- 2.59 MB

- 2022-04-29 13:58:16 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

'中国可再生能源目录PMSummary4INDUSTRYANALYSIS7Costreductionsaccelerating8Operatingenvironmentimproving16Valuation:Attractiverisk/rewardprofiledespiteshort-termpolicyuncertainties21Risks26COMPANYANALYSIS27LongiGreen(601012.SS):Drivingglobalmonopenetration;initiateatBuy28ZhejiangChint(601877.SS):Drivingfull-cyclesolarsolution;initiateatBuy40Tongwei(600438.SS):Emergingpolygiant;initiateatBuy52Goldwind(2208.HK/002202.SZ):Leadingturbinemaker;initiateH-shareatBuy62HuanengRenewable(0958.HK):ContinuedimprovementinutilizationtodriveEBITmargin;initiateatBuy72XinyiSolar(0968.HK):LeadingPVglassmaker,butvaluationpremiumunjustified;initiateatSell78LongyuanPower(0916.HK):Offshoreprojectstosupportinstallations;initiateatNeutralonlimitedupside86SungrowPower(300274.SZ):Growingglobalsharesbutvaluationfair;initiateatNeutral92APPENDICES101Appendix1:Stabilityofsupplyfromupstreamkeycomponent102Appendix2:Sectorbackground:highgrowthfueledbyhighsubsidy103Appendix3:M&AFramework106信息披露附录108

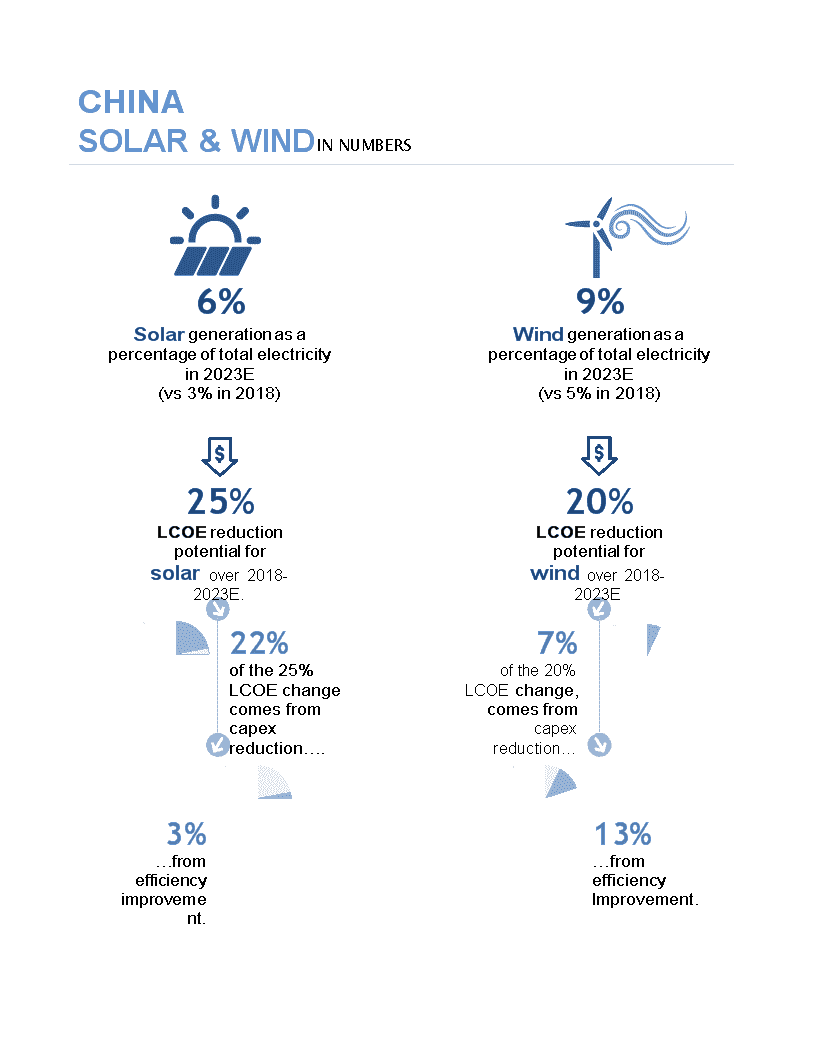

CHINASOLAR&WINDINNUMBERS6%Solargenerationasapercentageoftotalelectricityin2023E(vs3%in2018)9%Windgenerationasapercentageoftotalelectricityin2023E(vs5%in2018)25%LCOEreductionpotentialforsolarover2018-2023E.22%ofthe25%LCOEchangecomesfromcapexreduction….20%LCOEreductionpotentialforwindover2018-2023E7%ofthe20%LCOEchange,comesfromcapexreduction…3%…fromefficiencyimprovement.13%…fromefficiencyImprovement.

研究中国256GWofsolarinstallationweexpectChinatoaddover2018-2023.150GWofwindinstallationweexpectChinatoaddover2018-2023.

研究中国PMSummaryAcceleratingcost-reductionandimprovingoperatingenvironmenttodriveinstallationoutlook;BuycostleadersinupstreamandefficiencyleadersindownstreamWeforecast25%/20%costreductionsforsolar/windpowerin2018-23E.Webelievede-subsidizationpoliciespublishedinMay2018haveacceleratedcostreductionsforsolarandwindpowerinChina.WeforecastaverageLCOE(levelizedcostofelectricity)ofutility-scalesolarandon-shorewindpowerofUS$0.063/kwhandUS$0.060/kwhin2018,andweexpecttechnologicaladvancementstodrivefurthercostsreductionsof25%/20%in2018-23E.Improvingoperatingenvironment.Weexpecttheoperatingenvironmentofthesolarandwindsectorstograduallyimproveas:1)powerdemandinChinaremainsresilientin2019andbeyonddespiteapotentialeconomicslowdown;2)thereinforcementofRPS(RenewableEnergyPortfolioSystem)andthepotentialopeningupofsubsidy-freeprojectspromoterenewableenergyinvestment(solarandwindinparticular)overthelongterm.Competitionstillfiercedespiteasolidinstallationoutlook;leadersstandoutamidsectorconsolidation.Weforecastrapidlydeclininggenerationcostsandanimprovingoperatingenvironmenttodrive256GW/150GWsolar/windinstallationsin2018-23EwithaggregatecapexinvestmentofRmb1,040bnandRmb1,083bn,respectively.Weexpectupstreamcompetitiontoremainfierce,especiallyinthesolarsector,andupstreamconsolidationtocontinue.WeexpectupstreamleaderswithR&Dandexecutionstrengthtostandout,anddownstreamleaderswithoutstandingoperatingefficiencyandstrongbalancesheetstobenefitfromcostreductionsintheupstreamvaluechain.OurtopBuypicksareLongi,ZhejiangChintandHNR.WebelieveChina’ssolarandwindsectorsofferattractiveriskandreturnprofileswithvaluationsbelowtheaverageofthepastthreeyearandasolidgrowthoutlook.ExceptforLongiandZhejiangChint,ourestimatesare0%-6%belowconsensusfor2018,broadlyinlinefor2019,and2%-20%abovefor2020(exceptforLongyuan).WeinitiateatBuyonLongi,ZhejiangChint,Tongwei,HNRandGoldwind-H;weinitiateatNeutralonSungrow,LongyuanandGoldwind-A.WeinitiateatSellonXinyiSolaraswebelieveitsvaluationpremiumovercomparablepeersisunjustified(mostofourcoveragetradesbelowtheaveragesforcomparablepeers)Our12-monthtargetpriceforXinyiimplies8%downsidevs.the27%averageupsideforoursolarcoverageandthe27%averageupsideforourcombinedsolarandwindcoverage.AsshowninExhibit1,werankoursolarandwindcoverageusingaframeworkthatassessestheirvolumegrowthoutlook,company-specificcatalysts,

upside/downsidetoourtargetprice,netgearing,andcyclicalexposure.Allcategoriesareequallyweighted,withamaximumscoreof5andaminimumscoreof-5.

研究中国LongiandZhejiangChintrankhighestinsolar;HNRandGoldwind-Hrankhighestinwind.图表1:InvestmentframeworkCompanyVolumegrowth2018-20ESolarCompany-specificcatalystsUpside/downsideLongi76%wafershipmentgrowth+Marketsharegain;costreduction+45%upsidetoourRmb26.3/sh,12-monthpricetarget+Chint45%generationgrowthand117%EPCvolumegrowth+Marketsharegain;operatingefficiencyimprovement+38%upsidetoourRmb32.3/sh,12-monthpricetarget+Tongwei300%polyshipmentgrowth+Marketsharegain;costreduction+42%upsidetoourRmb12.3/sh,12-monthpricetarget+Sungrow63%invertershipmentgrowth+Marketsharegain;costreduction+19%upsidetoourRmb11.0/sh,12-monthpricetarget+/-Xinyi46%PVglassshipmentgrowth+Marketsharegain+8%downsidetoourHKD2.6/sh,12-monthpricetarget-WindHNR16%generationgrowth+/-Operatingefficiencyimprovement;cashflowimprovement+42%upsidetoourHKD3.0/sh,12-monthpricetarget+Goldwind-H32%turbineshipmentgrowth+Marketsharegain;costreduction+37%upsidetoourHKD10.4/sh,12-monthpricetarget+Longyuan9%generationgrowth+/-Operatingefficiencyimprovement;cashflowimprovement+13%upsidetoourHKD6.1/sh,12-monthpricetarget+/-Goldwind-A32%turbineshipmentgrowth+Marketsharegain;costreduction+18%upsidetoourRmb12.7/sh,12-monthpricetarget+/-CompanyNetdebt/equity2018ESolarCyclicalexposureScoreLongi-10%+Manufacturer,developer+/-4Chint15%+Assetownership,developer,manufacturer+/-4Tongwei29%+/-Assetownership,manufacturer+/-3Sungrow-27%+Manufacturer,developer+/-3Xinyi59%-Manufacturer,developer+/-0WindHNR152%-Assetownership+2Goldwind-H73%-Assetownership,developer,manufacturer+/-2Longyuan110%-Assetownership+1Goldwind-A73%-Assetownership,developer,manufacturer+/-1Note:“+”=+1,“-”=-1,“+/-”=0,allcategoriesequalweight,with5/-5max/minscores.资料来源:Companydata,GaoHuaSecuritiesResearch图表2:SummaryofourvaluationmethodologyUpside/ValuationTargetCompanyRatingPricetargetdownsidemethodologymultipleBenchmarkRationale(%)(x)SolarLongiBuy26.3Rmb/sh45%EV/EBITDA16.5HistoricalaverageLongi’scurrentEV/EBITDAwasslightlyhigherthantheaverageofpast5-yearrange,butofpeergrouplowerthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.ChintBuy32.3Rmb/sh38%EV/EBITDA10.5HistoricalaverageChint’scurrentEV/EBITDAwasbelowaverageofitspast5-yearrange,andalsolowerofpeergroupthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.TongweiBuy12.3Rmb/sh42%EV/EBITDA10.2HistoricalaverageTongwei’scurrentEV/EBITDAislowerthanaverageofitspast5-yearrange,andalsoofpeergrouplowerthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.SungrowNeutral11.0Rmb/sh19%EV/EBITDA8.5HistoricalaverageSungrow’scurrentEV/EBITDAislowerthanaverageofpast5-yrrangeandcomparableofpeergrouppeer’spast5-yraverage.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.XinyiSell2.6HKD/sh-8%EV/EBITDA7.4HistoricalaverageXinyi’scurrentEV/EBITDAislowerthanhistoricalaverage,buthigherthancomparableWindofpeergrouppeershistoricalaverage.AlthoughwebelieveXinyioperateswithmorediversifiedbusinessandbetterprofitabilities□andgrowthoutlookagainstitspeers.Webelieveitsvaluationpremium□isunjustifiedasmostofourpreferredpicksaretrading□atbelowaveragemultipleofpeersgroup.HNRBuy3.0HKD/sh42%EV/EBITDA6.5-0.5stdofhistoricalHNR’scurrentEV/EBITDAwaslowerthanaverageofpast3-yrrangeandcomparableaveragepeershistoricalaverage.Sincethebeginningof2018,HNRhasbeentradingbetweenpast3-yraverageand1stdbelowaverage.Itappearsthereisade-ratingin2018comparedtotheaverageof2016/17,duetoinvestors’concernonsubsidypaymentandutilization.Wehavediscountedourmorepositiveviewinourestimates,andadopt0.5stdbelowhistoricalaverage(medianofYTDrange)astargetmultiple.Goldwind-HBuy10.4HKD/sh37%EV/EBITDA10.0HistoricalaverageGoldwind-H’scurrentEV/EBITDAislowerthantheaverageofpast5-yrrange,alsolowerofpeergroupthanhistoricalaverageofpeergroup.Withagrowthoutlookhigherthansectoraverage,weexpectthecompanytotradeuptohistoricalaverageofpeergroup.LongyuanNeutral6.1HKD/sh13%EV/EBITDA5.7-1stdofhistroicalLongyuan’scurrentEV/EBITDAwaslowerthanaverageofpast3-yrrangeandaveragecomparablepeershistoricalaverage.Sincethebeginningof2018,Longyuanhasbeentradingbetweenpast3-yraverageand1stdbelowaverage.Itappearsthereisade-ratingin2018comparedtotheaverageof2016/17,duetoinvestors’concernonsubsidypaymentandutilization.Wehavediscountedourmorepositiveviewinourestimates,andadopt1stdbelowhistoricalaverage(0.5stdbelowHNR’stargetmultipleonlowerEBITDAgrowthoutlook)astargetmultiple.Goldwind-ANeutral12.7Rmb/sh18%EV/EBITDA12.3-1stdofhistoricalGoldwind-A’scurrentEV/EBITDAislowerthanaverageofpast5-yrrange.Goldwind’sA-averagesharehas47%averagepremiumoverH-sharesincethebeginningof2013.Webelievethisisduetodifferentperceptionofwindinstallationoutlookfromon-shoreandoff-shoreinvestors.Weapply1stdbelowhistoricalaverageastargetmutiple.资料来源:GaoHuaSecuritiesResearchWeadoptEV/EBITDAastheprimaryvaluationmethodologyforoursolarandwindcoverage.Weselectthecomparablepeergroupasavaluationreferencebasedonthenatureofeachcompany’sbusiness.Weapplytheaveragehistoricalmultipleofthepeergrouptoourcoverage(exceptforLongyuan,HNRandGoldwind-A).ForLongyuan

