNewLife*09983HK12,7742,7174,2295,87849.6%36456175347.6%53n.a.n.a.TimesNeighborhood*09928HK12,5571,8653,0464,34859.0%22639958482.4%4586.411.6PowerlongCommercial*09909HK12,2442,1322,8993,80332.9%28240956546.8%4739.56.7SichuanLanguangJustbon*02606HK9,1192,9804,2946,22643.7%5987961,06235.2%3814.63.7AoyuanHealthyLife03662HK5,7661,4752,1332,66143.5%24033842838.1%2829.46.1ZhenroServicesGroup*06958HK5,520n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.21n.a.n.a.ColourLifeServicesGroup01778HK5,4414,0754,3974,8047.7%5505826589.7%699.01.2KaisaProsperityHoldings02168HK5,3131,7382,3823,24637.0%23633146441.5%2726.06.5BinjiangServiceGroup03316HK5,2088891,1341,42826.7%16120926031.4%2637.76.4FinancialStreetProperty*01502HK3,366n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.7521.1n.a.RedsunServicesGroup*01971HK2,432n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.46n.a.n.a.YinchengLifeService*01922HK1,897n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.14839.113.9XinyuanProperty*01895HK1,561n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.9411.51.7ZhongAoHomeGroup01538HK1,4531,7442,153n.a.n.a.129170n.a.n.a.n.a.11.31.8RiverineChinaHoldings01417HK919n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.50.03.6HevolServicesGroup*06093HK634n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.29.32.9CliffordModernLiving03686HK589n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.5.41.3XingyeWulianService*09916HK576n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.7610.63.4YeXingHoldings*01941HK571n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.15113.26.7SimpleAverage4,6626,2108,36937.3%5968091,12039.9%37.18.1WeightedAverage8,35711,13414,30636.1%1,1641,5782,08136.2%52.212.6PropertySector房地产行业Source:CRIC,Bloomberg,GuotaiJunanInternational.Notes:(1)Companieswith"*"markwerelistedin2019andweaddedbacktheirlistingfeesinthecalculationofcorenetprofitandtheCAGRfrom2019-2022.SectorReport(2)TherankingofcontractedsalesisreferencedfromCRICandrepresentsrankingofaccumulatedcontractedsalesfromrelatedpropertydeveloperin1H20.

SectorReport28July2020Table2:PeersValuationTableCompanyStockCodeMktCapLastPricePEPBD/Y(%)ROE(%)(HK$m)(HK$)2020F2021F2022F2020F2021F2022F2020F2020FPropertyManagementCompaniesCountryGardenServices06098HK120,99943.85047.736.627.414.811.38.50.533.8A-LivingServices03319HK60,66745.50031.724.319.37.46.45.31.325.1PolyPropertyDevelopment06049HK46,34283.75056.841.530.67.26.45.60.513.2GreentownServiceGroup02869HK34,35710.68044.734.526.96.65.95.10.816.5ChinaOverseasProperty02669HK27,6108.40040.031.124.713.510.27.90.736.7EverSunshine01995HK23,72014.20054.435.524.110.78.87.10.622.4S-EnjoyService01755HK19,22523.50041.227.819.714.410.87.81.337.0CentralChinaNewLife09983HK12,77410.26030.820.014.94.23.63.11.021.1TimesNeighborhood09928HK12,55712.74047.227.318.67.86.55.10.619.5PowerlongCommercial09909HK12,24419.70038.026.319.45.95.14.41.215.7SichuanLanguangJustbon02606HK9,11951.20013.810.47.93.12.62.12.724.7AoyuanHealthyLife03662HK5,7667.94021.615.412.25.24.23.51.926.8ZhenroServicesGroup06958HK5,5205.520n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.ColourLifeServicesGroup01778HK5,4413.7408.88.07.31.11.00.93.013.4KaisaProsperityHoldings02168HK5,31334.50019.013.89.84.03.42.91.927.2BinjiangServiceGroup03316HK5,20818.84029.722.618.3n.a.n.a.n.a.1.721.2FinancialStreetProperty01502HK3,3669.350n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.RedsunServicesGroup01971HK2,4326.080n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.YinchengLifeService01922HK1,8977.100n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.XinyuanPropertyManagement01895HK1,5612.840n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.ZhongAoHomeGroup01538HK1,4531.7009.77.8n.a.1.41.2n.a.1.8n.a.RiverineChinaHoldings01417HK9192.270n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.HevolServicesGroup06093HK6341.320n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.CliffordModernLiving03686HK5890.580n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.XingyeWulianService09916HK5761.440n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.YeXingHoldings01941HK5711.410n.a.n.a.n.a.n.a.n.a.n.a.n.a.n.a.SimpleAverage33.423.918.77.25.84.91.323.6WeightedAverage40.629.922.59.67.66.00.924.9PropertySector房地产行业Source:Bloomberg,GuotaiJunanInternational.'

您可能关注的文档

- 物业管理行业专题研究报告:社区养护市场化曙光初现-20190709-中信证券.pdf

- 湖北物业管理行业发展现状与趋势浅析.doc

- 物业管理行业专题:从单盘模型透视品质之路的丰厚回报-20200113-中信证券.pdf

- 物业管理行业:大数据解构与关键问题再思考-20200117-华菁证券.pdf

- 营改增对物业管理行业的影响及对策-论文.pdf

- 湖南省房地业协会物业管理行业专家申请表.doc

- 关于物业管理行业发展的背景环境.doc

- 物业管理行业发展的背景环境.doc

- 物业管理行业服务规范.doc

- 深圳市物业管理行业廉洁自律公约.docx

- 我国物业管理行业概况研究.pdf

- 物业管理行业人力资源保障体系建设初探.doc

- 物业管理行业规范招投标机制的思考.doc

- 物业管理行业动态展望.doc

- 物业管理行业风险和防范措施.doc

- 专题培训一览表-广州物业管理行业协会.doc

- 全国物业管理行业职业技能竞赛电工理论知识考核预赛试题.pdf

- 我县物业管理行业运行情况调研报告.doc