研究中国andHNR,weapply-1std/0.5stdbelowthehistoricalaveragetoreflectthede-ratingofthetwocompaniessincethebeginningof2018oninvestorconcernsaroundsubsidiesandutilization;wehavereflectedourmorepositiveviewinourestimatesaswebelievetheseissuescouldgraduallyimproveasRPSisreinforced.Weapply1stdbelowthehistoricalaveragetoGoldwind-Aasithasbeentradingatanaverage47%premiumoverGoldwind-H,whichweattributetodifferingperceptionsonthewindinstallationoutlookamongon-shoreandoffshoreinvestors.图表3:Derivationsummaryforour12-monthtargetpricesLongiChintTongweiSungrowXinyi601012.SS601877.SS600438.SS300274.SZ0968.HK2018EV/EBITDA15.410.111.19.29.72019EV/EBITDA11.78.07.57.18.4Historicalaverage14.110.69.419.112.7Histroricalmean12.69.78.718.610.0Peer’saverage16.710.410.28.67.4Peer’s18-20EBITDAcagr22%17%13%8%11%Company18-20EEBITDAcagr31%25%35%26%18%2019EEBITDA4,3876,7815,0921,5683,6172019ENetdebt(1,100)2,6764,091(2,614)6,718TargetmultipleBenchmark16.510.510.2Historicalaverageof8.5peergroup7.4Targetprice26.332.312.311.02.6CurrentPrice18.223.58.79.22.9PricecurrencyCNYCNYCNYCNYHKDUpside45%38%42%19%-8%RatingBUYBUYBUYNeutralSellImplied2019P/E23.014.815.715.38.6Implied2020P/E16.611.312.011.77.4Historicalmedianlevel(2013-18)23.316.523.4188.9LongyuanHNRGoldwind-HGoldwind-A0916.HK0958.HK2208.HK002202.SZ2018EV/EBITDA6.26.210.614.32019EV/EBITDA5.65.98.511.4Historicalaverage7.37.410.715.0Histroricalmean7.47.410.714.6Peer’saverage8.08.010.210.2Peer’s18-20EBITDAcagr5%5%15%15%Company18-20EEBITDAcagr6%6%29%29%2019EEBITDA17,97410,8135,3405,3402019ENetdebt58,94142,31920,52420,524Targetmultiple5.76.510.012.31stdbelowhistorical0.5stdbelowhistoricalHistoricalaverageof1stbelowBenchmarkaverageaveragepeergrouphistoricalaverageTargetprice6.13.010.412.7CurrentPrice5.42.17.610.8PricecurrencyHKDHKDHKDCNYUpside13%42%37%18%RatingNeutralBUYBUYNeutralImplied2019P/E9.48.18.810.8Implied2020P/E8.47.17.18.7Historicalmedianlevel(2013-18)13.18.49.312.9资料来源:GaoHuaSecuritiesResearch,Wind,Bloomberg

研究中国INDUSTRYANALYSIS

CostreductionsacceleratingWebelievefavorablesubsidypolicieshavedrivenmassiveinvestmentandrapidtechnologicaladvancementacrossChina’ssolarandwindsectors,whichhasledtosubstantialcostreductionsoverthelastfiveyears.WeestimateLCOElevelsforsolar/windpowerinChinafell55%/19%in2012-17.Asgenerationcostsdeclinerapidlyandtheoperatingenvironmentimproves,weexpectChina’swindandsolarsectorswillgraduallymovefromasubsidy-driventocost-drivenmodel.图表4:ChinasolaraverageFiTandLCOE图表5:ChinawindaverageFiTandLCOE1.21.11.00.90.80.70.60.50.40.30.2(Rmb/kwh)(Rmb/w)10.09.08.07.06.05.04.03.02.01.00.00.70.60.60.50.50.40.40.39.0(Rmb/kwh)(Rmb/w)8.07.06.05.04.03.02.01.00.0201320142015201620172018E2023ECAPEX(RHS)Coal-fired-FiTSolar-FiTSolar-LCOE201320142015201620172018E2023ECAPEX(RHS)Coal-fired-FiTWind-FiTWind-LCOE研究中国资料来源:NEA,CEC,GaoHuaSecuritiesResearchEstimate资料来源:NEA,CEC,GaoHuaSecuritiesResearchEstimate2018policeshaveacceleratedcostreductions...Webelievethede-subsidizationpoliciespublishedinMay2018haveacceleratedthisprocess.nOnMay18,theNEApublishedanoticestatingthatalltheprovinceswhichhavenotpublished2018windinstallationplansshouldadoptacompetitivebiddingprocesswhenallocatingwindprojectquotaandsettingFiTs(Feed-in-Tariff),andallon-shoreandoffshorewindprojectsshouldbeallocatedquotasandFiTbasedonacompetitivebiddingprocessstartingfrom2019.nOnMay31,theNEA,theNDRCandtheMoFjointlypublishedanoticeregardingsolarpower,statingthatinordertooptimizesolarinstallation:1)noquotaswouldbeallocatedforutility-scalesolarprojectsthatneedsubsidiesinanyformduring2018(2017installation:33GW)andquotaforDG(distributedgeneration)solarprojectswithsubsidieswouldbelimitedto10GW(2017DGinstallation:19GW);2)feed-in-tariffofutility-scalesolarfarmswouldbereducedbyRmb0.05/kwhtoRmb0.5/0.6/0.7/kwhinZoneI/II/IIIandsubsidiesforDGprojectsreducedbyRmb0.05/kwhtoRmb0.32/kwh.Followingthesepolicychanges(fromMay31toOctober21),sharepricesformajorsolar/windnamesfell31%/39%(marketcapweightedaverage)vs.a17%declinefortheCSI300.

图表6:SharepricemovementsforkeysolarandwindcompaniesinChina1.01.00.90.90.80.80.70.70.61.1SolarWindCSI300Note:Solarnames:LongiGreen,SungrowPower,TongweiCo.,XingyiSolar,ZhejiangChint;Windnames:LongyuanPower,HuanengRenewable,Goldwind资料来源:WindKeysolarproductshaveseenasignificantASPdeclineduringJunetoOctober(vs.January-May),astheabruptpolicychangescausedasharpdeclineininstallationsduring3Q18.Chinapolysilicon/wafer/cellASPsfellasmuchas23%/37%/32%inJune-Octobervs.declinesof8%/25%/25%inJanuary-May.ModuleASPssawaslightrecoveryinlateAugustdrivenbythestart-upoffront-runnerprograms.图表7:ASPmovementofkeysolarproductsinChina图表8:Averagebiddingpricefor2.0MWwindturbineMonomoduleMultimoduleMonocellMulticellMonowaferMultiwaferPolysilicon3,800(Rmb/kw)3,7003,6003,5003,4003,3003,2003,1003,0002,900-40%-35%-30%-25%-20%-15%-10%-5%0%Jun-Oct2018Jan-May2018Averagebiddingpricefor2.0MWturbine研究中国资料来源:PVinsight资料来源:Goldwind

WeestimateaverageLCOEofutility-scalesolarandon-shorewindpowerwasUS$0.063/kwhandUS$0.060/kwhin2018,andweexpecttechnologicaladvancementcoulddrivefurthercostreductionsof25%and200%in2018-23E.Weexpectsolar

研究中国LCOEreductiontomainlybedrivenbyupstreamcapexreductionandLCOEreductiontobedrivenbyanimprovementinsystemefficiencies.图表9:Weestimate25%and20%LCOEreductionpotentialforsolarandwindin2018-23ELCOEcalculationformajorpowerprojectsinChina2018ELCOEGasSolar-DGOff-shorewindSolar-utilityOn-shoreWindCoalNuclearHydroCapex/kW(Rmb)Capex/kW(USD)5,0007355,20076512,0001,7654,5006627,2501,0663,80055915,0002,2068,0001,176Lifetime(Yrs)2020202020303030Utilizationhours3,6001,1002,8001,2502,0004,2007,0003,500Equityfinancing%25%25%25%25%25%25%25%25%Debtfinancing%75%75%75%75%75%75%75%75%Equityrequiredreturn8%8%8%8%8%8%8%8%Debtrequiredreturn6%6%6%6%6%6%6%6%LCOE(Rmb/kwh)0.730.570.500.430.410.360.330.26LCOE(USD/kwh)0.1070.0830.0740.0630.0600.0540.0480.0382023ELCOEGasSolar-DGOff-shorewindSolar-utilityOn-shoreWindCoalNuclearHydroCapex/kW(Rmb)Capex/kW(USD)5,0007354,10060311,2001,6473,5005156,7009853,80055915,0002,2068,0001,176Lifetime(Yrs)2020202020303030Utilizationhours3,6001,1503,2501,3002,3004,2007,0003,500Equityfinancing%25%25%25%25%25%25%25%25%Debtfinancing%75%75%75%75%75%75%75%75%Equityrequiredreturn8%8%8%8%8%8%8%8%Debtrequiredreturn6%6%6%6%6%6%6%6%LCOE(Rmb/kwh)0.730.430.410.320.330.360.330.26LCOE(USD/kwh)0.1070.0630.0600.0470.0480.0540.0480.038(USD/kwh)(USD/kwh)25%reductionpotentialforUtility-scaleSolar20%reductionpotentialforOn-shoreWindGasSolar-DGOff-shorewindSolar-utilityOn-shoreWindCoalNuclearHydro0.120.120.100.100.080.080.060.060.040.040.020.020.00-LCOE-2018ELCOE-2023E资料来源:GaoHuaSecuritiesResearchSolarcostreductionsdrivenbycapexreductionWeforecastLCOEofutility-scalesolartofall25%in2018-23E(22pptfromcapexreductionand3pptfromefficiencyimprovements).Weexpectunitcapexforutility-scalesolarpowertofallfromUS$0.66/win2018EtoUS$0.52/win2023E.

图表10:WeexpectlowercapextobethemaindriverofreductioninsolarLCOEUtility-scalesolarLCOE/CAPEXbreakdownandsensitivityanalysis0.70(USD/w)0.07WeexpectCAPEXtodeclineby22%over2018-23E(USD/w)WeexpectLCOEtodeclineby25%over2018-23E,22%fromCAPEXreduction,3%fromefficiencyimprovement0.060.600.050.500.040.030.020.400.010.300.002018E2023EDepreciationcostFinancialcostOPEX0.200.100.002018E2023ECAPEX(Rmb/kw)Utilizations2,8353,1503,5003,8504,2351,1370.300.330.370.400.451,1970.280.310.350.380.421,2600.270.300.330.370.401,3230.260.280.320.350.381,3890.240.270.300.330.36CAPEX(Rmb/kw)研究中国2,8353,1503,5003,8504,2351,137-10%0%11%22%34%1,197-15%-5%5%16%27%Utilizations1,260-19%-10%0%10%21%1,323-23%-14%-5%5%15%1,389-27%-18%-9%0%10%PolyproductioncostPolygrossprofitWaferprocessingcostWafergrossprofitCellprocessingcostCellgrossprofitModuleprocessingcostModulegrossprofitSolarinverterBOS资料来源:GaoHuaSecuritiesResearchTechnologicaladvancestodrivecostreductionsacrossvaluechainWeexpecttechnologicaladvancestobethemaindriverofcostreductionsacrossthevaluechain.nPoly-silicon:Moreadvancedhydrogenationprocesstoreduceelectricitycosts.AccordingtoBloombergNewEnergyFinance(BNEF),electricitycostsaccountfor48%ofproductioncostsforpolysilicon.AccordingtotheChinaPhotovoltaicIndustryAssociation(CPIA),averageunitpowerconsumptionwas65Kwh/kgin2018,andisexpectedtobefurtherreducedto58kwh/kgin2025Ethroughamoreadvancedhydrogenationprocess.Inaddition,moreleadingplayersarebuildingnewcapacityinregionswithlowerpowertariffssuchasInnerMongolia,Sichuan,etc.

图表11:ElectricityisthelargestcomponentforpolysiliconproductionCostbreakdownofpolysiliconproduction图表12:Unitpowerconsumptioncouldfallfrom65kwh/kgin2018to58kwh/kgin2025Averageunitpowerconsumptioninpolysiliconproductionprocess85.0(Kwh/kg)16%7%48%29%80.075.0ElectricitySiliconmetalLabourGas,steam,O&Mandothers70.065.060.055.050.0201620172018202020222025Unitpowerconsumtion资料来源:BNEF资料来源:CPIAnWafers:Moreadvanceddiamondwire(DW)cuttingtoincreasewaferyield,andrisingmonopenetrationtodriveefficiencies.Weexpectrisingcostperformanceandbettercost-reductionpotentialandupsideforefficiencyimprovementtofurtherdrivemarketsharegainsbymonosolutions.Webelievemonowafers,whichhaveamorefavorablemolecularstructure,aremoreadaptabletomoreadvancedDWcuttingtechnology,whichincreaseswaferyieldandreducesunitpolysiliconconsumption.图表13:Globalmonopenetrationtorisefrom28%in2017to55%in2021EMarketshareofmultiandmonosolution图表14:MonowaferscontinuetoseerisingpoweroutputPoweroutputofmultiandmonowafers120%5.5100%5.080%60%4.540%4.020%3.50%201620172018201920202021MultiMono3.020112012201320142015201620172018MultiwaferpoweroutputMonowaferpoweroutput研究中国资料来源:BNEF资料来源:BNEF

图表15:Costbreakdownofwaferproduction图表16:DWcuttingenablesmonowaferstoreducepolysiliconconsumptionPer-wattpolysiliconconsumptionofmultiandmonowafers4.03.53.02.52.01.51.00.56.0(g/w)5.04.03.02.01.00.0MultiMonoPolysilicon-to-brickBrick-to-wafer(UScent/w)0.0201320142015201620172018MultiMono资料来源:BNEF资料来源:BNEF图表17:BNEFexpectDWcuttingtoenablemonowaferstoreach63picyieldper1kgbrickin2018Averagewaferyieldper1kgbrickandDWconsumptionperpic(pic/1kgbrick)64.02.562.060.058.056.054.052.02.01.51.00.550.0201720180.0Multi-waferyieldMono-waferyieldMulti-DWconsumption(RHS)Mono-DWconsumption(RHS)研究中国资料来源:BNEFnCells/modules:High-efficiencycell/dual-glasssolutionstodriveefficiency.Weexpectefficiencyimprovementtobethekeydriverofcostreductionsforcell/modules.Intheshortterm,PERC(passivatedemitterandrearcell)solutioncouldexpandmarketsharefrom12%in2017to41%in2020accordingtoBNEF.Afterthat,mainstreamsolutioncouldgraduallyshifttotheHIT(heterojunctionwithintrinsicthinlayer)andIBC(interdigitatedbackcontact)solutions.Inaddition,modulemanufacturershaveincreasedtheiradoptionofabi-facialdual-glasssolutiontoreplacethetraditionalaluminumframesandback-sheetsubstratewithPVglass.Thebi-facialcellsarethereforefullyencapsulatedinglassandcangenerateanextra10%-30%powerfromthebackside.AccordingtotheCPIA,thepenetrationofthedual-glasssolutionamongChinamodulemakerscouldrisefrom8%in2017to35%in2025.Webelievethistrendcouldeffectivelyincreasethedemandforsolarglassoverthelongterm.

图表18:High-efficiencycellstogainmarketshareoverthelongtermMarketshareofdifferenttypesofsolarcell图表19:Averageyear-endcellpoweroutputbytechnologies100%90%80%70%60%50%40%30%20%10%0%201620172018201920202021N-typemonoIBCN-typemonoHITN-typemonoPERTP-typemonoPERC/PERLP-typemonoAl-BSFP-typemultiPERCP-typemultiAl-BSF7.06.05.0Efficiency4.03.02.01.00.0(W/pic)MultiAl-BSFMultiPERCMonoAl-BSFMonoPERCN-typePERTHJT20172018资料来源:BNEF资料来源:BNEF图表20:Averagemoduleefficiencyforecast图表21:Dual-glasssolutiontogainmarketshareMarketshareofdifferentback-coversolution19.0%18.5%18.0%17.5%17.0%16.5%16.0%15.5%15.0%14.5%14.0%201320142015201620172018MonomoduleMultimdoule100%90%80%70%60%50%40%30%20%10%0%201620172018202020222025TPTbacksheetnon-TPTbacksheetGlassbacksheet研究中国资料来源:BNEF资料来源:CPIAWindcostreductiondrivenbyefficiencyimprovementsWeexpectLCOEofon-shorewindpowertofallby20%in2018-23E(13pptfromefficiencyimprovementand7pptfromcapexreduction).Weexpectturbinecosttofall3%p.a.andBOS(BalanceofSystem)toincreaseby1%p.a.asinstallationsgraduallymovefromwesternChinatoeasternandsouthernChina.Overall,weexpectunitcapexforon-shorewindpowertofall4%in2018-23.

图表22:WeexpectwindLCOEtofall20%in2018-23EOnshorewindpowerLCOE/CAPEXbreakdownandsensitivityanalysis0.070.061.20(USD/w)WeestimateLCOEtofallby20%over2018-23E,13%fromefficiencyimprovementand7%fromCAPEXreduction(USD/w)Weturbinecosttofall3%p.awhileBOStoincreaseby1%p.a.TotalCAPEXtofall4%over2018-23E1.000.800.600.050.400.040.200.030.002018EWindturbineBOS2023E研究中国CAPEX(Rmb/W)6,0476,3652,3000.300.312,4150.280.30Utilizations2,3000.300.316,7000.330.310.337,0357,3870.350.360.330.350.350.362,4150.280.300.310.330.352,5360.270.280.300.310.33CAPEX(Rmb/W)0.020.016,0476,3656,7007,0357,3872,300-10%-5%0%5%10%2,415-14%-10%-5%0%5%Utilizations2,300-10%-5%0%5%10%2,415-14%-10%-5%0%5%2,536-18%-14%-9%-5%0%02018E2023EDepreciationcostFinancialcostOPEX资料来源:GaoHuaSecuritiesResearchHowever,asdownstreamwindfarmoperatorsincreasetheadoptionoflarger-sizedandmoreefficientturbines,weexpectaverageutilizationhourstoimprovefrom2,000hoursin2018Eto2,300hoursin2023E.

OperatingenvironmentimprovingRenewableportfoliosystemandopeningupofsubsidy-freeprojectstopromoterenewableinvestmentinthelongtermTheNEApublishedtheconsultationdocumentsforarenewableenergyportfoliosysteminMarch,SeptemberandNovemberof2018.Inthelatestversionofitsconsultationdocuments,theNEAhassetaspecificminimumandanincentiverenewableenergyconsumptiontargetforeachprovinceandallowedthepurchaseofgreencertificatesasanalternativesolutiontofulfilltheRPStargets.WebelievethereinforcementofRPScouldimprovethegenerationshareofnon-hydrorenewableenergyconsumptionby3-4pptin2017-20andeffectivelypromoterenewableenergyinvestmentinChinaoverthelongterm.图表23:Renewableenergyportfoliosystemkeyinfo:setaspecificminimumandanincentiverenewableenergyconsumptiontargetforeachprovinceandallowedthepurchaseofgreencertificatesasanalternativesolutiontofulfilltheRPStargetsDraftpublishedinNov13th,2018DraftpublishedinMar23rd,2018GeneraltermSetmininumrequiredandincentivetargetsfortotalrenewableenergySettargetfortotalrenewableenergyandnon-hydroandnon-hydrorenewableenergyconsumptionineachprovinces.Therenewableenergyconsumptionineachprovinceincentivetargetwouldbesetas10%higherthanmininumrequiredtarget.EntitywithrepsonsibilityandobligationsLocalgovernmentineachprovincesshouldundertaketheimplementationresponsibilities,andpowersalescorporatesandendaccordingtorenewableresources,nationalenergyplanandconstructionstatusofcross-regionaltransmissionfacilitiesGridcompaniesineachprovinces,otherpowersalescorporates,industrialcompanieswithin-housepowerpowerusersshouldundertaketheobligationofthesystem,including:plants,andend-usersparticipatedirectpowersales1)allgridcompanies,independentpowersalescorportsandpowersalescorporateswithdistributionrights;2)enduserswhoparticipatedirectpowersalesandcorporatewithin-housepowerplants.ConnectthesystemwithpowersalesPowesalescorporatesareresponsibleforimplementingandprioritizingpowersalesrelatedtorenewableenergyAlternativesolutionsResponsbileentitiescouldseekalternativesolutionstofulfillitsshouldundertaketheobligationofthesystem.Thetargetforcorporateswithcoal-firedin-housepowerplantsshouldbehigherthanthetargetforthelocalprovince.GridcompaniesineachprovincesshouldsetimplementationplanaccordingtoRPStargetandguidethepowersalesparticipantstoprioritizetransactiononrenewableenergyandreinforceallocationofRPStargetsifmarket-basetransactioncannotensurethefulfillmentofRPStargets."Renewableenergycertificate"systemwouldberesponsiblities:1)purchaserenewableenergyfromotherentitieswhoestablishedtorecordtheproduction,consumptionexceededtheirtargests;2)voluntarilypurchaseequvalientamountofandtransactionofrenewableenergy.Eachcertificategreencertificates.MonitoringandevaluationofRPSNationalrenewableenergyinformationmanagementcommitteeareresponsibleforsetupaccountsforundertaking,evaluationandtransferofRPSinfo.BeijingpowersalesexchangeandGuangzhoupowersalesexchangeareresponsibleforimplementingcross-regionalpowersalestransaction.TreatmentofrenewableenergyexceededthetargestsFortheamountofpowerexceededincentivetargests,noextraamountofpowerwouldbeincludedinthecalaculationofRPStargerts.2018/19targetsNoevaluationwouldbemadeonthecompletionof2018Targetsand2019Targetswouldbereleasedin1Q2019.MethodologyforsettingthetargetsEnergysupervisorydepartmentsineachprovincesareresponsibleforsettingsuggestedmininumrequiedRPStargetswithsupportfromStateGridandSouthernGrid,andshouldbesubmittedforStateCouncil’sreview.StateCouncilwouldberesponsibleforpublishingfinalRPStargetsbeforetheendofMarchineveryyears.equals1Mwhofrenewableenergypower,andcertificateswouldbecategorizedintohydropowercertificateandnon-hydrorenewableenergypower.Gridcompaniesareresponsibleforcalculationofrenewableenergycertificates,marketparticipantswhocannotfulfilltheRPStargetshavetopurchaserenewableenergycertificatefromlocalgridcompanies,andtheincomewouldbeusedtosupporttheconsumptionofrenewableenergywithintheregion.Pricingofhydroandnon-hydrorenewableenergycertificatesshouldbebasedonmarket-basedtransaction.LocalgridcompaniesareresponsibleforsettingthepricingplanandsubmittingforStateCouncil’sregistration.EnergysupervisorydepartmentofStateCouncilwillberesponsibleformonitoring,evaluatingthecompletionofRPStargetsandpublishrelatedreviewreportsannually.ForprovincewhichfailedtomeetRPStargets,StateCouncilwouldsuspendorreducetheconstructionscaleoffossil-fueledpowerprojects;FormarketparticipantswhofailedtocompleteRPStargets,itsscaleofmarket-basedpowersaleswouldbereducedorevencanceled.研究中国资料来源:NEA

研究中国图表24:RPStargetsineachprovincevs.2017actualnumbersDraftpublishedinMar2018DraftpublishedinNov2018TargetfortotalrenewableenergyProvince201820202018minrequired2018incentive2020minrequired2020incentive2017Beijing11.0%13.5%11.0%12.1%15.0%16.5%12.1%Tianjing11.0%13.5%11.0%12.1%15.0%16.5%10.4%Heibei11.0%13.5%11.0%12.1%15.0%16.5%11.6%Shanxi14.0%16.0%15.0%16.3%16.5%18.0%14.1%Innermongolia14.0%16.0%18.5%20.3%18.5%20.3%19.2%Liaoning10.5%10.5%12.0%13.0%12.5%13.6%12.2%Jilin20.0%25.5%20.0%21.5%22.0%23.7%22.2%Heilongjiang18.5%24.5%19.5%21.0%26.0%28.1%20.2%Shanghai30.5%31.5%31.5%32.0%33.0%33.5%33.3%Jiangsu13.5%13.5%14.5%15.1%15.0%15.8%14.7%Zhejiang17.0%17.5%18.0%18.5%19.0%19.8%19.3%Anhui15.5%17.5%13.0%14.0%14.5%15.7%14.3%Fujian22.5%23.0%17.0%17.5%22.0%22.6%24.2%Jiangxi23.0%29.5%23.0%23.5%29.0%30.0%25.4%Shandong8.5%11.0%9.5%10.4%10.5%11.6%7.3%Henan14.0%18.5%13.5%14.5%16.0%17.1%14.6%Hubei36.0%36.5%39.0%39.9%40.0%41.0%43.0%Hunan50.5%56.5%51.5%52.4%51.5%52.4%50.4%Guangdong29.4%27.8%31.0%31.4%29.5%30.0%32.4%Guangxi50.4%44.1%51.0%51.4%50.0%50.5%51.6%Hainan10.0%11.5%11.0%11.5%11.5%12.0%13.3%Chongqing47.0%45.0%47.5%47.5%45.0%45.3%49.2%Sichuan91.0%88.5%80.0%80.4%80.0%80.4%83.5%Guizhou29.2%21.6%33.5%34.0%31.5%32.0%35.6%Yunnan80.0%70.0%80.0%81.0%80.0%81.2%85.6%Xizang59.0%68.5%nananana83.8%Shan’xi15.5%18.5%17.5%18.4%21.5%22.7%16.0%Gansu41.0%38.0%44.0%45.6%47.0%48.9%46.9%Qinhai58.5%69.0%70.0%71.9%70.0%72.5%64.9%Ningxia23.0%23.0%20.0%22.0%25.0%27.0%23.0%Xinjiang26.5%29.5%25.0%26.5%26.0%27.3%26.0%Targetfornon-hydro-renewableenergyProvince201820202018minrequired2018incentive2020minrequired2020incentive2017Beijing10.5%13.0%10.5%11.6%15.0%16.5%10.4%Tianjing10.5%13.0%10.5%11.6%15.0%16.5%10.4%Heibei10.5%13.0%10.5%11.6%15.0%16.5%10.4%Shanxi13.0%15.0%12.5%13.8%14.5%16.0%12.0%Innermongolia13.0%13.0%18.0%19.8%18.0%19.8%18.3%Liaoning9.0%9.0%10.0%11.0%10.5%11.6%9.2%Jilin16.5%20.0%15.0%16.0%16.5%18.2%16.4%Heilongjiang15.5%22.0%15.0%16.5%20.5%22.6%15.8%Shanghai2.5%3.5%2.5%2.8%3.0%3.3%2.7%Jiangsu5.5%6.5%5.5%6.1%7.5%8.3%5.4%Zhejiang5.0%6.0%5.0%5.5%7.5%8.3%4.2%Anhui11.5%14.5%9.5%10.5%11.5%12.7%8.8%Fujian5.0%7.0%4.5%5.0%6.0%6.6%4.5%Jiangxi6.5%14.5%6.5%7.2%8.0%8.8%6.5%Shandong8.0%10.5%9.0%9.9%10.5%11.6%6.9%Henan8.0%13.5%9.0%9.9%10.5%11.6%8.1%Hubei7.5%11.0%7.5%8.3%10.0%11.0%6.8%Hunan9.0%19.0%9.0%9.9%13.0%14.3%7.2%Guangdong3.0%3.8%3.5%3.9%4.0%4.4%3.2%Guangxi3.0%5.0%4.0%4.4%5.0%5.5%3.0%Hainan4.0%5.0%4.5%5.0%5.0%5.5%4.7%Chongqing3.0%3.5%2.0%2.2%2.5%2.8%2.4%Sichuan4.5%4.5%3.5%3.9%3.5%3.9%3.3%Guizhou4.0%4.8%4.5%5.0%5.0%5.5%4.3%Yunnan10.0%10.0%11.5%12.7%11.5%12.7%14.2%Xizang13.5%17.5%nananana14.0%Shan’xi8.5%11.5%9.0%9.9%12.0%13.2%7.7%Gansu15.0%15.0%15.5%17.1%19.0%20.9%13.8%Qinhai21.0%25.5%19.0%20.9%25.0%27.5%18.5%Ningxia21.0%21.5%18.0%19.8%20.0%22.0%21.0%Xinjiang14.5%14.5%14.5%16.0%16.0%17.6%13.1%资料来源:NEA

InSeptember,theNEApublishedaconsultationdocumentregardingthepromotionofgrid-parityforwindandsolarpower,statingthatlocalauthoritiesineachprovincecouldgrantquotasforsubsidy-freewind/solarprojectsbasedonlocalwind/solarresourceswithouttheNEA’sapproval.Webelievethisisaremarkablesteptowardopeningupthequotaforsubsidy-freeprojects.PowerdemandinChinacouldremainresilientin2019andbeyonddespiteapotentialeconomicslowdownPowerdemandinChinapostedstronggrowthin10M18,up8.7%yoy.Webelievethemajordriversofthiswerestrongpowerdemandfromtheresidential(up11.1%YTD)andtertiarysectors(up13.1%YTD).图表25:Chinapowerconsumptionup8.69%in10M18PowerconsumptionbysectorinChina图表26:Powerdemandfromsoftwareandinternetservicessectorssawstronggrowthin10M1810M2018top10sectorpowerdemand700,000600,000500,000400,000300,000200,000100,000012(GWh)(%)1086420Jan-FebMar-18Apr-18May-18Jun-18Jul-18Aug-18Sep-18Oct-182018Roadtransportation(%)LivestockhusbandryPetro,coalandotherfuelprocessingOtherconstructionanddecotrationMetalproductmanufacturingPipelinetransportationWasteresourcerecyclingOtherminingInternetandrelatedserviceResidentialTertiaryindustrySecondaryindustryPreliminaryindustryYoYtotalpowerconsumptiongrowth(RHS)SoftwareandITservices01020304050607080研究中国资料来源:CEC资料来源:CECTheGSMacroResearchteamforecastsrealGDPgrowthof6.2%/6.1%in2019/20E,downfrom6.6%in2018and6.9%in2017.WeexpectChinapowerdemandtoremainrelativelyresilientin2019andbeyonddespiteapotentialeconomicslowdownduetothefollowingreasons:nWeexpectdemandfromthetertiarysectortocontinuetogrowaswebelievethekeysub-sectorswithstrongpowerdemandgrowth(suchasdatacenterservicesandcloudcomputing,etc.)shouldbemoreimmunetoeconomicvolatility.nWeforecastresidentialdemandtoremainstrongonincreasedelectrificationandthespreadofpower-intensivebehaviors(suchasusinghomeappliancesanddrivingelectricvehicles).nAhighersectorconcentrationratioinenergy-intensivesectors,asaresultofsupply-sidereform,wouldenableleadingplayerstomaintainrelativelyhighutilizationandsupportunderlyingdemandforpowerduringaneconomicslowdown.

研究中国Risingeconomicstodriveinstallations;competitionremainsfierce;leadersstandingoutamidsectorconsolidationWeforecastrapidlydeclininggenerationcostsandanimprovingoperatingenvironmenttodrive150GW/256GWofwind/solarinstallationsin2018-23EwithatotalofRmb1,083bn/Rmb1,040bnincapexinvestment.图表27:WeexpectChinatoadd150/256GWofwind/solarinstallationin2018-23EOursolarandwindinstallationforecastsforChinaWind2017A2018E2019E2020E2021E2022E2023EGenerationBnkwh305.7357.2413.5476.9545.9618.6699.6AccumulatedCapacityGW163.7185.7208.7233.7259.7285.7313.7NewadditionGW15.022.023.025.026.026.028.0CAPEXBnRmb165.0170.2182.5187.2184.6193.2Solar2017A2018E2019E2020E2021E2022E2023EGenerationBnkwh118.2167.3216.0271.5337.2408.7493.0AccumulatedCapacityGW130.3167.3205.8246.3291.3336.3386.3Newaddition-ChinaGW52.837.038.540.545.045.050.0Newaddition-GlobalGW98.888.298.5106.2112.2117.3150.0CAPEXBnRmb167167170185171180资料来源:NEA,GaoHuaSecuritiesResearchWeexpectthegenerationshareofwindandsolarpowertoreach15%in2023E,upfrom7%in2017.图表28:Weexpectthegenerationshareofwindandsolarpowertoreach15%by2023EGenerationmixbypowersource100%90%80%70%60%50%40%30%20%10%0%20172018E2019E2020E2021E2022E2023EThermalHydroWindNuclearSolar资料来源:CEC,GaoHuaSecuritiesResearchAsupstreammanufacturersarevigorouslyexpandingcapacitytoprepareforthegrid-parityera,weexpectupstreamcompetitiontoremainfierce,especiallyinsolar.Weforecasttotalpolysilicon/wafer/modulecapacitytorise43%/18%/9%in2018and22%/17%/12%in2019.Weexpecttheconsolidationinupstreammanufacturingtocontinue,withdivergent

cost-cuttingcapabilities,andweexpectupstreamleaderswith

R&Dandexecutionstrengthtostandout,anddownstreamleaderswithoutstandingoperatingefficiencyandstrongbalancesheetsshouldalsobenefitfromcostreductionsintheupstreamvaluechain.图表29:Capacityexpansionplanofleadingsolarproductmanufacturers600,000500,000400,000300,000200,000100,00002015201620172018E2019ESilicon(tonnes)Wafer(MW)Module(MW)资料来源:Companydata,GaoHuaSecuritiesResearch图表30:WeexpectleaderswithcostadvantagetogainmarketshareamidconsolidationMarketshareofleadingsolarandwindproductmanufacturers图表31:WeexpectdownstreamleaderstoexpandEBITmarginsEBITmarginofleadingdownstreamsolarandwindoperators35%60%25%30%25%20%15%10%5%55%50%45%40%35%20%15%10%5%0%201620172018E2019E2020ELongiSungrowGoldwind30%0%201620172018E2019E2020ELongyuanHNRChint(RHS)Note:GlobalmarketshareforLongiandSungrow,ChinamarketshareforGoldwind资料来源:Companydata,GaoHuaSecuritiesResearch研究中国资料来源:Companydata,GaoHuaSecuritiesResearch

Valuation:Attractiverisk/rewardprofiledespiteshort-termpolicyuncertaintiesWeinitiatecoverageoneightwindandsolarnamesChina’ssolar/windsectorsaretradingatone-yearforwardP/Esof10.7x/6.5xandP/Bsof1.8x/0.9x,belowtheiraveragesoverthepastthreeyears(averageP/E:13.1x/9.7x;averageP/B:2.2x/1.1x).Weviewthecurrentrisk-rewardprofileasattractivedespiteshort-termpolicyuncertainties.图表32:SolarsectorrollingP/E图表33:SolarsectorrollingP/BMax:23x20Max:13x1510Max:9x50255.04.54.03.53.02.52.01.51.00.50.0MAx:4.4xAve:2.2xMin:1.6xNote:MarketcapweightedaverageofLongi/Sungrow/Tongwei/Xinyi/ChintMarketcapweightedaverageofLongi/Sungrow/Tongwei/Xinyi/Chint资料来源:Wind,GaoHuaSecuritiesResearch资料来源:Wind,GaoHuaSecuritiesResearch图表34:WindsectorrollingP/E图表35:WindsectorrollingP/BMax:20x2015Max:13x10Max:8x50251.81.61.41.2Ave:1.6xAve:1.1x1.00.80.60.40.20.0Min:0.7x研究中国MarketcapweightedaverageofLongyuan/HNR/GoldwindMarketcapweightedaverageofLongyuan/HNR/Goldwind资料来源:Wind,GaoHuaSecuritiesResearch资料来源:Wind,GaoHuaSecuritiesResearchInthewindsegment,weinitiatecoverageofHNRandGoldwind-HatBuyandGoldwind-AandLongyuanatNeutral.Insolar,weinitiatecoverageofLongi,TongweiandZhejiangChintatBuy,SungrowatNeutralandXinyiatSell.

研究中国图表36:CoveragesummaryLongiChintTongweiSungrowXinyi601012.SS601877.SS600438.SS300274.SZ0968.HK2018EV/EBITDA15.410.111.19.29.72019EV/EBITDA11.78.07.57.18.4Historicalaverage14.110.69.419.112.7Histroricalmean12.69.78.718.610.0Peer’saverage16.710.410.28.67.4Peer’s18-20EBITDAcagr22%17%13%8%11%Company18-20EEBITDAcagr31%25%35%26%18%2019EEBITDA4,3876,7815,0921,5683,6172019ENetdebt(1,100)2,6764,091(2,614)6,718TargetmultipleBenchmark16.510.510.2Historicalaverageof8.5peergroup7.4Targetprice26.332.312.311.02.6CurrentPrice18.223.58.79.22.9PricecurrencyCNYCNYCNYCNYHKDUpside45%38%42%19%-8%RatingBUYBUYBUYNeutralSellImplied2019P/E23.014.815.715.38.6Implied2020P/E16.611.312.011.77.4Historicalmedianlevel(2013-18)23.316.523.4188.9LongyuanHNRGoldwind-HGoldwind-A0916.HK0958.HK2208.HK002202.SZ2018EV/EBITDA6.26.210.614.32019EV/EBITDA5.65.98.511.4Historicalaverage7.37.410.715.0Histroricalmean7.47.410.714.6Peer’saverage8.08.010.210.2Peer’s18-20EBITDAcagr5%5%15%15%Company18-20EEBITDAcagr6%6%29%29%2019EEBITDA17,97410,8135,3405,3402019ENetdebt58,94142,31920,52420,524Targetmultiple5.76.510.012.31stdbelowhistorical0.5stdbelowhistoricalHistoricalaverageof1stbelowBenchmarkaverageaveragepeergrouphistoricalaverageTargetprice6.13.010.412.7CurrentPrice5.42.17.610.8PricecurrencyHKDHKDHKDCNYUpside13%42%37%18%RatingNeutralBUYBUYNeutralImplied2019P/E9.48.18.810.8Implied2020P/E8.47.17.18.7Historicalmedianlevel(2013-18)13.18.49.312.9资料来源:Companydata,GaoHuaSecuritiesResearchExcludingLongiandZhejiangChint,our2018estimatesare0%-6%belowconsensus,our2019estimatesarebroadlyinlinewithconsensus,andour2020estimatesare0%-20%above(exceptforLongyuan).

研究中国图表37:Our2020estimatesare2%-20%aboveconsensusGHnetincomeestimatevs.consensusRating2018E(Rmb/HKDmn)GHestimate2019E(Rmb/HKDmn)2020E(Rmb/HKDmn)VS2018Econsensus2019E2020EGoldwind-ANeutral3,3864,1985,202-6%-1%5%Goldwind-HBuy3,3864,1985,202-6%-1%5%LongyuanNeutral4,7535,2535,861-2%-3%-1%HNRBuy3,5793,8794,4380%-1%2%LongiBuy2,5373,1984,4191%7%20%SungrowNeutral8641,0411,365-4%-4%3%XinyiSell1,9732,3192,720-4%-1%2%ChintBuy3,7114,6326,0681%6%16%TongweiBuy1,8883,0483,997-5%3%11%ThereportingcurrencyforXinyiisHKD,allothersareCNY资料来源:Companydata,Wind,Bloomberg,GaoHuaSecuritiesResearchWeadoptEV/EBITDAastheprimaryvaluationmethodologyforoursolarandwindcoverageaswehavefoundthathistoricalmultiplesarehighlyco-relatedtoEBITDAgrowth,givingusareliableandmeasurablebenchmarkacrossthesectors.Weselectthecomparablepeergroupasavaluationreferencebasedonthenatureofeachcompany’sbusiness.Weapplytheaveragehistoricalmultipleofthepeergrouptoourcoverage(exceptforLongyuan,HNRandGoldwind-A).ForLongyuanandHNR,weapplymultiplesthatare-1std/0.5stbelowthehistoricalaveragestoreflectthede-ratingsincethebeginningof2018duetoinvestorconcernsonsubsidypaymentandutilization.WehavereflectedourmorepositiveviewsinourestimatesforthetwocompaniesaswebelievetheseissuescouldimprovegraduallyasRPSisreinforced.Weapply1stdbelowthehistoricalaveragetoGoldwind-Aasithasbeentradingatanaverage47%premiumoverGoldwind-H,whichweattributetodifferingperceptionsonthewindinstallationoutlookamongon-shoreandoffshoreinvestors.

研究中国图表38:SummaryofourvaluationframeworkUpside/ValuationTargetCompanyRatingPricetargetdownsidemethodologymultipleBenchmarkRationale(%)(x)SolarLongiBuy26.3Rmb/sh45%EV/EBITDA16.5HistoricalaverageLongi’scurrentEV/EBITDAwasslightlyhigherthantheaverageofpast5-yearrange,butofpeergrouplowerthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.ChintBuy32.3Rmb/sh38%EV/EBITDA10.5HistoricalaverageChint’scurrentEV/EBITDAwasbelowaverageofitspast5-yearrange,andalsolowerofpeergroupthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.TongweiBuy12.3Rmb/sh42%EV/EBITDA10.2HistoricalaverageTongwei’scurrentEV/EBITDAislowerthanaverageofitspast5-yearrange,andalsoofpeergrouplowerthanhistoricalaverageofcomparablepeergroup.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.SungrowNeutral11.0Rmb/sh19%EV/EBITDA8.5HistoricalaverageSungrow’scurrentEV/EBITDAislowerthanaverageofpast5-yrrangeandcomparableofpeergrouppeer’spast5-yraverage.Withasector-leadinggrowthoutlook,weexpectthecompanytotradeuptoaverageofcomparablepeersgroup.XinyiSell2.6HKD/sh-8%EV/EBITDA7.4HistoricalaverageXinyi’scurrentEV/EBITDAislowerthanhistoricalaverage,buthigherthancomparableWindofpeergrouppeershistoricalaverage.AlthoughwebelieveXinyioperateswithmorediversifiedbusinessandbetterprofitabilities□andgrowthoutlookagainstitspeers.Webelieveitsvaluationpremium□isunjustifiedasmostofourpreferredpicksaretrading□atbelowaveragemultipleofpeersgroup.HNRBuy3.0HKD/sh42%EV/EBITDA6.5-0.5stdofhistoricalHNR’scurrentEV/EBITDAwaslowerthanaverageofpast3-yrrangeandcomparableaveragepeershistoricalaverage.Sincethebeginningof2018,HNRhasbeentradingbetweenpast3-yraverageand1stdbelowaverage.Itappearsthereisade-ratingin2018comparedtotheaverageof2016/17,duetoinvestors’concernonsubsidypaymentandutilization.Wehavediscountedourmorepositiveviewinourestimates,andadopt0.5stdbelowhistoricalaverage(medianofYTDrange)astargetmultiple.Goldwind-HBuy10.4HKD/sh37%EV/EBITDA10.0HistoricalaverageGoldwind-H’scurrentEV/EBITDAislowerthantheaverageofpast5-yrrange,alsolowerofpeergroupthanhistoricalaverageofpeergroup.Withagrowthoutlookhigherthansectoraverage,weexpectthecompanytotradeuptohistoricalaverageofpeergroup.LongyuanNeutral6.1HKD/sh13%EV/EBITDA5.7-1stdofhistroicalLongyuan’scurrentEV/EBITDAwaslowerthanaverageofpast3-yrrangeandaveragecomparablepeershistoricalaverage.Sincethebeginningof2018,Longyuanhasbeentradingbetweenpast3-yraverageand1stdbelowaverage.Itappearsthereisade-ratingin2018comparedtotheaverageof2016/17,duetoinvestors’concernonsubsidypaymentandutilization.Wehavediscountedourmorepositiveviewinourestimates,andadopt1stdbelowhistoricalaverage(0.5stdbelowHNR’stargetmultipleonlowerEBITDAgrowthoutlook)astargetmultiple.Goldwind-ANeutral12.7Rmb/sh18%EV/EBITDA12.3-1stdofhistoricalGoldwind-A’scurrentEV/EBITDAislowerthanaverageofpast5-yrrange.Goldwind’sA-averagesharehas47%averagepremiumoverH-sharesincethebeginningof2013.Webelievethisisduetodifferentperceptionofwindinstallationoutlookfromon-shoreandoff-shoreinvestors.Weapply1stdbelowhistoricalaverageastargetmutiple.资料来源:GaoHuaSecuritiesResearch

研究中国图表39:ValuationtableTickerCompanyMktCapUSDMnPriceLoccurEVLoccur2018P/E201920202018P/B201920202018ROE20192020Gearning20172018EV/EBITDA20192020Windmanufacturer2208HKEquityXINJIANGGOLD-H5,143.177.5554,9737.96.45.21.10.90.814.115.717.260.010.68.56.9002202CHEquityXINJIANGGOLD-A5,135.8010.7049,79711.29.17.31.51.31.214.115.717.280.614.311.49.1VWSEUEquityVESTASWINDSYST16,071.95514.009,87716.815.510.84.74.64.227.229.239.2(107.9)8.37.35.8SGRESMEquitySIEMENSGAMESAR9,896.5212.806,91119.016.413.91.41.41.5(1.6)0.44.4(10.4)9.18.57.8NDX1EUEquityNORDEXSE952.238.65962nana18.11.01.11.0(8.7)(6.6)5.711.112.89.85.4Average13.711.811.11.91.91.79.010.916.7Median11.29.113.91.41.31.214.115.717.2Windoperator916HKEquityCHINALONGYUAN-H5,606.405.45121,9859.28.37.51.00.90.811.011.211.4136.26.86.35.7958HKEquityHUANENGRENEWA-H2,894.502.1473,0476.35.85.10.80.70.713.713.213.5192.16.25.94.81798HKEquityCHINADATANGC-H949.691.0257,1465.84.94.30.60.50.511.211.711.9324.07.97.26.7EDPREUEquityEDPRENOVAVEISS7,564.807.6410,48626.227.126.21.01.01.04.03.83.836.18.78.78.5Average11.811.510.70.90.80.710.010.010.2Median7.87.16.30.90.80.711.111.411.6Wind-Average12.811.610.91.41.31.29.510.413.4Wind-Median9.58.110.11.11.11.012.613.614.4Polysilicon600438CHEquityTONGWEICO-A4,897.158.7050,62417.911.18.42.21.91.613.318.520.323.711.17.55.8DQUSEquityDAQONEWENE-ADR313.4924.378045.24.73.00.50.50.410.79.615.039.86.55.63.7600089CHEquityTBEACOLTD-A3,716.016.9059,43711.310.28.80.80.70.77.57.88.648.612.010.79.1Average11.58.76.81.21.00.910.512.014.7Median11.310.28.40.80.70.710.79.615.0Wafer601012CHEquityLONGIGREENEN-A7,339.9118.1476,76120.015.811.53.02.52.016.217.019.328.415.411.78.13800HKEquityGCL-POLYENERGY1,137.970.4973,29413.98.26.30.40.40.42.14.15.2172.48.37.46.8002129CHEquityTIANJINZHONG-A2,830.717.0142,43773.850.114.3nanana3.75.49.377.6nananaAverage35.924.710.71.71.41.27.38.811.3Median20.015.811.51.71.41.23.75.49.3Cell/ModuleJKSUSEquityJINKOSOLAR-ADR437.2211.1515,5065.915.615.41.51.51.56.11.71.7154.55.76.97.1CSIQUSEquityCANADIANSOLARI937.8916.013,5135.58.914.50.80.80.715.68.75.1235.95.86.27.1FSLRUSEquityFIRSTSOLARINC4,406.4242.044,03429.616.312.50.90.8na2.95.06.1(59.2)16.68.35.9SPWRUSEquitySUNPOWERCORP816.885.792,460nananananana(855.7)(31.8)(38.3)443.520.08.27.7Average8.314.413.11.11.01.1(207.8)(4.1)(6.4)Median5.716.013.50.90.81.14.53.33.4Inverter300274CHEquitySUNGROWPOWER-A2,003.489.5227,60216.013.310.11.81.61.411.812.814.813.99.27.15.1002518CHEquitySHENZHENKSTAR-A695.008.238,59812.310.58.61.91.71.414.815.317.3(38.9)21.419.213.3SEDGUSEquitySOLAREDGETECHNO1,711.5737.411,30211.519.634.13.83.63.537.019.811.2(86.4)10.318.531.8Average13.314.517.62.52.32.121.216.014.4Median14.211.99.41.91.61.413.314.016.0PVGlass968HKEquityXINYISOLARHLDS2,823.772.8828,49311.29.58.12.01.81.618.519.620.656.19.78.46.96865HKEquityFLATGLASSGRO-H493.072.142,93810.37.46.41.11.00.910.714.214.213.83.62.52.0Average10.88.47.21.51.41.214.616.917.4Median10.88.47.21.51.41.214.616.917.4EPC/Solarfarmoperator601877CHEquityZHEJIANGCHINT-A7,345.8323.5564,19013.410.88.22.11.81.517.018.120.037.810.18.06.1451HKEquityGCLNEWENERGY708.040.2943,0986.45.65.60.70.60.511.711.810.5375.88.87.97.81250HKEquityBJENTCLEAN837.550.1017,0124.54.33.70.80.60.517.914.610.035.06.14.64.1RUNUSEquitySUNRUNINC1,466.3913.111,97055.614.213.71.82.85.6(38.2)(45.0)(73.3)66.6nana74.4PEGIUSEquityPATTERNENER-A1,910.9119.485,17113.0nana1.71.92.113.4(0.0)1.177.313.713.112.8AverageMedian18.613.08.75.67.88.21.41.71.51.82.11.54.413.4(0.1)11.8(6.3)10.0Solar-average16.413.210.51.61.41.4(25.0)8.27.5Solar-Median12.111.08.91.61.41.212.010.712.5资料来源:Bloomberg,Wind,GaoHuaSecuritiesResearch

研究中国RisksDisappointingFiTpoliciesin2019.Althoughwebelievesolarandwindpoweraregraduallymovingfromasubsidy-driventoacost-drivenmodel,currentprojectreturnsofsolarandwindpowerstillrelyonsubsidies.DisappointingFiTpolicieswouldreducetheprojectedreturnofsolarandwindpowerandhurtunderlyingdemandintheshortterm.Disappointingpolicyonsolarprojectquotain2019.Althoughwebelievesolarandwindpoweraregraduallymovingfromasubsidy-driventocost-drivenmodel,mostsolarandwindpowerprojectsneedgovernmentapprovaltogetconnectedtothegrid.Assuch,iftheNEApublishesadisappointingpolicyonprojectquotasin2019,underlyinginstallationanddemandwouldbesubstantiallyimpacted.DisappointingRPSpolicy.TheNEAhaspublishedthreeversionsofconsultationdocumentsforRPS,andthefinalversioncoulddifferfromthelatestconsultationdocument.IftheRPSpolicyturnsouttobedisappointing,webelievesentimentforrenewableenergyinvestmentinChinawouldbehurt.Over-supplyfromupstreamsolarproductmanufacturers.Ifupstreamsolarproductmanufacturersexpandcapacitymorethanexpected,over-supplyinupstreammanufacturingwouldincreasecompetitionwithinthesectorandhurttheprofitabilityofrelatedmanufacturers.

研究中国COMPANYANALYSIS

研究中国LongiGreen(601012.SS):Drivingglobalmonopenetration;initiateatBuyLongiisthelargestmonowaferandmodulemakerintheworldwithcapacitiesof15GWforwafersand6.5GWformodulesasofend-2017.Webelieveitskeyadvantageliesinitssector-leadingR&Dandexecutioncapabilities,whichhavedrivencontinuouscostreductionandrapidcapacityexpansion.Over2012-17,Longisuccessfullygrewitswafershipmentsfrom826MWto10.7GWwhileitsglobalmarketshareexpandedto11%from3%.Rapidcapacityexpansionandhigh-efficiencyproductofferingstodriveglobalshare.WeexpectLongi,throughanaggressivecapacityexpansionandpricingstrategy,torecordCAGRsof47%/46%foritswafer/moduleexternalshipmentsin2018-20.Withwafer/moduleASPsdecliningby35%/22%in2018,9%/7%in2019and5%/5%in2020onourestimates,weexpectLongitorecordCAGRsof18%/38%forwafer/modulerevenuein2018-20.LeadingR&Dstrengthtodrivecost-reduction.WeestimatethatLongi,byleveragingitssector-leadingR&Dcapability,reducednon-siliconcostforitswafersby78%in2012-17,anditsproductioncostformodulesby36%in2015-17.In2018-20,weexpectcontinuedefficiencyimprovementstodrivefurther22%and21%reductionsinitswafer’snon-siliconcostanditsmodule’sprocessingcost.Asaresultof35%and22%ASPdeclineforwafers/modulesin2018,weexpectgrossmarginforLongi’swaferandmodulestodeclinefrom32.7%/30.7%in2017to13.2%/20.6%in2018,butgraduallyrecoverto15.8%/21.1%in2019and15.8%/21.4%in2020ascostreductionscatchup.Drivingglobalmonopenetration:WeexpectLongitorecorda32%netincomeCAGRin2018-20.WelikeLongi’ssector-leadingR&DandexecutioncapabilitiesandexpectLongitofurtherdriveglobalshareonrapidcapacityexpansionandcontinuedcostreductions.Giventhesepositives,andwith45%upsidetoour12-monthtargetpriceofRmb26.3,weinitiatecoverageonLongiatBuy.

研究中国图表40:FinancialsummaryProfitmodel(Rmbmn)12/1712/18E12/19E12/20ETotalrevenue16,362.322,775.527,709.538,409.3Costofgoodssold(11,081.8)(18,346.0)(22,050.5)(30,381.9)SG&A(1,328.7)(1,776.5)(2,161.3)(2,995.9)R&D--------Otheroperatingprofit/(expense)(151.6)(136.5)(122.8)(122.8)EBITDA4,394.83,297.74,386.66,175.8Depreciation&amortization(594.6)(781.2)(1,011.8)(1,267.1)EBIT3,800.12,516.53,374.84,908.7Interestincome75.775.791.6101.1Interestexpense(270.0)(338.2)(435.4)(513.0)Income/(loss)fromuncons.subs.--------Others411.9650.0650.0650.0Pretaxprofits4,017.72,904.03,680.95,146.7Incometax(468.3)(377.5)(496.9)(746.3)Minorities15.110.813.618.8Netincomepre-preferred3,564.52,537.23,197.64,419.2Preferreddividends--------Netincome(pre-exceptionals)3,564.52,537.23,197.64,419.2Posttaxexceptionals--------Netincome3,564.52,537.23,197.64,419.2EPS(basic,pre-except)(Rmb)1.280.911.151.58EPS(basic,post-except)(Rmb)1.280.911.151.58EPS(diluted,post-except)(Rmb)1.280.911.151.58DPS(Rmb)0.180.090.110.16Dividendpayoutratio(%)14.110.010.010.0Freecashflowyield(%)(6.2)(0.1)(0.7)2.7Growth&margins(%)12/1712/18E12/19E12/20ESalesgrowth41.939.221.738.6EBITDAgrowth77.0(25.0)33.040.8EBITgrowth76.7(33.8)34.145.5Netincomegrowth130.4(28.8)26.038.2EPSgrowth130.4(28.8)26.038.2Grossmargin32.319.420.420.9EBITDAmargin26.914.515.816.1EBITmargin23.211.012.212.8Cashflowstatement(Rmbmn)12/1712/18E12/19E12/20ENetincomepre-preferreddividends3,564.52,537.23,197.64,419.2D&Aadd-back594.6781.21,011.81,267.1Minoritiesinterestsadd-back(15.1)(10.8)(13.6)(18.8)Net(inc)/decworkingcapital808.0642.9(64.1)746.9Otheroperatingcashflow(3,710.1)------Cashflowfromoperations1,241.93,950.54,131.76,414.5Capitalexpenditures(3,945.2)(4,000.0)(4,500.0)(5,000.0)Acquisitions--------Divestitures--------Others171.1------Cashflowfrominvestments(3,774.0)(4,000.0)(4,500.0)(5,000.0)Dividendspaid(common&pref)(199.6)(358.9)(253.7)(319.8)Inc/(dec)indebt3,576.52,200.01,700.01,200.0Commonstockissuance(repurchase)198.6------Otherfinancingcashflows1,686.1------Cashflowfromfinancing5,261.61,841.11,446.3880.2Totalcashflow2,729.51,791.61,078.02,294.7Balancesheet(Rmbmn)12/1712/18E12/19E12/20ECash&equivalents8,546.010,337.711,415.613,710.4Accountsreceivable6,131.38,611.010,248.713,153.9Inventory2,380.43,970.84,530.95,826.7Othercurrentassets1,869.61,869.61,869.61,869.6Totalcurrentassets18,927.424,789.128,064.934,560.5NetPP&E10,803.514,031.917,529.621,277.5Netintangibles212.9203.4193.9178.9Totalinvestments515.2515.2515.2515.2Otherlong-termassets2,424.73,142.53,650.04,289.5Totalassets32,883.742,682.049,953.560,821.6Accountspayable7,350.212,063.114,196.919,144.8Short-termloans1,611.81,811.82,011.82,211.8Othercurrentliabilities3,378.13,378.13,378.13,378.1Totalcurrentliabilities12,340.117,253.119,586.824,734.7Long-termdebt4,804.06,804.08,304.09,304.0Otherlong-termliabilities1,495.51,495.51,495.51,495.5Totallong-termliabilities6,299.48,299.49,799.410,799.4Totalliabilities18,639.625,552.529,386.335,534.1Preferredshares--------Totalcommonequity14,195.417,091.520,542.825,281.7Minorityinterest48.838.024.45.7Totalliabilities&equity32,883.742,682.049,953.560,821.6BVPS(Rmb)5.096.127.369.06Ratios12/1712/18E12/19E12/20ECROCI(%)5.422.122.525.4ROE(%)29.416.217.019.3ROA(%)13.76.76.98.0Inventorydays59.263.270.462.2Receivablesdays111.1118.1124.2111.2Payabledays171.7193.1217.3200.3Netdebt/equity(%)(15.0)(10.1)(5.3)(8.7)Interestcover-EBIT(X)19.69.69.811.9Valuation12/1712/18E12/19E12/20EP/Ebasic(X)12.220.716.411.9P/B(X)3.13.12.62.1EV/EBITDA(X)9.415.411.78.1EV/GCI(X)2.92.92.32.0Dividendyield(%)1.20.50.60.8Note:Lastactualyearmayincludereportedandestimateddata.Source:Companydata,GoldmanSachsResearchestimates.资料来源:Companydata,GaoHuaSecuritiesResearch

Theworld’slargestmakerofmonowafersandmodulesIncorporatedin2010,Longiistheworld’slargestmakerofmonowafersandmoduleswith15GWofwaferand6.5GWofmodulecapacityasofend-2017.In2017,wafers/modulescontributed35%/56%ofLongi’srevenue,withgrossmarginsof33%/31%.WebelieveLongi’skeyadvantagesare:1)itssector-leadingR&Dandexecutioncapability,whichhavedrivencontinuedcostreductionsandrapidcapacityexpansion;2)anintegratedbusinessmodelcoveringhigh-efficiencywafer,cellandmodulemanufacturing,whichhasallowedthecompanytopromoteitsground-breakingmonosolutiondirectlytoend-users.In2012-17,Longigrewitswafershipmentsto10.7GWfrom826MW,aCAGRof67%,whileitsglobalmarketshareexpandedto11%from3%;atthesametime,grossmarginofthewafersegmentrosefrom13%to33%.图表41:Longi’swafershipmentsrecordedaCAGRof67%in2012-17Historicalwafer/modulecapacityandshipment图表42:HistoricalrevenuebysegmentandYoYgrowthfortotalrevenue70,00060,00050,00040,00030,00020,00010,00002012201320142015201620172018E2019E2020E12%(MW)10%8%6%4%2%0%45,00040,00035,00030,00025,00020,00015,00010,0005,0000(Rmbmn)2015201620172018E2019E2020E100%90%80%70%60%50%40%30%20%10%0%WafercapacityModulecapacityWafershipmenModuleshipmentGlobalmarketshare(RHS)WaferModuleCellSolarpowerOtherYoYgrowth(RHS)资料来源:Companydata,GaoHuaSecuritiesResearch资料来源:Companydata,GaoHuaSecuritiesResearch图表43:Grossmarginbysegment图表44:HistoricalEBIT,EBITmarginandR&DexpasapercentageofrevenueHistoricalEBIT,EBITmarginandR&Dexpasa%ofrev40%35%30%25%20%15%10%5%0%2015201620172018E2019E2020EBlendedWaferModule55004500350025001500500-500EBITEBITmarginR&Dexpas%ofrev25%(Rmbmn)2015201620172018E2019E2020E20%15%10%5%0%研究中国资料来源:Companydata,GaoHuaSecuritiesResearch资料来源:Companydata,GaoHuaSecuritiesResearch

图表45:Longi’smarketshareexpandedto11%in2017from3%in2012Productionvolumeofleadingwafermakers(2017)(MW)30,00012%25,00010%20,0008%15,0006%10,0004%5,0002%-0%201220132014201520162017CanadianSolarZhonghuanJinkoSolarLongiGCLLongi’smarketshare(RHS)资料来源:CompanydataRapidcapacityexpansionandhigh-efficiencymonosolutionstodriveglobalshareWebelieveLongiisnotjustbest-positionedtorideonrisingglobalmonopenetration,butcouldalsobethekeydriverofthechange.Accordingtoitsstrategicplanfor2018-20,Longiisaimingtoexpandmonowafercapacityfrom15GWbyend-2017to28GWbyend-2018,36GWbyend-2019and45GWbyend-2020.Inaddition,Longitargetsareductioninthenon-siliconcostofitswaferstolessthanRmb1/pic,andcouldsupport22.5%conversionefficiencyforPERCcellproductswithlessthan1%ofLID.图表46:Capacityofleadingwafermakers(2017)Capacityofleadingwafermakers(2017)图表47:Longiaimstobuild45GWofwafercapacitybyend-2020CapacityexpansionplanofleadingwafermakersGCLLongiJinkoSolarZhonghuanCanadianSolarLDKJASolarYingliGreenEnergyReneSola(wafer)TrinaNanBoSFCE(SuntechPower)SolargigaEnergy05,00010,00015,00020,00025,00030,00035,00050,00045,00040,00035,00030,00025,00020,00015,00010,0005,0000201620172018E2019E2020ECanadianSolarJinkoSolarZhonghuanGCLLongi研究中国资料来源:Companydata,PVinsight资料来源:Companydata,PVinsight,GaoHuaSecuritiesResearchWebelieveLongicouldusethiscapacityexpansiontocapturethegrowth

opportunityfromoverseasmarketsandfurtherdriveglobalmarketshareonthebackofahigh-efficiencymonosolution.Longi’sglobalsharewasc.11%in2017,and74%ofits

revenueisderivedfromtheChinamarket.SinceLongibeganaddingcapacityaggressivelyin2015andsuccessfullyrolledoutground-breakinghigh-efficiencymonomoduleswithrecordlowLIDfeaturesinthesameyear,Longi’sMOP-typemoduleproductshaveconsistentlydeliveredbettergenerationperformancethanregularmulti-modules.Asaresultofthissector-leadingcostperformance,Longi’swafershipmentsgrewto10.7GWfrom2.7GWanditsmoduleshipmentsgrewto4.7GWfrom821MWin2015-17.Asaresultofitsrobustshipments,LongiChina’slargestmakerofmonoproductsdroveglobalmonopenetrationfrom20%in2016to28%in2017.图表48:Longihasconsistentlyrolledoutground-breakinghigh-efficiencymodulesBi-facialmonomodule-LR6-72BP(355-370W)-LR6-60BP(290-310W)PERCmonomodule-LR6-72PE(355-370W)-LR6-60PE(295-310W)Regularmonomodule-LR6-72(335-345W)-LR6-60(280-295W)25yearpowerwarrantyannualpowerattenuation:0.55%Longi’smonomoduleofferings资料来源:Companydata图表49:Longi’shigh-efficiencymoduleoffersbettergenerationperformanceGenerationperformanceofLongiHi-MO1P-typemoduleandregularmultimodule图表50:Globalmonopenetration2,500(Kwh/year)2.5%120%2,0002.0%100%1,5001.5%80%60%1,0001.0%40%5000.5%20%0DatongCologneRiyadhLosangelasChennaiHi-MO1MultimodulesGenerationpremium(RHS)0.0%0%201620172018201920202021MultiMono

研究中国资料来源:Companydata资料来源:BNEF

图表51:Chinasalesaccountedfor74%andutilizationcloseto100%in2017Revenuebreakdown,waferandmoduleutilizationandsales-to-productionratio(Rmbmn)74%79%71%18,000100%16,00014,00012,00010,0008,0006,0004,0002,00090%80%70%60%50%40%30%20%10%研究中国00%201520162017ChinaAsia-pacificAmerciaEuropeAfricaWaferutilization(RHS)Moduleutilization(RHS)Wafersales-to-production(RHS)Modulesales-to-production(RHS)资料来源:CompanydataAsnewcapacitycameintooperationin4Q17andLongiactivelylowereditswaferpricestoimprovethecostperformanceagainstmulti-products,Longi’soverseasmoduleshipmentsgrew18xyoyto687MWin1H18.Webelieve2018marksthebeginningofahigh-growthperiodforLongi’soverseasshipmentsandexpectitsglobalsharetofurtherexpandonrapidcapacityadditionsandcontinuedupgradeinitshigh-efficiencyproductofferings.图表52:WeexpectLongi’swaferandmodulecapacitytoreach45GWand18GWbyend-2020Waferandmodulecapacityforecast(MW)50,00045,00040,00035,00030,00025,00020,00015,00010,0005,0000201620172018E2019E2020EWaferModule资料来源:Companydata,GaoHuaSecuritiesResearchWeexpectLongitogrowitswafershipmentsfrom18.5GWin2018to32.5GWin2020(aCAGRof33%);weforecastmoduleshipmentstogrowfrom6.8GWin2018to14.5GWin2020(aCAGRof46%).Inordertofurtherimprovecostperformanceagainstmulti-productsandexpandmarketshareamidlower

2H18demandinChina,weexpectLongitolowerASPsforitswafer/modulesby35%/22%in2018.For2019-20,weexpect

lessASPdeclineasmarketconsolidationeasesoffin2018;weforecastwaferandmoduleASPstoseecompounddeclinesof7%/6%in2019-20.Ontherevenueside,weexpectLongi’swafer/modulerevenuetoincrease29%/51%toRmb7.4bn/Rmb13.9bnin2018,up33%/17%toRmb9.8bn/Rmb16.2bnin2019andup4%/62%toRmb10.2bn/Rmb26.3bnin2020.图表53:Weexpect33%and46%CAGRsforwaferandmoduleshipmentsin2018-20Waferandmoduleshipment/ASPforecast图表54:WeexpectLongi’swaferandmodulerevenuetosee18%/38%CAGRsin2018-20Waferandmodulerevenue/yoygrowthforecast35,00030,00025,00020,00015,00010,0005,0000(MW)(Rmb/w)201620172018E2019E2020EWafershipmentModuleshipmentWaferASP(RHS)ModuleASP(RHS)4.54.03.53.02.52.01.51.00.50.030,00025,00020,00015,00010,0005,0000(Rmbmn)201620172018E2019E2020EWaferrevenueModulerevenueWaferrevenueyoygrowth(RHS)Modulerevenueyoygrowth(RHS)250%200%150%100%50%0%研究中国资料来源:Companydata,GaoHuaSecuritiesResearch资料来源:Companydata,GaoHuaSecuritiesResearchTosupportitscapacityexpansionplan,weestimateLongi’scapextobeRmb4bn/Rmb4.5bn/Rmb5.0bnin2018-20.Asofend-2017,LongihasanetcashbalanceofRmb8.5bnandoperatingcashflowamountedtoRmb1.2bnin2017.LongihasproposedraisingRmb3.9bnbyissuingnomorethan838mnnewsharestoexistingshareholders.Accordingtothisrightsissueplan,theproceedsraisedwouldbeusedtofundtheconstructionof:1)5GWmonocellcapacity;2)5GWmonomodulescapacity;and3)workingcapital.Althoughweestimatethiscouldresultinac.8%increaseinthetotalnumberofsharesassumingtherightsareissuedatthelastclosingpriceofDecember17,2018,webelieveLongicaneffectivelydriveitsglobalshareandnetincomebasedonitssolidtrackrecord.In2015-17,LongiraisedanaggregateofRmb7.7bntofunditscapacityexpansionplanandtotalsharecapitalincreasedby264%.However,thecompanymanagedtoexpanditsROEfrom11.8%to30.1%onrapidearningsgrowth.

图表55:Historicaloperatingcashflow/netcashflow/cashbalancevs.capex图表56:In2015-17,Longi’sROEexpandedto30.14%from11.8%afteritraisedRmb7.7bnHistoricalfinancingandROE(Rmbmn)9,0008,0007,0006,0005,0004,0003,0002,0001,0000201520162017OperatingcashflowNetcashflowCashbalanceCAPEX3,5003,0002,5002,0001,5001,0005000201520162017ProceedraisedROE35%(Rmbmn)30%25%20%15%10%5%0%资料来源:Companydata资料来源:CompanydataLeadingR&DstrengthtodrivecostreductionWebelievecontinuedinvestmentinR&Dhasbeenthekeydriverofthesector-leadingcostperformanceforLongi’smonoproducts.In2012-17,LongiinvestedRmb24bninR&DwhilemaintainingR&Dexpenseasapercentageofrevenuesatc.5%p.a.In2015-17,themaxvoltageofLongi’smonomodulesrosefrom290Wto334W.图表57:LongihasbeenconsistentlyinvestinginR&DtodrivecostadvantageR&Dexp,R&Dexpas%ofrevandglobalmarketshare(Rmbmn)1,2001,00012%10%图表58:LongihasconsistentlyupgradedtheefficienciesofitsmodulesVoltageof60pcP-typemodule-Longi(W)3503208006004002008%2906%2604%2%23000%201220132014201520162017R&DexpGlobalmarketshareR&Das%ofrev200201520162017AverageMax研究中国资料来源:Companydata资料来源:CompanydataUnlikemostofitspeers,whichpurchasecompletesetsofcrystal-growingequipment,Longiinternallydesignsanddevelopshigh-efficiencycrystal-growingequipmentandcontrollingsoftware;itonlyoutsourcestheproductionofgeneralequipment,whichhasenabledLongitominimizeproductioncostintermsofcapex.Inaddition,Longihasconsistentlyupgradedproductivityofthecrystal-pullingandingotslicingprocesstodrivecostreductions.WeestimateLongiwasabletoreducethenon-siliconcostofitswafersby75%in2012-17,andproductioncostforitsmodulesby41%in2015-17.WeestimateLongi’snon-siliconcostreachedc.US$0.04/wbyend-2017.Goingforward,weexpect

Longitodrivefurthercostreductionsthroughimprovementinitscell’sconversionefficiencies.

图表59:Longihasdrivenwafercostreductionthroughhigh-speed/multiplecrystal-pullingandefficientdiamondwirecuttingtechnologiesProductionprocessofwaferandcoretechnology资料来源:Companydata图表60:Longireduceditsnon-siliconcostby75%in2012-17,andcouldfurtherreduce22%in2018-20ASPandnon-siliconcostofLongi’swafer(Rmb/w)(USD/w)1.41.21.00.80.60.40.20.090.080.070.060.050.040.030.020.01图表61:Longireduceditsproductioncostby41%in2012-17,andcouldfurtherreduce21%in2018-20ASPandproductioncostofLongi’smodule(Rmb/w)4.03.53.02.52.01.51.00.50.02015201620172018E2019E2020EASPNon-siliconcost0.000.02015201620172018E2019E2020EASPProductioncost研究中国资料来源:Companydata,GaoHuaSecuritiesResearch资料来源:Companydata,GaoHuaSecuritiesResearchWeestimateLongicouldlowertheon-siliconcostofitswafersby22%anditsmoduleproductioncostby21%in2018-20.Asaresultofwafer/moduleASPdeclinesof35%/22%ASPin2018,weexpectgrossmarginforLongi’s

wafers/modulestodecline

研究中国from32.7%/30.7%in2017to13.2%/20.6%in2018,butgraduallyrecoverto15.8%/21.1%in2019and15.8%/21.4%in2020ascostreductioncatchesup.图表62:WeexpectLongi’swafer/modulegrossmargintodecline20/10pptto13.2%/20.6%in2018andrecoverto15.8%/21.1%in2019,and15.8%/21.4%in2020Grossmarginofwaferandmodulesegment40%35%30%25%20%15%10%5%0%201620172018E2019E2020EGrossmargin-moduleGrossmargin-wafer资料来源:Companydata,GaoHuaSecuritiesResearchFinancialstatementanalysisP&L:WeexpectLongitodeliver39%revenuegrowthin2018onsolidshipmentgrowthandfurthergrow22%and39%in2019/20.Onthebackof35%/22%wafer/moduleASPdeclinesin2018,weexpectwaferandmodulegrossmarginstofall20/10pptto13.2%/20.6%in2018andgraduallyrecoverto15.8%/21.1%in2019and15.8%/21.4%in2020ascostreductionrecovers.WeexpectEBITmargintofall12pptto11%in2018Eonlowergrossmarginandgraduallyrecoverto12.2%/12.8%in2019/20.WeexpectLongitorecorda32%netincomeCAGRin2018-20.Balancesheet:Atend-2017,Longi’snetgearingwas-15%anditscashbalancewasRmb8.5bn.In2018/19/20,weexpectnetgearingtoincreaseto-10%/-5%/-9%asthecompanyraiseslong-termdebttosupportitscapacityconstructionplans.Cashflow:WeexpectLongitorecordRmb4.0/4.5/5.0bnofcapexin2018-20,mainlytosupportcapacityexpansion.Weexpectthecompany’snetcashflowwillamounttoRmb1.79/1.08/2.30bnin2018-20.

图表63:Summaryofkeyassumptions201620172018E2019E2020EWaferSalesvolume(MW)4,7475,40710,70015,50017,000ASP(Rmb/w)1.071.060.690.630.60Revenue(Rmbmn)5,0755,7537,4019,80910,221Grossmargin18%33%13%16%16%ModuleSalesvolume(MW)1,8471,8471,8471,8471,847ASP(Rmb/w)3.093.093.093.093.09Revenue(Rmbmn)5,7015,7015,7015,7015,701Grossmargin36%31%21%21%21%Totalrevenue(Rmbmn)11,53116,36222,77527,70938,409YoYgrowth94%42%39%22%39%Grossmargin27%32%19%20%21%EBITmargin19%23%11%12%13%Netincome(Rmbmn)1,5473,5652,5373,1984,419YoYgrowth197%130%-29%26%38%资料来源:Companydata,GaoHuaSecuritiesResearchDrivingglobalmonopenetration;initiateatBuyLongiiscurrentlytradingata2019EV/EBITDAof11.7xvs.thehistoricalaverageandmedianof14.1xand12.6x.Longi’scomparablepeershavepostedafive-yearaverageEV/EBITDAof16.7x.Ourdetailedanalysissuggeststhatitspeers’valuationdistributionwasbroadlyrelatedtoEBITDAgrowth.Longi’scurrentEV/EBITDAwasslightlyhigherthantheaverageofitsrangeinthepastfiveyears,butlowerthanthehistoricalaverageofitscomparablepeergroup.WeexpectLongi,withasector-leadinggrowthoutlook,totradeuptotheaverageofitscomparablepeergroup.Webaseour12-monthtargetpriceofRmb26.3onatarget2019EV/EBITDAof16.7x(inlinewiththefive-yearhistoricalaverageofLongi’speergroup).With40%upsidetoourtargetprice,andconsideringourpositiveviewonthecompany’sprospects,weinitiatecoverageofLongiwithaBuyrating.图表64:HistoricalEV/EBITDA图表65:Currentvaluationcomparison40.035.030.025.020.015.010.05.0181614121086420Longi-currentPeers’averageLongi-historical35%30%25%20%15%10%5%0%+1std:20.3xAve:14.1x-1std:8..x0.01/1/20131/1/20141/1/20151/1/20161/1/20171/1/20182018EV/EBITDA2019EV/EBITDA18-20EEBITDAcagr(RHS)研究中国资料来源:Wind,GaoHuaSecuritiesResearch资料来源:Wind,GaoHuaSecuritiesResearch

图表66:HistoricalEV/EBITDAvs.2013-17EBITDACAGR35302520151050ZhonghuanSungrowLongiTBEAGCLAverageMedian13-17EBITDAcagr(RHS)100%90%80%70%60%50%40%30%20%10%0%研究中国资料来源:Wind,GaoHuaSecuritiesResearchKeyrisks:Slower-than-expectedcapacityexpansion.Longiaimstoexpandmonowafercapacityfrom15GWbyend-2017to45GWbyend-2020.Ifitscapacityexpansionturnsoutslowerthanexpected,ourestimateswouldhavedownsiderisk.Lower-than-expectedwaferprices.LowerwaferpriceswoulddragonLongi’sgrossmarginsandposedownsideriskforourestimates.

研究中国ZhejiangChint(601877.SS):Drivingfull-cyclesolarsolution;initiateatBuyDrivingfull-cyclesolarsolution.Asthelargestlow-voltagepowerequipmentmakerinChina,ZhejiangChinttargetsdrivingafull-cyclesolarservicesolutioncoveringupstreamcell/module/invertermanufacturing,midstreamEPCserviceanddownstreamsolarfarmoperationbyleveragingitsstrongfranchiseandcash-flowgenerationinlow-voltageelectricalequipment.ActiveexpansionandoptimizationofprojectportfoliotodrivesolarEPCandoperationrevenue.Leveragingitsstrongfranchiseandcash-flowgenerationinlow-electricalequipment,ZhejiangChinttargetstodriveafull-cyclesolarservicesolutioncoveringupstreamcell/module/invertermanufacturing,midstreamEPCserviceanddownstreamsolarfarmoperation.WeexpectZhejiangChinttorecorda25%CAGRforsolarrevenuein2018-20,mainlydrivenbya45%CAGRfromEPCserviceand19%frompowersales.Low-voltagepowerequipmentre-gainingmomentumpostdistributionrestructure.Thankstoatwo-yeardistributionrestructuringandtheroll-outofthehigh-endKunlunbrand,salesgrowthoflow-voltagepowerequipmentrecoveredto14%in2017,andZhejiangChintfurtherraisedASPby3%-5%in1Q18.WeexpectZhejiangChint’sre-vitalizeddistributionsystemandstrongbrandequitytodrivea13%revenueCAGRforlow-voltagepowerproducts,andweforecastgrossmargintoexpandfrom33.6%in2018to35.6%in2020.Solidgrowthoutlookandundemandingvaluation,initiateatBuy.WeexpectZhejingChinttodelivera28%netincomeCAGRin2018-20.Welikeitsbusinessmodel,whichisbasedondrivinganLCOE-orientedfull-cyclesolarsolution,leveragingitsstrongfranchiseinlow-voltagepowerproductsandleadingexpertiseinsolartech.Giventhesepositives,andwith38%upsidetoour12-monthtargetpriceofRmb32.3(basedon10.5x2019EV/EBITDA),weinitiatecoverageonZhejiangChintatBuy.

研究中国图表67:FinancialsummaryProfitmodel(Rmbmn)12/1712/18E12/19E12/20ETotalrevenue23,416.627,198.131,862.437,418.4Costofgoodssold(16,550.9)(19,095.4)(22,022.2)(25,632.2)SG&A(3,151.2)(3,535.8)(4,142.1)(4,490.2)R&D--------Otheroperatingprofit/(expense)(172.8)(172.8)(172.8)(159.0)EBITDA4,630.75,465.56,780.78,586.1Depreciation&amortization(1,089.1)(1,071.4)(1,255.4)(1,449.1)EBIT3,541.64,394.15,525.37,137.0Interestincome152.0186.8207.1210.2Interestexpense(590.1)(609.7)(642.9)(609.7)Income/(loss)fromuncons.subs.--------Others291.1420.0420.0480.0Pretaxprofits3,394.64,391.25,509.57,217.6Incometax(398.5)(505.0)(633.6)(830.0)Minorities(156.2)(174.9)(243.8)(319.4)Netincomepre-preferred2,839.93,711.34,632.16,068.2Preferreddividends--------Netincome(pre-exceptionals)2,839.93,711.34,632.16,068.2Posttaxexceptionals--------Netincome2,839.93,711.34,632.16,068.2EPS(basic,pre-except)(Rmb)1.341.752.192.86EPS(basic,post-except)(Rmb)1.341.752.192.86EPS(diluted,post-except)(Rmb)1.341.752.192.86DPS(Rmb)0.080.260.330.43Dividendpayoutratio(%)6.015.015.015.0Freecashflowyield(%)(1.5)2.53.06.4Growth&margins(%)12/1712/18E12/19E12/20ESalesgrowth16.116.117.117.4EBITDAgrowth12.318.024.126.6EBITgrowth8.024.125.729.2Netincomegrowth30.030.724.831.0EPSgrowth30.030.724.831.0Grossmargin29.329.830.931.5EBITDAmargin19.820.121.322.9EBITmargin15.116.217.319.1Cashflowstatement(Rmbmn)12/1712/18E12/19E12/20ENetincomepre-preferreddividends2,839.93,711.34,632.16,068.2D&Aadd-back1,089.11,071.41,255.41,449.1Minoritiesinterestsadd-back156.2174.9243.8319.4Net(inc)/decworkingcapital(1,877.5)(1,094.6)(1,266.0)(1,031.4)Otheroperatingcashflow359.9------Cashflowfromoperations2,567.63,863.04,865.26,805.2Capitalexpenditures(3,233.3)(2,577.4)(3,295.4)(3,467.3)Acquisitions--------Divestitures--------Others520.0------Cashflowfrominvestments(2,713.3)(2,577.4)(3,295.4)(3,467.3)Dividendspaid(common&pref)(1,277.3)(115.9)(556.7)(694.8)Inc/(dec)indebt218.2------Commonstockissuance(repurchase)4,777.5------Otherfinancingcashflows(562.0)------Cashflowfromfinancing3,156.5(115.9)(556.7)(694.8)Totalcashflow3,010.81,169.81,013.12,643.1Balancesheet(Rmbmn)12/1712/18E12/19E12/20ECash&equivalents6,226.37,396.18,409.211,052.3Accountsreceivable8,862.810,432.112,395.814,147.2Inventory3,271.33,923.74,585.45,126.4Othercurrentassets2,679.82,679.82,679.82,679.8Totalcurrentassets21,040.124,431.728,070.233,005.8NetPP&E16,092.717,645.719,734.121,802.1Netintangibles344.2297.2248.8199.0Totalinvestments1,885.31,885.31,885.31,885.3Otherlong-termassets4,793.04,793.04,793.04,793.0Totalassets44,155.449,052.954,731.461,685.1Accountspayable7,348.18,475.29,834.611,095.6Short-termloans2,092.52,092.52,092.52,092.5Othercurrentliabilities3,590.53,590.53,590.53,590.5Totalcurrentliabilities13,031.114,158.215,517.616,778.6Long-termdebt8,992.28,992.28,992.28,992.2Otherlong-termliabilities1,561.71,561.71,561.71,561.7Totallong-termliabilities10,553.910,553.910,553.910,553.9Totalliabilities23,585.024,712.126,071.527,332.5Preferredshares--------Totalcommonequity19,986.523,581.927,657.333,030.7Minorityinterest584.0758.81,002.61,322.0Totalliabilities&equity44,155.449,052.954,731.461,685.1BVPS(Rmb)9.4311.1313.0515.59Ratios12/1712/18E12/19E12/20ECROCI(%)20.119.020.322.4ROE(%)17.017.018.120.0ROA(%)7.18.08.910.4Inventorydays58.668.870.569.1Receivablesdays126.6129.5130.8129.5Payabledays147.5151.2151.7149.0Netdebt/equity(%)23.615.29.30.1Interestcover-EBIT(X)8.110.412.717.9Valuation12/1712/18E12/19E12/20EP/Ebasic(X)15.713.711.08.4P/B(X)2.22.21.81.5EV/EBITDA(X)10.810.18.06.1EV/GCI(X)1.91.91.61.3Dividendyield(%)0.41.11.41.8Note:Lastactualyearmayincludereportedandestimateddata.Source:Companydata,GoldmanSachsResearchestimates.资料来源:Companydata,GaoHuaSecuritiesResearch

Leveragingsynergybetweenlow-voltagepowerequipmentandsolartechtodriveLCOE-orientedfull-cyclesolarsolutionIncorporatedin1997,ZhejiangChintisthelargestlow-voltageelectricalequipmentmakerinChinaandisactivelyexpandingitssolarpoweroperationandmanufacturingbusinesswith2.2GWsolarfarmsand2.2GWofsolarmodulecapacitybyend-2017.Leveragingitsstrongfranchiseandcash-flowgenerationinlow-voltageelectricalequipment,ZhejiangChintaimstodriveafull-cyclesolarservicesolutioncoveringupstreamcell/module/invertermanufacturing,midstreamEPCserviceanddownstreamsolarfarmoperation.In2016,ZhejiangChintacquired85.4%ofChintNewEnergy,100%ofLeqingXiangru,100%ofLeqingZhantu,100%ofLeqingFengyuanand100%ofHangzhouTaikubyissuing562mnadditionalsharestoChintGroupandothershareholdersatRmb16.66(representingaconsiderationofRmb9.37bn),throughthistransaction,ZhejiangChintacquired99.44%ofChintNewEnergy(1.5GWofsolarfarmcapacityand700M/1.7GWsolarcell/modulecapacity).ChintalsoraisedRmb4.36bnbyissuing248mnadditionalsharesatRmb17.58/sharetofundfurthersolarfarmconstruction.图表68:ZhejiangChinthas2.2GWsolarfarmsbyend-2017Capacityandrevenueofsolarfarmoperation图表69:Solarbusinessaccountedfor40%oftotalrevenuein2017Historicalrevenuebreakdownbysegment2,5002,0001,800(MW)(Rmbmn)1,6001,40025,00020,000(Rmbmn)1,5001,2001,00015,0001,00050080060040020010,0005,000002015201620170201220132014201520162017CapacityRevenue(RHS)SolarmodulesSolarpowerSolarfarmEPCOthersLow-electricalequipment资料来源:Companydata资料来源:Companydata图表70:Historicalgrossmarginbysegment图表71:ZhejiangChintrecordedan18%netincomeCAGRin2012-17HistoricalnetincomeandEBITmargin70%60%50%40%30%20%10%3,0002,5002,0001,5001,00050025%(Rmbmn)20%15%10%5%0%20122013201420152016201700%201220132014201520162017SolarmodulesSolarfarmEPCLow-voltageelectricalequipmentSolarpowerNetincomeEBITmargin

研究中国资料来源:Companydata资料来源:Companydata

ActiveexpansionandoptimizationofprojectportfoliotodrivesolarEPCandoperationrevenueLeveragingitsstrongfranchiseandcash-flowgenerationinlow-voltageelectricalequipment,ZhejiangChintaimstodriveafull-cyclesolarservicesolutioncoveringupstreamcell/module/invertermanufacturing,midstreamEPCserviceanddownstreamsolarfarmoperation.WeexpectZhejiangChinttorecorda25%CAGRforsolarrevenuein2018-20,mainlydrivenbya45%CAGRforEPCserviceand19%forpowersales.Withproductioncapacitycoveringhigh-efficiencysolarcell/moduleandinverters,ZhejiangChinthasbuiltanaggregateof3.5GWsolarprojectsgloballyandoffersanLCOE-orientedfull-cycleEPCservicetodownstreaminvestors.Withastrongbalancesheetandglobalfranchisefromlow-voltageelectricalequipmentbusiness,webelieveZhejiangChintisbest-positionedtoridearisingsectorconcentrationasdownstreamsolarfarminvestorshavedisplayedanincreasingpreferenceforLCOE-orientedfull-cycleEPC/BTservicesprovidedbylarge-scaleleadingEPC/BTcompanies,inourview.WeexpectZhejiangChint,withmorethan2.8GWofpipelineonhandasofend-2017,todeliver230/350/500MWofEPCprojectsin2018-20,andrecorda45%revenueCAGRduringthisperiod.图表72:WeexpectEPCservicetodelivera45%revenueCAGRin2018-20EPCprojectvolumeandrevenueforecast图表73:ZhejiangChinthas2.89GWprojectpipelineatend-2017Installedprojectsatyear-endandprojectpipelineonhand8,0007,0006,0005,0004,0003,0002,0001,000600(Rmbmn)(MW)5004003002001003,500(MW)3,0002,5002,0001,5001,00050000201620172018E2019E2020ERevenueEPCproject0Projectsatyear-endPipeline20162017研究中国资料来源:Companydata,GaoHuaSecuritiesResearch资料来源:Companydata图表74:ConversionefficiencyofZhejiangChint’scellandinverter20162017Multicell18.60%20.10%Monocell20%21.40%Inverter98.50%98.50%资料来源:Companydata

GridconnectionTransformerSwithgearACcabinetTransformerDCcabinetCombinerboxSolarmodulesInverter图表75:ZhejiangChintoffersaLCOE-orientedfull-cycleEPCsolution研究中国资料来源:CompanydataZhejiangChintisalsoactivelyexpandingintheresidentialroof-topEPCbusiness.In2017,ZhejiangChintcompleted40,000residentialroof-topprojectsanddevelopedover60distributorsinZhejiangprovinceandover22distributorsinAnhui,HenanandShandongprovinces.Althoughtheresidentialroof-topbusinessofferssmallersingle-projectscale(usually3-5kwperproject),webelievetheresidentialroof-topmarketofferstremendousupsideinChinaonthebackof:1)theimprovingeconomicsofsolarpower;and2)adequateroof-topspaceinruralareaswithlowpenetrationsinChina.Asofend-2017,Chinahadaruralpopulationof577mnand645mnhaoffarminglandarea;weestimatethatthiscouldcreateinstallationsitesformorethan300GWofpotentialresidentialroof-topprojects(assuming100mnofruralhouseholdswith20m2ofroof-topareaeachcarrya3kwproject).Leveragingitsnationwidedistributionnetworkandstrongbrandequityfromthelow-electricalequipmentsegment,webelieveZhejiangChintiswell-positionedtorideontherisingruralresidentialroof-topmarketgoingforward.

图表76:Chinahadaruralpopulationof577mnasofend-2017Ruralpopulationandaveragemonthlyincome图表77:Chinahad645mnhaoffarmlandasofend-2017FarmlandareainChina6606406204,000(Rmbmn)(Rmb)3,5003,0002,500650(Mnhectare)6456406002,0006355805601,5001,0005006306255400201220132014201520162017RuralpopulationAveragemonthlyincome620201520162017201520162017资料来源:Companydata资料来源:CompanydataForthedownstreamoperationbusiness,ZhejiangChinthasbeencontinuouslyoptimizingitsprojectportfoliotodriveinvestmentreturns.TheportionofcapacityfromDGhasgrownfrom20%in1Q17to48%in3Q18.DGoffersbettercashflowgenerationandlesscurtailmentriskscomparedtoutility-scaleprojects,inourview.WeexpectZhejiangChinttoadd200/350/400MWofnewcapacityin2018-20andrecorda19%revenueCAGRfrompowersales.Weexpectgrossmargintoexpandfrom64.9%in2018to70.1%in2020thankstocontinuedportfoliooptimization.图表78:TheportionofDGoftotalcapacitygrewfrom20%in1Q17to48%in3Q18Solarfarmcapacitybreakdown(MW)2,5002,0001,500图表79:WeexpectZhejiangChinttoadd200/350/400MWin2018-20Accumulativecapacityandnewadditionofsolarprojects(MW)3,5003,0002,5002,0001,0001,50050001Q172Q173Q174Q171Q182Q183Q18UtilityDG1,0005000201620172018E2019E2020EAccumulativecapacityNewaddition研究中国资料来源:Companydata资料来源:Companydata,GaoHuaSecuritiesResearch

图表80:Weexpectgrossmarginofpowersalestoexpandfrom64.9%to70.1%in2018-20Solarfarmoperationrevenueandgrossmarginforecast3,5003,0002,5002,0001,5001,00050080%(Rmbmn)70%60%50%40%30%20%10%研究中国00%201620172018E2019E2020ERevenueGrossmargin资料来源:Companydata,GaoHuaSecuritiesResearchForsolarmodulesales,weexpecttoseea15%revenuedeclinein2018duetoa15%ASPdrop,andweexpectrevenuegrowthrecoverto4%/15%in2019/20asChinademandrecovers.Grossmarginshoulddrop9pptto9%in2018onlowerASP,butweexpectittograduallyrecoverto10%/12%in2019/20.Low-voltagepowerequipmentre-gainingmomentumpostdistributionrestructureAsthelargestlow-voltagepowerequipmentmakerinChina,ZhejiangChintrecordedrevenueofRmb14bnin2017,withc.17%-18%marketshareonourestimate.Webelieveitscompetitiveadvantageliesin:1)Strongbrandequitythroughconsistentlyrollingouthigh-qualityproductsandthewidestproductofferingsacrossthevaluechain;2)avastandhighlyefficientdistributionnetwork(400coredistributorsand2,800distributionoutletsby2017);and3)itsCIP(ContinuedImprovementinProcess)initiativetooptimizecoststructureandimproveproductivity.

研究中国图表81:Salesvolumeoflow-voltageelectricalequipment(Mnunit)1,4001,2001,00080060040020002015201620172018E2019E2020EPowerDistributionEquipmentTerminalDevicePowerControlEquipmentPowerSupplyEquipmentPowerElectronicsInstrumentsandMetersBuildingElectricalAppliances资料来源:Companydata,GaoHuaSecuritiesResearchZhejiangChint’slow-voltagepowerequipmentsalessawrapidgrowthin2011-13witha24%CAGR.Revenuegrowthslowedto7%in2014and-7%in2015onahighcomparablebaseandaweakmacrobackground.Inlate2015,ZhejiangChintstartedtorestructureitsdistributionnetworkby:1.Introducingatwo-layerdistributionnetwork;thenumberofcoredistributorsincreased33%yoyto400in2017.2.Optimizingtheincentivesystemfordistributors.ZhejiangChintstartedshareholdingschemeforselecteddistributorsinJanuary2018(ChintGroupsold24.18mnsharesofZhejiangChinttoGuotai-Gubenassetmanagementplanat22.47rmb/shareinconnectionwithashareholdingschemeforselectdistributorsandemployees).In2016,ZhejiangChintrolledoutanupgraded“Kunlun”brand.WithoverRmb150mnofinvestmentinR&D,360patentsand7,860reliabilitytests,“Kunlun”offersahigher-qualityversionofitsexistingproductline.